Corporate

Governance,

Management

What Is It Like to Be

Owned by Warren Buffett?

A new survey reveals

Berkshire’s management style.

October 29, 2015 | by Shana Lynch

For

many companies, there’s a bit of magic to being bought by Warren

Buffett’s Berkshire Hathaway. The company’s “Powerhouse Five,” its

largest noninsurance businesses,

recorded $12.4

billion in pre-tax earnings last year, up nearly 13% from

the previous year. Its smaller companies also grew, increasing 8% over

the year.

Of

course, not all his bets

have paid off

(think Tesco and Dexter Shoe). But from an outsider’s perspective,

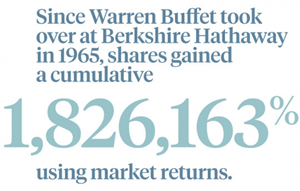

Berkshire’s strategy has been a wild success. Using market returns,

shares gained a

cumulative

1,826,163% since Buffett took the reins in 1965.

But

what does it look like from the inside? Stanford Graduate School of

Business professor

David F. Larcker

and Stanford GSB researcher

Brian Tayan

surveyed approximately 80 Berkshire subsidiary CEOs to determine how

Buffett’s

acquisition and

management style translates on the ground.

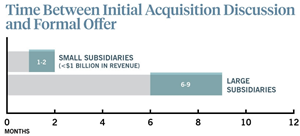

Acquisition Time

Acquisitions in general

can move quickly or take years, but Buffett moves fairly quickly when

he’s ready to buy. The CEOs of Berkshire’s smaller subsidiaries (less

than $1 billion in revenue) said about one to two months passed

between initial acquisition discussion and a formal offer. Larger

subsidiaries took longer — on average, six to nine months. Closing

times also lined up similarly: Smaller firms took between one to two

months to close, while larger firms took four to five months.

Immediate Changes

Most respondents said

their companies experienced few major governance changes following

their acquisitions. When there were changes, they were most often to

the board of directors or CEO compensation contracts. Insurance

subsidiary CEOs said they changed internal-audit and risk-management

practices. Of course, companies that had been publicly traded

eliminated their investor-relations departments.

Still, changes were

relatively few, the CEOs reported. One respondent noted, “The only

change is that I now discuss any major capital acquisitions with

Warren. We run the business the way we always have.”

Long-Term View

The subsidiary chiefs

also believe their companies’ performances are better under Berkshire

(and even better than if they were stand-alone companies). Respondents

point to Berkshire’s brand value and financial strength. Another

reason? Berkshire lets CEOs focus on a longer performance horizon than

they would expect under other ownership. Although each CEO varied on

what that horizon would be, with estimates ranging from three years to

50, they all said Berkshire management encourages a long-term focus.

Compensation

Another area of

agreement: Survey respondents think they’d be paid better elsewhere.

All say their annual bonus is calculated with two performance measures

(typically, larger corporations use 2.4 measures). Berkshire CEOs are

judged on metrics such as earnings, return on equity, and operating or

profit margins. None have their compensation tied to Berkshire’s stock

price, which is standard practice in many large companies.

Hands-Off Management

|

No one gives a

company this kind of freedom.

— Survey respondent

|

|

According to the survey,

Buffett lives up to his “delegation just short of abdication” style.

The CEOs provide monthly financial statements to headquarters, but

they have infrequent contact with Buffett. Most report having phone

calls with him on a monthly or quarterly basis. None have a

pre-established schedule, and all said they initiate the communication

themselves.

Buffett is also unlikely

to get involved in the affairs of their companies, the CEOs noted.

They would handle independently issues like labor disruptions,

supply-chain issues, legal action against the company, or modest

declines in sales. What would bring Buffett to the phone: anything

that impacts Berkshire’s reputation or a severe restatement of

previously reported financial results, respondents said. One CEO

noted, “No one gives a company this kind of freedom.”

Life Beyond Buffett

Each CEO who took the

survey agrees that common culture is shared across Berkshire’s

subsidiaries, and that culture — focused on honesty, integrity,

long-term orientation, and customer service — won’t change when

Buffett steps down. As one said, “The more I interact with the board

at Berkshire and other Berkshire managers, the more confident I am in

the future of Berkshire post-Warren.”

Read more about the

study published

by the Corporate Governance Research Initiative at Stanford Graduate

School of Business and the Rock Center for Corporate Governance at

Stanford University. David F. Larcker is the James Irvin Miller

Professor of Accounting and Brian Tayan is a researcher at Stanford

GSB.

Copyright © Stanford

Graduate School of Business

655 Knight Way, Stanford, CA 94305 |