|

THE

WALL STREET JOURNAL.

Markets

Companies Forgot About Mom-and-Pop Investors...Until Now

Under pressure, companies turn to individual shareholders to help

fight their battles

|

CSX,

stung by defeat in a campaign against activists, jazzed up its

shareholder mailings and now even plants trees to encourage

individuals to vote. PHOTO: LUKE SHARRETT/BLOOMBERG NEWS |

By

Vipal Monga

and

David Benoit

July 19, 2016 5:30 a.m. ET

Companies under pressure from shareholder activists and other big

investors are increasingly turning to an unlikely source for help: mom

and pop.

Railroad operator

CSX

Corp,

agriculture giant

DuPont Co.

and others

are analyzing voting data and adopting new marketing techniques to

target individual investors in corporate elections over everything

from board makeup to executive pay.

CSX, stung by defeat in a campaign

against activists, jazzed up its shareholder mailings and now even

plants trees to encourage individuals to vote. DuPont launched an ad

blitz aimed at small shareholders as part of its successful effort to

fend off activist investor Trian Fund Management LP. And

Humana Inc.

hit the

phones to secure enough votes for its proposed merger with

Aetna Inc.

To win over those shareholders, companies are borrowing

tactics from the political realm, where voter turnout may help

determine who becomes the next president, said

Eric Cantor, the former House

majority leader who is now vice chairman at investment bank

Moelis

& Co.

“A

retail investor is not too dissimilar to an unlikely voter who is not

registered,” he said. “The universe of voters is what matters. If you

expand the universe, you’ll be more successful.”

On their face, the costly

and time-consuming efforts don’t make a lot of sense given trends in

shareholding. A small number of big holders like

BlackRock Inc. control most shares and vote religiously.

Meanwhile, individuals who directly buy stock are shrinking as a

portion of the total pool of shareholders and often don’t even open

ballot packages before throwing them away.

But crucially, retail

shareholders tend to support management when they do vote. That makes

them attractive in close calls and in say-on-pay votes, where anything

less than 70% support can raise red flags for governance watchers and

activist investors looking for an opening.

Take Jacksonville,

Fla.-based CSX. In 2008, it lost a bitter challenge from two activist

hedge funds that wanted to split the chief-executive and chairman

roles and change the company’s compensation structure. Since then, it

has been keen to woo retail investors, who own about 30% of the

company’s stock, said Mark Austin, CSX’s assistant corporate

secretary.

Three years ago, the

company sought help from

Broadridge Financial Solutions Inc., which prepares, ships and

counts most of the proxies U.S. companies send out each year.

Broadridge also taps its database to develop profiles of likely

voters.

Broadridge redesigned

CSX’s proxy packaging, replacing formerly nondescript black and white

documents with ones featuring trains streaking across sunlit fields.

The packaging also prominently displays messages encouraging

shareholders: “Exercise our *Right* to Vote.”

CSX also now offers to

plant a tree for every registered shareholder who votes. Since 2013,

it has planted 18,459 trees, according to a company spokeswoman.

Mr. Austin of CSX

estimated that the company has spent hundreds of thousands of dollars

on the expanded packages. He says it wanted to boost retail voting to

“reduce the likelihood of unexpected results.” In 2015, 22% of CSX’s

retail shares were voted. That’s up from 20% in 2013 but still below

average.

|

Eric

Cantor of Moelis & Co. says, ‘A retail investor is not too

dissimilar to an unlikely voter who is not registered.’, and

former House majority leader, speaks while delivering closing

remarks at t

Photo: Andrew Harrer/Bloomberg News

|

|

Humana last fall needed approval from 75% of its shares outstanding to

proceed with its planned sale to Aetna. To pick up insurance votes,

its proxy solicitor, D.F. King & Co., made more than 40,000 calls,

according to a person close to the deal. In the end, the vote wasn’t

close, with Humana shareholders overwhelmingly approving the deal.

(Before it can happen, the proposed tie-up still needs approval from

regulators.)

Proxy solicitors caution that big investors still hold sway in

corporate elections. Individual investors held just 34% of shares in

U.S. public companies in 2015, down from 39% in 2008, Broadridge

says. And getting smaller shareholders to participate is no easy

task. Mom-and-pop investors collectively voted just 28% of their

shares in 2015, down from 32% in 2008.

Still, the efforts to mobilize them show that measures to improve

corporate governance—such as making directors stand for election each

year and giving investors a nonbinding vote on executive pay—may be

making companies more accountable to all shareholders.

Meanwhile, activist investors have grown in influence and the pension

and mutual funds that once could be counted on to support management

have become more demanding, meaning smaller shareholders are

increasingly important for companies under attack.

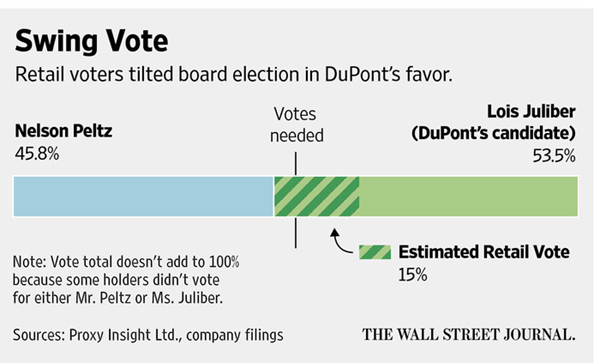

DuPont’s ability last year to use retail shareholders to help fend off

Trian has been widely discussed among companies looking for advantages

against activists.

Trian wanted a breakup of DuPont and board seats, including for its

co-founder

Nelson Peltz. The company’s

outreach included tailored mailings to retail investors, which held

about 30% of the stock, and ads in hometown papers in Wilmington,

Del. About half those shares voted in the contest—overwhelmingly in

favor of DuPont’s chosen slate of directors.

When DuPont eked out a win by less than 6% of shares outstanding, Mr.

Peltz credited retail voters.

|