|

THE

WALL STREET JOURNAL.

Markets

| Heard on the Street

CEO Bonuses: How Pro Forma Results Boost Them

Reported earnings faltered last year; to help set bonus payments,

many companies relied on pro forma measures

|

New York's Financial District. PHOTO: RICHARD DREW/ASSOCIATED

PRESS |

By

Justin Lahart

May 26, 2016 1:57 p.m. ET

Earnings before the bad

stuff can do good things for executive pay.

Last year was tough for

many companies, so many asked investors to imagine what things would

have looked like if the tough things had never happened. This led to

the

biggest divergence since 2009

between pro forma results, which exclude items such as restructuring

charges and stock-based compensation, and results under generally

accepted accounting principles, or GAAP.

But these adjusted metrics

aren’t just showing up in earnings releases. Pro forma figures have

been proliferating in annual proxy statements, too. There, when used

with compensation metrics, they can help executives draw bigger pay

packets.

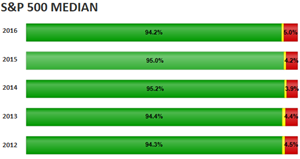

Research firm Audit

Analytics finds that the term “non-GAAP” appeared in 58% of proxies

for companies in the S&P 500 that have released them so far this year.

Five years ago, that term showed up in 27% of proxies for current S&P

500 constituents.

There is nothing improper

about using non-GAAP measures as long as they are disclosed properly.

And corporate boards decide on the measures they want to use for

compensation purposes. Plus, there is an argument to be made for

sometimes excluding items from results for compensation purposes. If,

say, a natural disaster hits a company with expensive repairs, perhaps

an adjustment is in order.

But other items that often

get excluded in pro forma results, such as layoff-related charges, do

seem like a reflection of management’s performance. And boards have

too often shown a willingness to set awfully low bars for executives

to clear.

That, though, can

disadvantage shareholders and wreck the idea of pay for performance.

In that vein, the dramatic rise in the number of companies using pro

forma measures to determine bonuses would indicate the balance between

shareholders and executives is being skewed in executives’ favor.

Indeed, an examination of

the most recent proxy statements from companies in the Dow Jones

Industrial Average shows about a dozen of the index’s 30 constituents

had annual pro forma earnings well in excess of GAAP ones and used the

pro forma ones in annual bonus calculations.

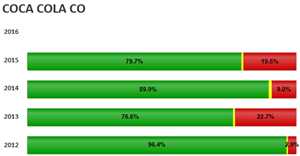

Coca-Cola’s pretax income increased

by 3% under GAAP. But after adjusting for the impact of the stronger

dollar and “nonrecurring items,” the income growth figure the Dow

component used for bonus purposes rose to 5.5%.

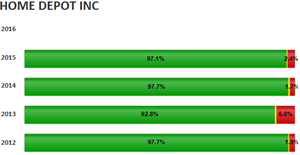

Absent adjustments, Dow

member

Home Depot

reported operating income of $11.77

billion last year. But the pro forma figure of $12.06 billion it used

for compensation figures excluded the impact of the strong dollar and

costs associated with

its 2014 credit-card data breach.

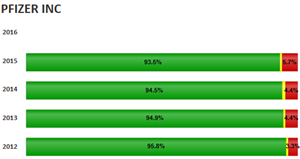

Pfizer

earned $1.11 per share last year under

GAAP. But the Dow component excluded a number of items from the pro

forma results it used for bonus purposes,

pushing earnings per share to $2.20—above

the $2.05 it had targeted for its annual incentive program. Without

that adjustment, the chief executive’s bonus under the company’s

annual incentive program could have been significantly lower. While in

most years, the pro forma earnings the pharmaceutical company has used

for compensation purposes have exceeded GAAP, in 2013 they were lower.

Several other Dow

components with pro forma earnings in excess of GAAP mentioned those

measures in their compensation discussion, but left it unclear how

they affected bonus amounts. Some used non-GAAP measures other than

earnings, such as economic profits, to set bonus amounts.

More worrisome, using pro

forma to set bonuses provides executives with an incentive to exclude

items not because they should, but to hit performance bogeys. That

creates a risk that pro forma results say less about a company’s

underlying health than about executives desire to get paid more.

Write to

Justin Lahart at

justin.lahart@wsj.com

|