|

Corequity Valuations

Corequity provides

independent, institutional equity valuation research. The results are used

to screen for the best and worst values out of over 500 equities on a

continuous basis. We have accumulated a proprietary database of historical

monthly valuation data. For a brief background...

http://corequity.blogspot.com/2013/05/some-background.html

Real Growth vs Growth Lite

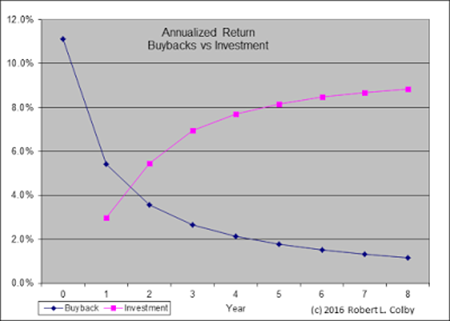

Our Net Profit Test: Comparing Buybacks to Investment shows that a

company’s purchase of its own shares causes a single increase in EPS (as

in simple interest) compared to compounding growth that results from

investment. This graph shows the annualized returns of the two asset

allocation decisions over time. The sinking annualized return on a

buyback explain the relatively low level of return required to grow the

Net Profit at the rate that the buybacks achieved due to the fewer number

of shares.

(See “Net Profit Test: Comparing Buybacks to Investment” at

corequity.blogspot.com)

The sinking annualized return on a buyback explains the relatively low

level of return required to grow the Net Profit at the same rate that a

buyback achieves due to the fewer number of shares.

To illustrate the advantage of Investment over Buybacks, here are two very

similar companies who couldn’t be further apart in their asset allocation

choices. The two are Cracker Barrel (CBRL) and Jack in the Box (JACK).

They are both mid-cap Restaurant companies trading at 19x earnings.

|

Company data as of May 31st |

CRBL |

JACK |

|

INDUSTRY |

RESTAURANT |

RESTAURANT |

|

MARKET CAP |

MID-CAP = $3.5 B |

MID-CAP = $2.4 B |

|

P/E |

19x |

19x |

|

YIELD |

3.1% |

1.6% |

|

2008-15 CASH FLOW - DIVIDENDS |

$1.27 bil |

$1.23 bil |

|

2008-15 STOCK BUYBACKS |

-$0.16 bil |

-$1.20 bil |

|

2008-15 CHANGE IN SHARES O/S |

+7% |

-37% |

|

GROWTH OF EPS 2008-2015 |

+144% or +13.6% pa |

+50% or +6.0% pa |

|

GROWTH IN NET PROFIT “ |

+151% or +14.0% pa |

-4% or -0.5% pa |

|

REQ’D AFTER TAX % TO = EPS GROWTH[1] |

- |

4.8% |

CBRL’s

Cash Flow from Operations less Dividends totaled $1.27 billion from 2008

and 2015. Most of this was invested in its operations as indicated by its

book value per share which grew from $4.15 to $22.45. As a result of this

investment, their Net Profit growth equaled the growth in EPS over the 7

years (+14.0% vs +13.6%) as their shares outstanding increased slightly.

By contrast, JACK bought $1.2 billion of their own stock, reducing their

shares outstanding by 37%. As a result their EPS grew by 6.0% pa entirely

due to buybacks but their Net Profit actually declined by 3.7%, or

-0.5% pa.

The Shareholders of JACK today would have been much better off had

management invested those funds - as much as that may have made the

Sharesellers happy. The company would only have to earn a 4.8% return on

those funds for the Net Profit to match the “growth” in EPS (the Net

Profit Test). That would have generated $64 million more in Net Profit in

2015 alone, or 56% more than they actually achieved ($178 million vs

$115).

Much has been said about the role of share buybacks in executive stock

options. It is therefore interesting to note how much these two companies

compensated their senior management. In 2015, Jack in the Box led by

$16.6 to $13.8 million.[2]

The five year average number is closer but JACK still wins: $9.9 to $9.6

million.

In JACK’s case, management is clearly not being judged by the Net Profit

Test.

|

© 2016 Robert L. Colby |

June 23rd 2016 |

[1]

The required rate of return applied to the buyback funds to grow the Net

Profit at the same rate as the EPS.

[2]

Morningstar

|