|

THE WALL STREET JOURNAL.

|

TECHNOLOGY | Updated August 2,

2013, 7:34 p.m. ET

Dell Reaches New Deal With

Founder

Agreement With Michael Dell,

Silver Lake Would Amend Voting Rules, Add Special Dividend |

|

By

DAVID BENOIT, KIRSTEN GRIND and

SHARON TERLEP

Relenting to pressure from all

sides, Michael

Dell agreed Friday to personally pay more to take ownership of the

company that bears his name.

|

Alexander F. Yuan/AP Photo

Michael Dell, Chairman and CEO of

Dell Inc.

|

|

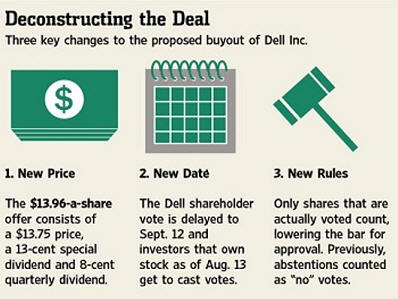

Mr. Dell and his partner on the

deal, private-equity firm Silver Lake, are now offering a 13-cent special

dividend to shareholders, plus a raised price of $13.75 for each share. The

increases add $350 million to what had been a $24.4 billion deal for Dell

Inc.

In exchange, the special Dell

board committee negotiating the deal agreed to adjust the shareholder voting

rules in ways that advocates and critics of the takeover alike say should

help it get across the finish line.

Mr. Dell himself is funding the

special dividend, according to people familiar with the deal.

The buyout, controversial with

Dell shareholders since it was announced in early February, still isn't

assured. Investor

Carl Icahn, its most-vocal detractor, on Thursday filed suit in Delaware

Court of Chancery seeking to bar any change in voting rules. A hearing on

that case is scheduled for Monday, Aug. 12, according to people involved in

it.

On Friday, Mr. Icahn said "an

increase of a mere 13 cents is an insult to shareholders" and he said the

special committee "is improperly putting its thumb on the scales in favor of

Mr. Dell's offer."

It is unclear if shareholders

will be satisfied with and pass the improved offer. Mr. Icahn, for one, has

argued the voting changes could in fact generate additional "no" votes.

Franklin Mutual Advisers, one of

Dell's large institutional investors, plans to vote in favor of the new Dell

deal, Peter Langerman, Franklin's chief executive said Friday. "We're not

jumping up and down," said Mr. Langerman, who said Franklin earlier voted

against the buyout. "But if the vote were today or tomorrow we would say

yes."

Mr. Langerman and his team met

with Mr. Dell last month and aired their concerns about the deal and its

price, he said. "We were quite vocal in terms of dissatisfaction with the

process and the price," Mr. Langerman said. Franklin is a unit of

money-manager

Franklin Resources Inc.

Donald Yacktman, president of

Yacktman Asset Management, said Friday he still opposes the Dell buyout.

"From the word go, we've made a statement about where we've stood and we're

not going to change that," said Mr. Yacktman, whose firm is also a large

Dell shareholder.

Relenting to pressure

from all sides, Michael Dell agrees to personally pay more to take

ownership of the company that bears his name. David Benoit

reports. Photo: AP.

Michael Dell and Silver

Lake struck a new deal with Dell's special committee. Could this

be final chapter in the Dell saga? David Benoit joins MoneyBeat

with details. Photo: AP.

|

|

The fabric of the new deal shows

the determination of Mr. Dell, the company's founder, chairman and chief

executive, to see it through. Last week the buyout group had offer to raise

its $13.65 bid to $13.75, saying it was their "best and final" offer. In his

own letter to shareholders last week Mr. Dell said, "I am at peace either

way and I will honor your decision."

Mr. Dell and the partner heading

the deal for Silver Lake, Egon Durban, spent time at their nearby homes in

Hawaii working out new terms, said people familiar with the talks.

The new deal also calls for a

third-quarter dividend of eight cents a share that might not have been paid

had the buyout closed according to an earlier schedule.

