|

THE

WALL STREET JOURNAL.

Markets

Activist Investors’ Secret Ally: Big Mutual Funds

Large investors quietly back campaigns to force change at U.S.

companies

|

ValueAct Capital Management founder and CEO Jeffrey Ubben, left,

and President Mason Morfit have sought support from mutual funds

in their efforts to force change at big companies. PHOTO:

JASON HENRY FOR THE WALL STREET JOURNAL |

By

David Benoit

and

Kirsten Grind

Updated Aug. 9, 2015 10:38

p.m. ET

When a low-profile

activist investor gained a board seat at

Microsoft Corp.

two years ago, corporate boards around the country were

stunned. How had a shareholder with less than 1% of the software

giant’s stock forced its way into the boardroom?

It turns out that

ValueAct Capital Management LP had some serious muscle behind the

scenes. Founder and Chief Executive Jeffrey Ubben and President Mason

Morfit had reached out to some of Microsoft’s biggest

stockholders—large mutual-fund companies not known for rocking the

boat—to ask for help.

Several of them,

including Franklin Templeton Investments and Capital Research &

Management Co., which together held morein a than 6% of Microsoft’s

stock, then contacted the company. Within five months, ValueAct had

its board seat.

Activist investors are

prevailing more than ever in their battles to force change at large

U.S. companies, in many cases because of support from big investors

who traditionally have stayed quiet. And that is changing the way U.S.

businesses respond to challenges from activist campaigns.

The shift comes as

activist investors set their sights on bigger companies. Last week,

investor William Ackman’s Pershing Square Capital Management LP

disclosed

a $5.5 billion stake in food giant

Mondelez International

Inc.

It also emerged that ValueAct has taken a

roughly $1 billion stake in

American Express

Co.

Large mutual funds have

long been seen as friends of management who buy a stock because they

liked what a company is doing. A decade ago, they would rarely even

pick up the phone to talk with activists bent on challenging the

status quo, according to activists and corporate advisers who

specialize in such situations.

These days, mutual funds

often are siding with activists. They quietly have backed some of the

most prominent activist campaigns, including Starboard Value LP’s

removal of the entire board at

Darden Restaurants Inc.

last year and a push at

General Motors Co. this year for a quicker share buyback. Although

Nelson Peltz ultimately

lost his campaign to get on the board of

DuPont

Co., he came close thanks to the support of many investors.

In a survey this year of

more than 350 of mutual-fund managers, Rivel Research Group, which

polls investors for companies, found that half had been contacted by

an activist in the past year, and 45% of those contacted decided to

support the activist.

“In contrast to the

situation of just a few years ago, companies must examine their

long-only shareholders with a critical eye,”

J.P. Morgan

bankers wrote to clients

earlier this year. “There are no ‘management friendly’ investors.”

Boardroom effect

That shift is changing

the way fights play out in boardrooms. Rather than face one loud

activist, companies sometimes are forced to contend with pressure from

multiple shareholders. That has made some companies more receptive to

activists and their ideas, such as share buybacks, cost-cutting and

asset sales, even as debate continues about how such moves affect the

health of companies.

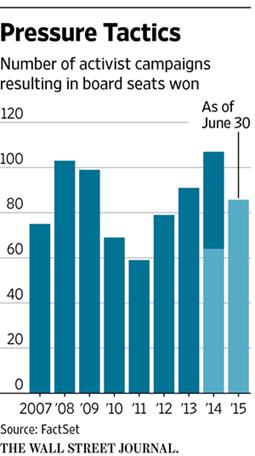

Activist investors take

stakes in companies they think are underperforming and push for

financial, strategic or leadership changes. Last year, activists

gained board seats at a record 107 companies, 91 of them through pacts

negotiated with the companies, according to data provider

FactSet. This year has gotten off to an even faster start, with

activists gaining seats at 86 companies in the first half alone.

When companies resist,

they are more often losing shareholder votes. In 2014, activists won

in a record 73% of battles for board seats in the U.S., up from 52% in

2012, according to FactSet.

The increasing

involvement of mutual funds comes as retail investors have been moving

money from stock-picking mutual funds to index funds and other funds

that track baskets of securities. That is increasing the pressure on

mutual-fund managers to beat the market, investors say.

“Everybody is looking

for an edge,” says Peter Langerman, the head of a large mutual-fund

unit at Franklin Templeton, which oversees about $75 billion.

