Negative TSR Prompts

Hard Look at Exec Pay

By Matthew

Scott

February 22, 2016

Compensation

committees are undergoing serious reviews of pay strategies amid

falling stock prices and the realization that total shareholder return

(TSR) for a majority of companies could be negative.

With both the S&P

500 and the Dow Jones Industrial Average ending 2015 in negative

territory and continuing downward to start 2016, shareholder concerns

about executive compensation are starting to intensify as proxy season

unfolds. MSCI ESG Research reports that declining stock values

have resulted in the average one-year TSR for S&P companies’ falling

to negative 2.93%, the first time TSR has been negative since 2009.

Since investors have also seen four straight quarters of declining

earnings, companies should expect higher levels of scrutiny as to

whether executives’ 2015 pay is actually aligned with company

performance.

“We’ve had five

years of positive TSR growth and now companies need to be prepared for

a different environment when total shareholder return is flat or

declining,” says Irv Becker, national practice leader for

executive compensation at Hay Group.

Shareholder scrutiny

is likely to be more acute at companies where CEO pay appears to be

relatively high following multiple years of negative TSR and lagging

performance.

Becker and other

observers suggest negative TSR numbers may even impact some companies’

say-on-pay votes this proxy season.

“If stock prices and

earnings are down, it is reasonable to expect that shareholders are

going to be in a grumpier mood when it comes time to vote on pay,”

says Steve Kline, a director and senior compensation consultant

who specializes in pay-for-performance measurement and analysis at

Willis Towers Watson. “Shareholders are going to expect to see how

the performance declines have washed through the pay practices.”

Experts say

compensation committees should review how their current pay plans

compensate executives when stock price and performance are declining.

Additionally, they should consider how their companies will explain

their pay decisions, particularly if they expect questions from

concerned shareholders.

High Pay, Low

Returns

Companies across

many industries will see negative TSR numbers this year and possibly

next, so understanding how TSR metrics can affect compensation is an

issue for all boardrooms, whether they use it in their pay plans or

not.

A Frederic W.

Cook report published last December reveals that 54% of the top

250 companies in the S&P 500 are currently using TSR as a performance

metric in compensation plans.

On a broader scale,

Equilar last month reported that 48.7% of S&P 1500 companies

use relative TSR in their pay plans.

For companies

already using TSR as a measure in their pay plans, figuring out the

clearest way to explain the role it plays will serve as good practice

for the SEC’s pay-for-performance disclosure rules, as well as helping

boards prepare for engagements with investors.

Opinions about the

use of TSR have been mixed as pay plans have moved toward

pay-for-performance models.

Institutional

investors and proxy advisory firms favor the use of TSR as a way to

achieve pay-for-performance alignment with company outcomes over the

long term.

Company management

believes use of TSR as a metric can be overblown because executives

don’t have the same control over stock price as they have over other

metrics such as earnings or revenue.

“TSR provides

alignment with shareholder returns, but it’s not a direct reflection

of how well or poorly management is running the firm,” notes

Farient Advisors vice president Dayna Harris.

She points out that

broad market sell-offs and other factors can drive stock prices

downward, and executives fear their compensation could be cut

unfairly.

Equilar’s

director of research, Belen Gomez, agrees.

“If [an] executive

team hit absolute performance metrics, did everything in its power to

prevent disaster for the company, and the loss of value could have

been much worse, the company may end up with disgruntled executives

and retention could become an issue,” says Gomez.

A look at CEO pay

among several companies with negative TSR quickly reveals how complex

the pay landscape can be for both management and shareholders.

