People with knowledge of that merger proxy

note it will clearly show, not just the blow by blow of the deal

making, but the extreme challenge and unpredictability that Dell is

dealing with as its personal computer business faces increased

competition from tablets and smartphones and PC makers such as

Lenovo, who happily operate on margins of as little as 2 percent.

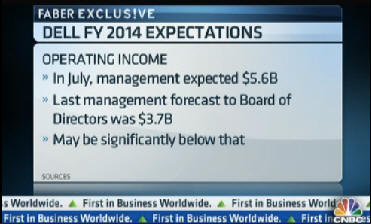

That volatility is best encapsulated by

one detail expected to be in the proxy. In July, the management plan

presented to the board called for operating income of $5.6 billion in

the current fiscal year 2014. Now, sources say the oft-revised

forecast, which most recently called for $3.7 billion, may be revised

significantly below that.

While Dell has spent over $13 billion on

acquisitions over the last five years designed to move it away from

reliance on PC's, they still represent roughly 66 percent of the

company's $56.9 billion in revenues. Sources familiar with the

situation say the proxy will cite the July plan as evidence of how

fast things have changed.

That three year plan, presented by

management prior to Michael Dell's engagement on a potential deal, was

a bottoms-up view of the business and its prospects that predicted an

increase in revenues and margins in fiscal year 2013—ended this

January—and beyond.

Only three weeks later, that three year

plan proved far too ambitious when Dell badly missed revenue and

earnings per share guidance for its second quarter. It wasn't long

after that, after discussing the idea with his neighbor in Hawaii,

George Roberts of KKR, that Michael Dell approached the company about

the possibility of a management led buyout.

A special committee of directors was

formed to negotiate with Dell and one of its first acts was to try to

get a handle on what the company was really worth. A new financial and

strategic forecast was provided by a small number of finance officials

in September. But as Dell's performance continued to deteriorate

through the fall, even that plan, which called for far lower margins

and revenues than the July plan, but still forecast $4.2 billion in

fiscal year 2014 operating income, seemed optimistic.

People familiar with the matter say the

Special Committee then made the unusual choice of turning to the

consulting firm of BCG to help it understand the future of the PC

business and the prospects for Dell to successfully transform itself.

BCG eventually gave the Special Committee an appraisal that assumed

Dell, even with margin improvement and cost savings, would not

generate operating income above $4 billion for years to come, and

would post roughly $3.4 billion in operating income this fiscal year—a

number that now looks optimistic.

As for the process itself, according to

people familiar with the matter, while Silver lake and KKR were the

first private equity firms to discuss a deal with Michael Dell, who

began this process on August 16, the idea of an LBO was first proposed

to him by Southeastern Asset Management last June, which indicated it

would desire rolling its equity into any transaction.

While KKR initially bid between $12 and

$13 a share, when first indications were received in late October, it

dropped out by early December without a follow up bid. Silver Lake

meanwhile started as low as $11.22 a share before slowly working its

way up to the $13.65 deal price.

None of this is to say the Dell deal will

get done at that price if at all. Shareholders are likely to read

things in the proxy that justify their perspective. And perhaps the

greatest single impediment to the deal is the market itself. As shares

of another troubled computer maker

Hewlett Packard have soared this year and its multiple along with

it, investors have gained confidence that Dell is simply worth more.

Still, the actions of a special committee

trying to navigate not just a typically conflict ridden process, but a

business that continues to change very quickly, and not for the

better, should provide for insight into a deal battle for the ages.

—By CNBC's David Faber; Follow

him on Twitter

@DavidFaber

|

© 2013

CNBC LLC. All Rights Reserved |