Some mutual funds are

voicing public support for activists’ positions. But many funds worry

that admitting to working with activists will cost them access to

management at companies in which they hold stakes, according to

investors and corporate advisers.

Private talks between

activists and mutual funds are becoming more common.

In April at the Milken

Institute’s annual conference in Los Angeles, a group of activists and

major institutional investors gathered in a closed-door meeting to

discuss their relationships, according to one person who attended.

They debated whether activists work in the long-term interest of all

shareholders, or are only after shorter-term profits. The two groups

agreed that companies are listening more to investors of all stripes,

which they saw as a positive.

The 10 largest

shareholders of an S&P 500 company, on average, hold 44.7% of the

company’s stock, says

Lazard Ltd.

banker Jim Rossman, who specializes in helping

companies deal with activists. That means winning the support of major

shareholders can put an activist on the path to victory, while losing

it can spell doom.

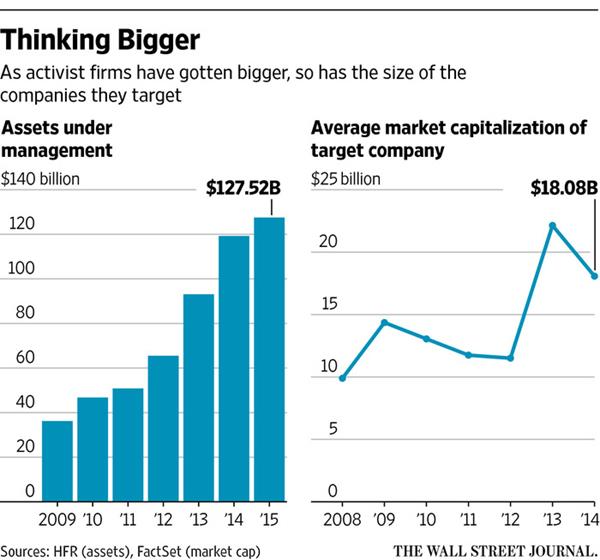

The average size of an

activist’s stake in a target company shrunk to 6.1% last year, from

7.7% in 2006, according to FactSet, which suggests that activists can

spend less and still win.

| |

Steve Ballmer announced in August 2013 that he would step down

as chief executive of Microsoft and retire.

Photo: Stuart Palley for The Wall Street Journal

|

Companies recognize the

importance of courting their institutional shareholders and have been

bulking up investor-relations departments, according to corporate

advisers and investor-relations experts. Corporate lawyers and bankers

urge companies to articulate a clear strategy or risk having an

activist-recommended strategy sounding better. Some companies are

having directors engage with shareholders regularly.

Institutional funds, for

their part, have “realized they have influence” and are saying, “We

have a responsibility to have a sophisticated approach to voting,”

Lazard’s Mr. Rossman said.

Mutual

funds have moved slowly into voting against management. They started

on governance issues, such as forcing annual elections for directors

and rejecting corporate pay in nonbinding referendums. This year, a

widespread push forced companies from

General Electric Co.

to

Citigroup Inc.

to

change their corporate rules and allow shareholders to more easily

nominate directors.

In the spring of 2013,

San Francisco-based ValueAct, which has about $20 billion under

management, asked for a single board seat at Microsoft for either its

chief executive, Mr. Ubben, or its president, Mr. Morfit, according to

people familiar with the request. ValueAct indicated it would fight

publicly for the seat if it couldn’t reach an accord.

Messrs. Ubben and Morfit

aren’t known for starting such proxy fights. ValueAct representatives

have served on the boards of

Valeant Pharmaceuticals International Inc.

and

Adobe Systems Inc.

Building

relationships

ValueAct’s

Microsoft plan was ambitious, given its less than 1% stake. But it has

been building relationships with mutual funds for years. Tapping those

contacts, Messrs. Ubben and Morfit called investors such as Martin

Flanagan, chief executive of Invesco Ltd., and Mr. Langerman of

Franklin Templeton’s Mutual Series unit, according to people familiar

with the conversations.

Their pitch: They wanted

a board seat, and, if necessary, planned to run a campaign against the

record of

Steve Ballmer, then Microsoft CEO, these people say. ValueAct

claimed management had been slow to adapt to new technologies and had

lost the pioneering position it once held, hurting shareholder value.