The buyout group proposed the

eight-cent payout on Wednesday, according to a person familiar with the

matter. The Dell board said the quarterly dividend wasn't enough, and by

Wednesday evening they'd agreed on adding the 13-cent special dividend,

people familiar with the matter said. The details were hammered out late

into Thursday night.

All in, the offer-price increase

and the dividends amount to a value of $13.96 a share for holders not

affiliated with Mr. Dell, a 2.3% increase from the original offer. Dell

shares rose 5.6% to $13.68 in Friday trading, the highest since April and a

sign investors think the deal will get done.

Dell shareholders will get a

chance to vote on the new proposal on Sept. 12. Friday's deal also includes

a new "record date," of Aug. 13, the date that determines which Dell

stockholders can cast votes on the deal.

The voting-rule change means only

shares that are actually voted count, altering an earlier clause that had

abstentions counting as "no" votes. That clause proved problematic when

turnout for the vote wasn't as high as the buyout group and special

committee had hoped. When they didn't have the confidence they had the votes

to get the deal passed, the special committee delayed the vote twice.

Alex Mandl, chairman of the

special committee, said Friday the new voting standard is "in the best

interests of Dell shareholders" and "has enabled us to secure substantial

additional value." He said the voting change was warranted because when the

sides struck a deal there was only a choice between "a going-private

transaction and a continuation of the status quo."

Now, he says, the "nature" of

shareholders' choice has changed because an alternative has emerged, a

reference to Mr. Icahn's competing plan for Dell to borrow and pay out money

to shareholders.

Southeastern Asset Management

Inc., aligned with Mr. Icahn in the fight, responded it was "amazed" at Mr.

Mandl's justification, saying he was using their opposition to justify

lowering the voting requirement for Mr. Dell and Silver Lake.

A new record date could also help

the buyout group by attracting short-term shareholders, known as merger

arbitragers, who buy shares with the hopes of securing gains when deals get

completed.

Dell, founded by Mr. Dell nearly

30 years ago, has struggled to keep pace with the latest technology trends.

Mr. Dell has envisioned refocusing the company on serving corporate clients

rather than selling consumer computers. Shareholders who have protested the

deal have had many of the same goals but felt the original $13.65-a-share

price undervalued the company and that the buyout unfairly cut them out of

potential upside in any Dell revival.

The resistance to the original

deal proved more than Mr. Dell could overcome, even as certain key

developments went his way. In April, industry-research firm IDC issued a

surprisingly bleak report on global PC shipments, potentially lending

credence to the board's inclination to sell the company.

Later that month, private-equity

giant

Blackstone Group LP, which had considered an offer greater than $14.25 a

share, backed away after getting spooked at Dell's business prospects during

due-diligence research. That move, and the lack of any other bidders for the

whole company, gave the committee and buyout group leverage to say no higher

offer was in sight. Then in July three shareholder-advisory firms urged

investors to take the $13.65-a-share offer.

Still, all of these favorable

factors weren't enough to overcome the assault by Southeastern and Mr.

Icahn. The investing pair have said if the buyout vote failed, they would

put up their own slate of directors at Dell's annual meeting to try to oust

the board, including Mr. Dell. They have proposed a plan in which the

company would borrow money and pay shareholders $14 a share and a warrant

for as many as 1.1 billion shares out of about 1.76 billion shares

outstanding.

They have urged Dell's board to

hold the buyout vote at the same time as the annual meeting, to give

shareholders an option to choose their proposal, Mr. Dell's, or neither.

On Friday morning, the Dell board

made clear it had no such intentions, setting the annual meeting for Oct.

17.

—Shira Ovide, Peg Brickley and Joann S. Lublin

contributed to this article.

Write to David

Benoit at

david.benoit@dowjones.com, Shira Ovide at

shira.ovide@wsj.com and Kirsten Grind at

kirsten.grind@wsj.com

A version of this article

appeared August 3, 2013, on page B1 in the U.S. edition of The Wall Street

Journal, with the headline: Michael Dell Sweetens Offer.

|

Copyright ©2013 Dow Jones & Company, Inc.

All Rights Reserved |

|

![[image]](http://si.wsj.net/public/resources/images/BF-AF497_DELL_NS_20130802181204.jpg)