THE

WALL STREET JOURNAL.

Markets

New Wall Street Conflict: Analysts Say ‘Buy’ to Win Special Access

for Their Clients

Securing face time for investors with top executives has become a

vital revenue source for securities firms; ‘brand ambassadors’ at

Coach

|

Coach’s headquarters in New York City in May. The luxury handbag

maker doesn’t let analysts who have a sell rating on its stock

host private meetings between their investor clients and top

Coach executives.

PHOTO: MICHAEL NAGLE/BLOOMBERG NEWS |

By

Serena Ng and

Thomas Gryta

Updated Jan. 19, 2017 11:31

a.m. ET

Analysts who want top

executives at Coach Inc. to

attend private events with their investor clients have to show they

are “brand ambassadors,” as the luxury

handbag retailer dubs it. You can’t be a brand ambassador

if you have a sell rating on Coach’s stock.

Coach investor-relations chief

Andrea Resnick says it takes that approach because of “the sheer volume of

requests” from analysts to have its management meet mutual funds, hedge funds

and other clients. Coach can’t say yes to everyone, she adds, so it has to

decide who gets access—and who doesn’t.

In 2003, a

$1.4 billion settlement between Wall Street securities firms and

regulators sought to eradicate conflicts of interest that led analysts to issue

overly positive research on companies, a phenomenon designed to help win

investment-banking deals. More than a decade later, the impact of the settlement

has helped exacerbate another set of potential conflicts.

Securities firms have struggled ever

since the settlement to make their research profitable. As a result, analysts’

relationships with company executives, including the ability to line up private

meetings for investor clients, have become an increasingly vital revenue source.

And that is increasing the pressure for analysts to be bullish on the publicly

traded companies they follow.

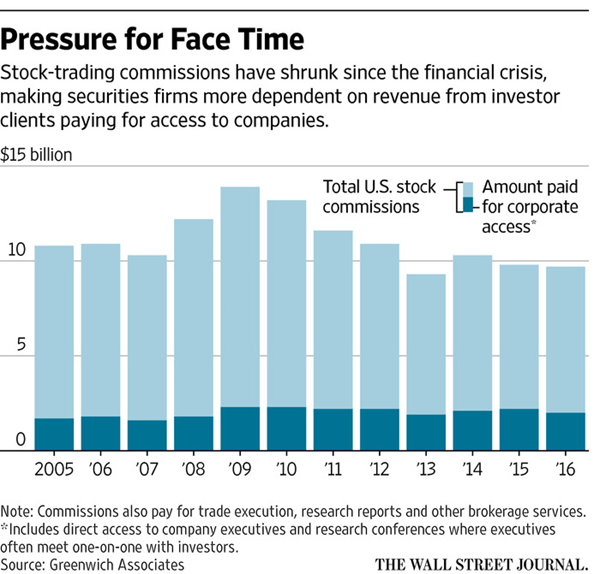

U.S. investors paid $2 billion in

brokerage commissions for corporate access in 2016, or more than a third of all

the money spent on stock research and related services, according to consulting

firm Greenwich Associates.

Many securities firms tally the

number of times their analysts take company executives on the road to meet

clients and use the number to help decide analysts’ annual bonuses.

At some firms, as much as one-third

of analysts’ yearly pay can be tied to corporate access, says James Valentine,

the founder of training and consulting firm AnalystSolutions LLC. Analysts

generally earn in the six figures a year, but pay ranges widely by experience

and securities firm.

Current and former analysts say

those forces can cause them to err on the side of producing rosy research

reports rather than jeopardize lucrative relationships with investor clients.

“It’s a decision I have to make on

my sell-rated stocks: whether I will forgo the opportunity for corporate access,

which clients will explicitly pay for,” says Laura Champine, a retail analyst at

Roe Equity Research. Some previous bosses at other firms told her to “just drop

coverage” instead of putting out sell ratings, she says, while declining to

comment on where that happened.

“When your compensation is in part

based on how many meetings you set up in a given year, it’s really tough to

stick to your guns,” says Eric Hollowaty, a former analyst at Stephens Inc. who

covered consumer companies.