It wanted Microsoft to refocus on its technology aimed at large

companies, such as software for corporate computing centers and a

version of its Microsoft Office software that had been remodeled for

the Web and mobile devices, these people say.

Franklin’s Mr. Langerman

and his team spoke several times with ValueAct executives to hear

their pitch and agreed that Microsoft needed a change. Later, in

discussions with Microsoft, they urged support for the activist’s

position, according to those familiar with the talks.

Capital Research, a

mutual-fund giant with $1.5 trillion under management, had been

expressing concern to Microsoft about its slumping share value before

ValueAct came along, according to people familiar with the talks. When

the firm’s technology analyst Paul Benjamin spoke with ValueAct

executives, they agreed that Microsoft needed help quickly. Mr.

Benjamin contacted Microsoft board members and urged them to work with

ValueAct.

In November 2012, in a

sign of the brewing discontent, Capital Research’s funds and others

withheld their support for the re-election to the board of Messrs.

Ballmer and Gates, according to vote-tracker Proxy Insight.

The two directors were

still elected by a wide margin. More than 96.6% of shares voted for

both, but the other directors got 99%. Such “no” votes are rare.

Capital Research’s American Funds, for instance, back management in

97.4% of all campaigns, according to Proxy Insight.

In August 2013,

Microsoft announced

Mr. Ballmer would retire. The company has said the leadership

change was in the works before ValueAct arrived, and that the fund

played no part in Mr. Ballmer’s departure.

After his retirement was

announced, Microsoft reached out to ValueAct to ask if it still wanted

a board seat, according to people familiar with the discussion.

ValueAct said it was happy with the change, but wouldn’t budge on its

board demand.

The following week—just

before a deadline for an investor to launch a fight for

seats—Microsoft announced Mr. Morfit would join the board.

Darden Restaurants,

which owns the Olive Garden chain, triggered a fight with activists

when its board decided last year to sell its Red Lobster chain even as

shareholders were seeking a vote on the matter, people on both sides

have said.

New York-based

Starboard, fellow activist Barington Capital Group LP and Darden duked

it out publicly. Starboard released a 300-page PowerPoint presentation

that criticized everything from Darden’s management to the lack of

salt in Olive Garden’s pasta water.

Capital Research, once

the largest shareholder, tried to broker a settlement. Capital

Research executive Gregory Wendt acted as a go-between with Darden

management and Starboard. He tried to find a way to change the board

but leave some members in place for continuity’s sake, a common

concern among institutional holders, people involved in the fight say.

The fight turned bitter,

and no settlement was reached.

Investors voted out the entire board last October, a particularly

whopping defeat for management. Capital Research voted for all 12 of

Starboard’s nominees, say people familiar with the vote.

At times, mutual funds

offer only qualified support for activists.

Investor Harry J. Wilson

went public in February with plans to push General Motors for a stock

buyback and a board seat. Mr. Wilson’s team quietly put out feelers to

big investors to see if they would support him, according to people

familiar with his campaign.

At Franklin Templeton’s

offices in Short Hills, N.J., Mr. Wilson made his pitch to portfolio

manager F. David Segal and others. He said he wanted GM to repurchase

$8 billion in stock.

Shortly thereafter, Mr.

Segal called GM’s head of investor relations and said Franklin’s

Mutual Series unit was sympathetic to Mr. Wilson’s views but thought

the buyback number was aggressive. Mr. Segal told GM that while

shareholders had been grumbling about the issue in the past, it had

become more public and the company needed to address it head-on,

according to people familiar with the call.

In early March, GM

announced it would undertake, earlier than originally planned,

a $5 billion buyback that was already in the works. Mr. Wilson

pulled his request for a board seat a month after he had made it.

ValueAct

also has gotten fast action at times.

In January, ValueAct

released a letter it wrote to stock-market-indexing company

MSCI Inc.

ValueAct wrote that MSCI had rebuffed its attempts to

get a board seat and hadn’t even checked the references ValueAct had

sent. Other MSCI holders quickly weighed in. Independent Franchise

Partners LLP and

T. Rowe

Price

Group, both top five holders, wrote

letters arguing ValueAct’s track record warranted a spot on the board.

Three weeks later,

ValueAct got the seat and two others.

Write to

David Benoit at

david.benoit@wsj.com and Kirsten Grind at

kirsten.grind@wsj.com

|