|

For Q3 2012, 82 S&P 500

companies have issued negative EPS guidance while 21 companies have

issued positive EPS guidance. If 82 is the final number of companies

issuing negative EPS guidance for the quarter, it will mark the third

highest number for a quarter during the past five years, only trailing

the numbers recorded in Q4 2011 (84) and Q4 2008 (83). If 21 is the

final number of companies issuing positive guidance for the quarter, it

will mark the lowest number of companies for a quarter since FactSet

began tracking guidance in Q1 2006.

As a result, the overall

percentage of companies issuing negative guidance for Q3 2012 stands at

80% (82 out of 103). If this is the final percentage for the quarter, it

will be the highest percentage recorded since FactSet began tracking

guidance data in Q1 2006. The Q4 2011 quarter currently has the record

for the quarter that finished with the highest percentage of companies

issuing negative EPS guidance (73%).

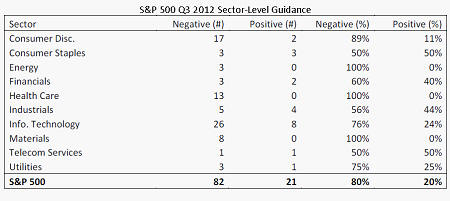

At the sector level (with a

minimum of five companies issuing quarterly EPS guidance), the Health

Care (100%) and Materials (100%) sectors have the highest percentages of

companies that have issued negative EPS preannouncements, while the

Consumer Staples (50%) and Industrials (44%) sectors have the highest

percentage of companies that have issued positive EPS preannouncements.

Although the percentage of

negative preannouncements is running at an all-time high, the market is

not punishing the price performance of these stocks in the short term.

For the 82 companies that have issued negative EPS guidance for Q3 2012

to date, the average price change (2 days before the guidance was issued

through 2 days after the guidance was issued) was 0.0%. This percentage

is above the average over the past five years of -1.8%. Just under half

of the companies (36) that have issued negative guidance have recorded

an increase in price during this time frame. Ten of these companies

witnessed a double-digit increase in price.

For companies that have

issued positive guidance, the story has been even better. Of the 21

companies that have issued positive EPS guidance for Q3 2012, the

average price increase has been +6.7%. This percentage is also well

above the average over the past five years of +2.6%.

On average, companies issued

EPS guidance that was 10.5% below the mean EPS estimate. This difference

is below the trailing 5-year average (-7.8%).

Read more about

the EPS guidance trends of the S&P 500 in this month's edition of

FactSet Guidance Monthly.

|

![[Maxwell Murphy]](http://si.wsj.net/public/resources/images/HC-GQ212_Murphy_AV_20110920101002.jpg)