Darden Restaurants has

so successfully reduced investors' appetites that even last Friday's

meager results were enough to send the company's shares modestly

higher. Happily, more sustenance could be on the way.

First, the morsels that

the owner of Red Lobster, Olive Garden, and LongHorn Steakhouse

doled out last week: It reported that fiscal third-quarter sales

rose 4.6%, to $2.26 billion, but that was due to new restaurant

openings and last year's acquisition of Yard House, a beer and

burger chain. Earnings fell 18%, to $134.5 million, as did earnings

per share, which came in at $1.02. Same-store sales at its three

biggest and best-known chains dropped 4.6%, dragging down margins

and profits.

|

Alan Diaz/Corbis

|

|

More important, however, the company is following a new operating

recipe designed to reverse the margin contraction and earnings

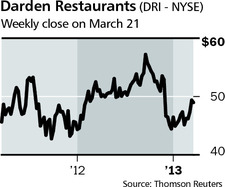

declines that have pulled the shares down 13% from last fall's peak.

In addition to cost-cutting, it wants to slow the growth of some of

its more mature brands while pushing harder on its newer,

faster-growing chains. Some think the company isn't going far enough

and that more changes could unlock a roughly 35% gain in the stock

over the next year or two.

Darden (ticker: DRI) took pains to tamp down expectations

at a February analyst meeting. By last week's report, analysts

expected the company to report $1.01 a share, down from the $1.13 a

share they'd been anticipating prior to the sessions with the

company. Similarly, analysts now project fiscal 2013 earnings of

$3.16 a share, down from about $4.10 a year ago.

Encouragingly,

investors chose to focus on the fact that the fiscal third-quarter

results were a penny better than the lowered forecasts. They also

took note when executives alluded to recent comments from industry

tracker Malcolm Knapp, who has been upbeat about March results at

U.S. restaurants. That would be a welcome break from February, when

casual-dining restaurant sales were down 5.4% industrywide, hurt by

higher payroll taxes, poor weather, and higher gas prices.

Orlando, Fla.–based

Darden gets the largest share of its revenue from Olive Garden,

whose 818 restaurants contribute 44% of sales. The chain's falling

same-stores sales were a concern when we wrote positively about the

company a year and a half ago ("Darden

Offers Investors a Tasty Treat," Nov. 14, 2011), and they remain

a worry today. Red Lobster, with 705 outlets, kicks in 32% of

revenues, and LongHorn's 416 restaurants generate 14% of revenue.

The latter have held their market positions.

Darden is working to

turn around its largest brands by limiting the extent of menu-price

increases and reducing the number of new restaurants. For example,

Olive Garden will open 15 new stores in fiscal 2014, down from 36

this year. The company already has kicked off a cost-cutting program

that has resulted in about $130 million in annual savings, which

will grow to $170 million to $195 million a year.

Simultaneously, Darden

wants to promote its smaller, lesser-known but faster-growing

brands. In addition to Yard House, they include Bahama Breeze, Eddie

V's, Capital Grille, and Seasons 52. With mostly positive same-store

sales and room to open new restaurants, the specialty group now has

168 restaurants that represent about 10% of sales.

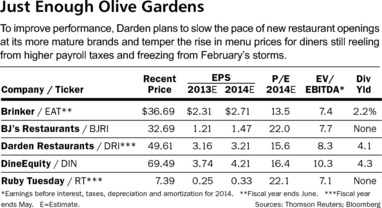

The Bottom Line

If Darden cuts menu

prices and costs, its shares could rise 35% to $66. |

|