Forum participants were encouraged to consider appraisal rights in

June 2013 as a means of realizing the same long term intrinsic

value that the company's founder and private equity partner sought

in an opportunistic market-priced buyout, and

legal research of court

valuation standards was commissioned to support the required

investment

decisions.

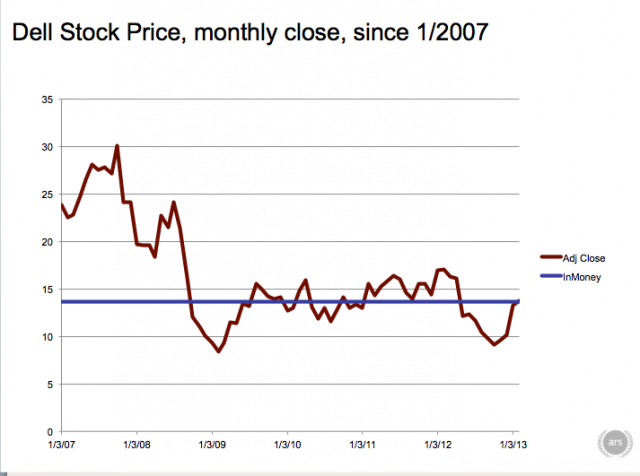

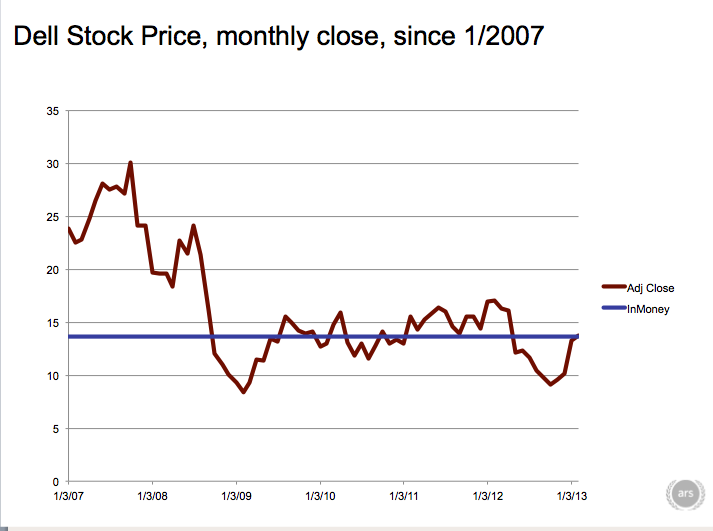

Each of the Dell shareholders who chose to rely upon the Forum's

support satisfied the procedural requirements to be eligible for payment

of the $17.62 fair value, plus interest on that amount compounding since

the effective date at 5% above the Federal Reserve discount rate.

Note: On December 14, 2017, the

Delaware Supreme Court

reversed and remanded the

decision above, encouraging reliance upon market pricing of the

transaction as a determination of "fair value." The Forum

accordingly

reported that it would resume

support of marketplace processes instead of

judicial appraisal for the realization of intrinsic value in

opportunistically priced but carefully negotiated buyouts.

For Dell Inc.

communications with employees relating to the views reported in the

article below, see

While Dell CEO Michael Dell and many at the top of the Dell executive

ladder stand to make out well in a move to take the company private, some

rank-and-file employees and mid-level executives are grumbling about how

the deal affects them. That's because Dell, which has used stock options

and restricted stock heavily as an incentive for employees in the past, is

simply cancelling many of the stock options it has awarded to employees if

the go-private deal is completed.

In

an internal e-mail to employees obtained by Ars Technica, the company

announced pending changes to its Long Term Incentive (LTI) program. Dell

plans to pay out the difference between the exercise price of options and

the $13.65-per-share go-private price to employees whose options were "in

the money"—with exercise prices below $13.65 per share. But options that

are "underwater"—issued when Dell's stock price was above $13.65—will

simply be cancelled.