Warren Stephens, the securities

firm’s chairman, president and chief executive, says in a statement that

analysts at Stephens “are encouraged to stay true to their convictions…even if

it means less access for us.”

Analysts’ ability to arrange private

events with management for clients is just a “minor aspect of compensation,” he

says, adding that “turnover is very low among our analysts.”

A federal rule bars companies from selectively

disclosing material nonpublic information but doesn’t prohibit

private conversations with investors. Companies also are allowed to control how

analysts and investors get access to corporate executives. Mutual funds and

hedge funds, meanwhile, are happy to pay for the opportunity to pepper top

executives with questions out of earshot of rival investors, possibly

gleaning information to inform trading decisions.

Coach’s Ms. Resnick says any analyst

may meet one-on-one with management, even if the analyst has a sell rating.

About 50 analysts currently cover Coach, she adds, and it has held investor

events with analysts who have buy or neutral ratings. Such analysts make up the

vast majority of those with a rating on the stock.

Just 6% of the roughly 11,000

recommendations on stocks in the S&P 500 index are sell or equivalent ratings,

according to research firm FactSet.

Last year, Deutsche

Bank AG agreed

to pay a $9.5 million penalty to settle civil charges that the firm “published

an improper research report” from an analyst who kept a buy rating on

Big

Lots Inc. despite

telling some traders and hedge funds he had new concerns about the discount

retailer, according to the Securities and Exchange Commission.

|

A Big Lots store in Alhambra, Calif., on Thanksgiving morning.

Regulators suspended an analyst who kept a buy rating on Big

Lots despite telling some investor clients that he had new

concerns about the discount retailer.PHOTO: FREDERIC

J.BROWNAGENCE FRANCE-PRESSE/GETTY IMAGES |

Those qualms were based on

information from investor meetings with Big Lots management hosted by

the analyst.

The SEC said Deutsche Bank’s

performance-evaluation system for analysts “assigned significant weight to

analysts’ access to and relationships with the senior management of the

companies they covered and the feedback that the firm received from its

clients.”

Analysts received additional credit

for securing meetings with chief executive officers and chief financial

officers, the SEC said. The enforcement action didn’t conclude that the practice

of investors paying analysts for corporate access creates a potential for

conflicts of interest or other problems.

The Financial Industry Regulatory

Authority says securities firms need to be proactive about identifying and

defusing conflicts of interest that could affect the objectivity of their

research analysts.

Amanda Williams, a spokeswoman for

Deutsche Bank, says the firm “takes its research analyst communications and

conduct very seriously and has a robust policy and control framework.”

The analyst, Charles Grom, paid a

$100,000 penalty to the SEC, was fired by Deutsche Bank and is serving

a one-year suspension from the securities industry. Mr. Grom and

Deutsche Bank didn’t admit or deny wrongdoing. The analyst’s lawyer, Patrick

Smith, said Mr. Grom had no comment.

Analyst recommendations often carry

weight with small investors, says John Bajkowski, president of the American

Association of Individual Investors, a nonprofit group with 180,000 members.

Most retail investors tend to lack sophisticated financial data and seldom dig

through corporate filings, he says.

Some hedge funds and smaller money

managers also get trading and investment ideas from analysts. “As much as we can

screen the fundamentals of a company, those analysts are going to know far more

than me and my colleagues,” says Kevin Mahn, president of Hennion & Walsh Asset

Management Inc., which oversees $800 million in investment trusts held mostly by

retail investors.

Upgrades and downgrades by analysts

often move stock prices, says Mark Bradshaw, a Boston College accounting

professor who has researched the securities industry. That is one reason why top

executives care deeply about what analysts are saying, investor-relations

officials say.

Mr. Valentine of AnalystSolutions, a

former analyst and managing director at Morgan

Stanley, now

coaches analysts across the industry.