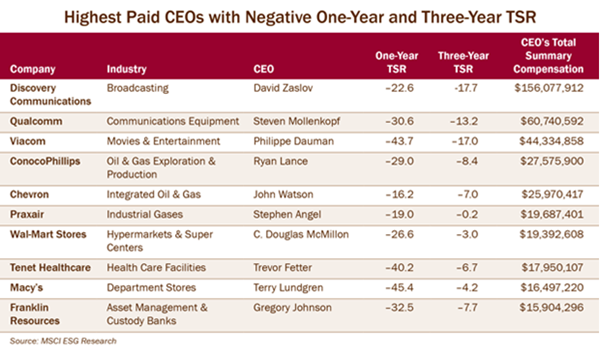

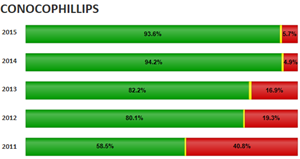

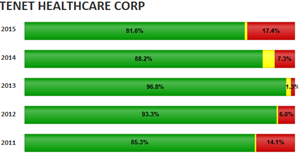

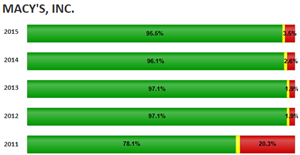

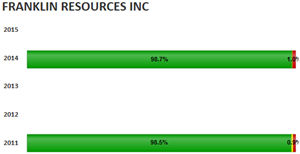

Ric Marshall,

head of MSCI ESG Research, identified a select group of companies for

Agenda that have registered negative TSR numbers over one- and

three-year periods. (Please see chart.)

Shareholders of

these companies have absorbed losses for at least three consecutive

years, yet the CEOs’ pay for 2014 appears to be generous considering

the period of poor performance. The combination of relatively high CEO

pay and three years’ worth of negative TSR should put these companies

on notice that they will likely attract shareholder scrutiny.

The numbers suggest

“these are companies that are already overpaying for previous bad

performance,” says Marshall. “If they continue to follow their past

patterns they may not be that responsive [to shareholders, and] they

may continue to overpay.”

For example, asset

manager

Franklin Resources compiled a

one-year TSR of negative 32.51% and a three-year average TSR of

negative 7.66%. Yet the board approved CEO Gregory Johnson’s

$15.9 million pay package in 2014, which included a $3.65 million cash

bonus.

By comparison,

Franklin Resources’ peer group of asset managers and custody banks

registered one-year TSR of negative 11.38%, and a three-year average

TSR of negative 49.31%. The annual average CEO pay for the group was

$6.2 million.

Even though Johnson

received more than twice the average CEO pay for the index and earned

a $3.65 million bonus, shareholder support for the company’s 2016 pay

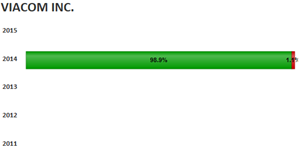

plan in a say-on-pay vote held on Jan. 8 was 99%.

“It is hard to

understand how they can continue to pay above the average for the

entire index even though the last several years of performance have

been as bad as they have, both relative to the market and relative to

their peers,” says Marshall.

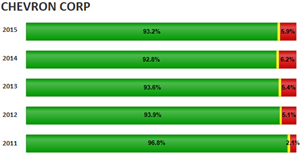

In the case of

Chevron, an oil and gas company,

negative TSR might be expected, given the way oil prices plunged in

the past year. Chevron compiled a one-year TSR of negative 16.21% and

a three-year average TSR of negative 7.01%. The integrated oil and gas

peer group registered one-year TSR of negative 13.86% and three-year

average TSR of negative 2.21%. The annual average CEO pay for the

group was $4.6 million.

Chevron addressed

its poor performance directly in its 2015 proxy statement. The board

justified Chairman and CEO John Watson’s $25.9 million

pay package on the basis of his meeting targets other than share price

because the entire industry had been impacted by lower oil prices, and

thus lower share prices.

In addition, $13.5

million of Watson’s pay is in the form of future equity grants. The

remainder is composed of basic salary of $2.1 million, a $3.1 million

bonus and $7.2 million in shares that vested during his previous six

years with the company.

There are other

compensation issues boards have to deal with in a negative TSR

environment other than explaining pay to executives and discussing pay

practices with shareholders.

As stock prices

decline, boards have to think about how they will grant stock in the

future.

Boards will have to

consider whether to give out more shares at lower prices to match the

value of the awards that were given in the previous year. Or boards

may decide to grant the same number of shares, regardless of the

price. In the former case, some companies may run the risk of running

out of shares in their stock plans.

“This is what

companies are struggling with right now,” Kline says. “We saw this in

2009 after the market tanked in 2008. Stocks were down 40%, so you had

to come up with some creative ways to make stock grants.”

Compensation

typically increases in the high single digits annually, but in a

negative TSR environment, pay increases may stall.

Andrew Gordon,

associate director of research services at Equilar, says executive pay

may flatten or even decline, depending on whether boards reduce bonus

payments and how lower stock prices affect the grant-date value of

equity awards.

However, Becker

counters that target compensation is likely to continue its upward

rise, whereas realizable pay may go down.

“What the

shareholders are going to see in the summary compensation table is

increasing comp,” he says. “Many companies will do an additional

disclosure that will show the real impact of the share price decline.”

|