|

Business Day

Safety Suffers as Stock Options Propel Executive Pay Packages

SEPT.

11, 2015

Outsize

executive pay packages have

frequently been a flash point for stock market investors. Lavish

executive compensation at publicly traded companies should be a

significant concern for consumers, too.

That’s

the message of a new study by three academics at the University of

Notre Dame. Their research focuses on companies that rely heavily on

stock options in executive compensation. They have found a correlation

between generous option grants and the incidence of serious product

recalls.

Stock

options have been the jet fuel propelling some of the biggest

executive pay packages over the years. From an investor’s point of

view, these instruments are problematic because they provide an

executive with little downside if the company’s underlying shares fall

but oodles of upside on the rise.

| |

Fair Game

A

column from Gretchen Morgenson examining the world of finance

and its impact on investors, workers and families

See More »

|

| |

|

This

heads-I-win, tails-I-barely-lose arrangement encourages executives to

swing for the fences, an array of academic research has shown. Eager

to reap the riches from a rising share price, option-laden executives

have been found to make unwise acquisitions or, even worse, to

undertake aggressive accounting practices.

Now

comes evidence that product recalls are often linked to abundant

option grants handed to chief executives. The

study, “Throwing Caution to the

Wind: The Effect of C.E.O. Stock Option Pay on the Incidence of

Product Safety Problems,” concluded that “C.E.O. option pay was

associated with both a higher likelihood of experiencing a recall as

well as a higher number of recalls.”

The

study’s authors are Adam J. Wowak, Michael J. Mannor and Kaitlin D.

Wowak, all assistant professors of management at the Notre Dame

Mendoza College of Business.

In an

interview on Tuesday, Mr. Wowak said that he and his colleagues wanted

to build on past analyses of how stock options induce risk-taking

among executives. “If options are generally causing C.E.O.s to be more

aggressive, then it makes sense that more mistakes could occur and

consumers could be affected,” Mr. Wowak said. “Options could be making

C.E.O.s ignore the downside potential of some of their actions.”

The

researchers scrutinized companies in two industries that are closely

regulated by the Food and Drug Administration. All of the companies

had sales and assets of at least $10 million. The academics looked at

the size of stock options in proportion to a chief executive’s total

pay and calculated a two-year average, finding that recalls tended to

be more prevalent at companies with higher option percentages. The

names of specific companies were not cited in the study.

One

group of companies produced consumer staples like foods, beverages and

personal care products, while the other manufactured health care

products, including medical devices and pharmaceuticals. Over the

period studied — from 2004 through 2011 — these two sectors together

accounted for over 85 percent of all recall activity reported by the

F.D.A., the professors said.

Their

analysis examined two significant types of product recalls: those in

which a product could cause serious harm or death and those in which

exposure to a product might cause temporary or medically reversible

health consequences.

The

study examined the pay packages of 386 chief executives. One curious

finding emerged: Product recalls were less common among companies

whose chief executives founded the companies or had long tenures

there. Such executives may be more risk-averse because they are

generally large shareholders and may also feel that their personal

reputations are intertwined with their companies’ actions.

“It

was interesting for us to see that options don’t affect everybody the

same way,” Mr. Wowak said in the interview. “When boards design pay

packages, it would be beneficial for them to think about how their

C.E.O. might respond and tailor the package around that.”

Mr.

Wowak acknowledged that among publicly traded corporations over all,

stock option grants as a percentage of total pay had declined

recently. Many companies are dispensing restricted stock instead,

making sure that executives feel the pain of a falling share price

alongside their stockholders. With options, a falling stock price

represents a lost opportunity for a future gain, not an actual hit to

executives’ wallets.

But

stock options remain popular. Data compiled by

Equilar, an executive compensation

analytics firm in Redwood City, Calif., shows that among the companies

in the Standard & Poor’s 500-stock index, option grants totaled 16.1

percent of direct pay for chief executives in 2014. In 2010, that

figure was 20.1 percent.

“Of

course, not every product recall that happens is caused by stock

options,” Mr. Wowak said. “And it’s possible to pay a lot in options

and not have a product recall. But boards are wise to have a balanced

view of the potential downside to building in heavy option components

to executive pay.”

The

researchers’ focus on health care companies was appropriate: These

companies are the biggest users of stock options, Equilar found. Last

year, 84.4 percent of chief executives at these companies received

options, while 67.3 percent of top managers at consumer goods

manufacturers were recipients, according to Equilar. At utility

companies, by contrast, only 27.6 percent of chief executives were

granted options.

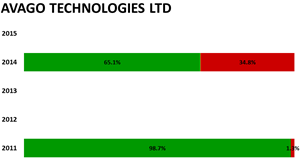

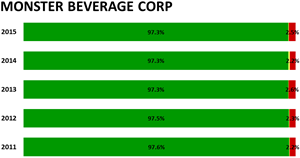

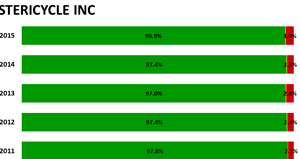

Among

the top dispensers of stock options as a percentage of total C.E.O.

pay, Equilar found, are Monster Beverage, with 87.1 percent; Avago

Technologies, a semiconductor maker, with 84.2 percent; and Stericycle,

a medical waste management company, at 69.7 percent.

Representatives from the three companies did not respond to requests

for comment.

Having

fielded complaints from shareholders about excessive executive pay for

decades, corporate boards say they have gotten the picture that chief

executives’ pay should be aligned with their owners’ interests. As

this new study shows, directors should understand that executive pay

needs to line up with consumers’ interests as well.

A version of this article appears in print on September 13, 2015, on

page BU1 of the New York edition with the headline: Safety Suffers in

Executive Pay Packages.

© 2015 The

New York Times Company |