"Upon closing of this proposed transaction, which is subject to

shareholder approval and other customary closing conditions, Dell will be

owned by Michael and Silver Lake, and shares of Dell will no longer be

traded publicly," the e-mail to employees said. While the company will

"continue to offer market-competitive compensation," the change means that

Dell's previously stock-heavy incentives for employees will have to be

converted to something else. And that means employees who hold a stake in

the company right now—or the promise of one—will be left with

significantly less than they may have hoped for.

That's part of a continuing theme for Dell employees who had bought into

the promise of working for a publicly traded company. In October, Dell

forced some employees who had heavily invested in Dell stock as part of

their 401k plans to sell off that stock at $9 a share—a move based on a

policy change.

Playing the

option

The use of stock options by corporations to reward employees—and

executives in particular—has long been controversial. Michael Dell and

other corporate executives made millions off of stock options in the 1990s

and the first half of the last decade—in part because of long-running

accounting fraud that

covered up kickbacks from Intel for exclusively using its processors.

But as the company has used stock and cash to acquire other companies to

create its software and enterprise services businesses over the past six

years, many of those employees who came onboard in the process have ended

up with stock options they couldn't use—because they were issued when

Dell's stock was high but vested after the stock had descended. And as

Dell moves to go private, those who held on to "underwater" options in the

hopes of a better future are cut out of the deal.

Enlarge/ For

employees who got performance options when the company's stock was over

$13.65, those options get converted to a hearty handshake.

And those options aren't insignificant. In 2009, Dell took an expense of

$106 million to accelerate the vesting of stock options it had given to

employees that were underwater—options for 20.9 million shares that had

been issued to employees with an average exercise price of $22.03 a share.

If they had been exercised, they would have amounted to more than 1

percent of Dell's outstanding shares—shares Dell would have had to buy

back from investors to award to employees.

Dell employees who were awarded Restricted Stock Units (RSUs) as part of

their compensation will get some cash out of the buyout—but

probably not what they had expected. RSUs will be converted to cash if the

deal goes through, but they will still be locked into Dell's vesting plan.

That means that in five years, if Dell goes public again at a higher stock

value, those who had RSUs will still just get paid out at $13.65 per

share.

When asked about the changes, a Dell spokesman referred to the

company's SEC filings, in which it said details on new long-term

incentive programs and other compensation would be finalized after the

deal is complete. "Our intent is for all of our team members to feel that

the new program is equal to or better than the prior programs," Dell said

in its public message to "team members."

Sean Gallagher / Sean is Ars Technica's IT

Editor. A former Navy officer, systems administrator, and network

systems integrator with 20 years of IT journalism experience, he lives

and works in Baltimore, Maryland.

This project was conducted as part of

the Shareholder Forum's public interest program for "Fair

Investor Access," which is open free of charge to anyone

concerned with investor interests in the development of

marketplace standards for expanded access to information for

securities valuation and shareholder voting decisions.

As stated in the

posted

Conditions of Participation, the

Forum's purpose is to provide decision-makers with access to

information and a free exchange of views on the issues

presented in the program's

Forum Summary. Each

participant is expected to make independent use of

information obtained through the Forum, subject to the

privacy rights of other participants. It is a Forum

rule that participants will not be identified or quoted

without their explicit permission.

The management of Dell Inc. declined the

Forum's invitation to provide leadership of this project,

but was encouraged to collaborate in its progress to assure

cost-efficient, timely delivery of information relevant to

investor decisions. As the project evolved, those

information requirements were ultimately satisfied in the

context of an appraisal proceeding.

Inquiries about this project

and requests to be included in its distribution list may be

addressed to

dell@shareholderforum.com.

The information

provided to Forum participants is intended for

their private reference, and permission has not

been granted for the republishing of any

copyrighted material. The material presented on

this web site is the responsibility of

Gary Lutin, as chairman of the Shareholder

Forum.

Shareholder

Forum™

is a trademark owned by The Shareholder Forum,

Inc., for the programs conducted since 1999 to

support investor access to decision-making

information. It should be noted that we have no

responsibility for the services that Broadridge

Financial Solutions, Inc., introduced for review

in the Forum's

2010 "E-Meetings" program and has since been

offering with the “Shareholder Forum” name, and

we have asked Broadridge to use a different name

that does not suggest our support or

endorsement.

{kind=link}