Many of them have a goal of

increasing the number of “non-deal roadshows,” or marketing trips that aren’t

tied to specific corporate transactions or stock sales but feature analysts

taking executives to the offices of current and potential investors. The

meetings allow executives to pitch an analyst’s clients on the company’s

strategy and investment value.

More than 90% of companies go on

such roadshows, according to a 2014 survey conducted by the National Investor

Relations Institute trade group.

Banks and brokerages often poll

large investors on the services they value most highly. Private meetings

arranged by analysts are cited among the top reasons why investors steered

trades through the banks and brokerages.

That decision is important because

commissions from such trades are part of the lifeblood at many financial firms.

Competition has intensified since the financial crisis because the pool of

available commissions is shrinking from price cuts and the rise of automated

trading.

Christopher King, a former Stifel

Financial Corp. analyst,

recalls asking Sprint Corp. for meetings with clients when he had a hold rating

on the wireless telecommunications company a few years ago. He says a Sprint

investor-relations officer asked why it should oblige when he didn’t have a buy

rating.

Two analysts who still follow Sprint

say their investor-meeting requests also were been rebuffed when their ratings

were negative. Twenty analysts have a buy or hold rating on Sprint, while nine

rate the stock a sell, according to Thomson Reuters.

Sprint’s head of investor relations,

Jud Henry, says he doesn’t recall telling analysts that they wouldn’t get

corporate access because they didn’t have a buy rating on the company. He says

Sprint executives recently attended conferences hosted by analysts with neutral

and sell ratings.

Meredith Adler, a longtime

retail analyst who retired from Barclays PLC

in early 2016, says companies sometimes reacted to sell ratings by cutting

analysts off, which was “a hardship because your questions go unanswered and

you’re deprived of information,” she adds.

The former analyst recalls that

Family Dollar Stores Inc. wouldn’t let analysts with negative ratings take

executives on the road to meet with investors, though the discount retailer

would still maintain contact with those analysts.

Family Dollar was acquired by Dollar

Tree Inc. for

about $9 billion in 2015. Randy Guiler, Dollar Tree’s head of investor

relations, says the company considers executives’ availability, analysts’

ratings and other factors when making decisions about corporate-access events.

Media analyst Richard Greenfield of

BTIG LLC says his emails, phone calls, and a request for an investor meeting

with Walt

Disney Co. have

gone unanswered since he issued a sell rating on the company in December 2015.

The rating went out on the same day

as the world-wide release of “Star

Wars: The Force Awakens.” Before then, when Mr. Greenfield had a buy

rating on the stock, he was regularly invited to Disney events and once hosted a

meeting between a group of investors and a Disney executive, the analyst says.

“Everything changed when we went to

a sell,” says Mr. Greenfield. When Disney invited more than 50 analysts and

investors to the opening of its Shanghai

Disneyland resort last summer, Mr. Greenfield was left out.

Disney did invite Barclays analyst

Kannan Venkateshwar, who had an “underweight” rating on Disney last spring,

according to people familiar with the matter.

In November, Mr. Venkateshwar

boosted his Disney rating, and he is scheduled to hold an investor meeting with

Disney next month, one of the people says.

David Strasser, a former retail

analyst at Janney Montgomery Scott LLC, says some investors told him they had

little interest in his research and were only paying for meetings he could set

up with companies.

“I wanted to be valued for my

analytical abilities, but arranging meetings became such a critical part of the

job,” says Mr. Strasser, adding that he was sometimes asked to sit outside the

room so investors could ask questions without him. In 2015, he left the research

industry to join a venture-capital firm.

When Steve West was an analyst

covering restaurants and grocery chains, many companies did roadshows only with

analysts who had buy ratings, he says. Corporate access “became part of the

overall calculus,” he adds.

Mr. West is trying to change things

now that he is Panera

Bread Co.’s vice

president of investor relations. He says Panera’s policy is that all analysts

can get their clients face time with management regardless of their rating on

Panera’s stock.

“It shouldn’t be a popularity

contest,” he says.

Write to Serena

Ng at serena.ng@wsj.com and

Thomas Gryta at thomas.gryta@wsj.com