|

THE

WALL STREET JOURNAL.

Business

Companies Routinely Steer Analysts to Deliver Earnings Surprises

With nudges and phone calls, analysts are urged to lower their

estimates, making it easier for companies to beat them; ‘a rigged

race,’ says Barry Diller

|

An

AT&T store in New York City’s Times Square. Before announcing

earnings in April, the company’s investor-relations employees

encouraged analysts to look back at an executive’s comments that

suggested revenue might be hurt because some customers were

waiting longer to upgrade their mobile phones. PHOTO:

RICHARD DREW/ASSOCIATED PRESS |

By

Thomas Gryta,

Serena Ng

and

Theo Francis

Aug. 4, 2016 11:58 a.m. ET

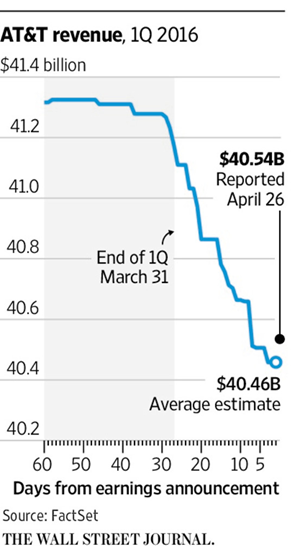

In April,

AT&T Inc.

shares rose after it

reported quarterly revenue that

narrowly topped the average estimate from analysts.

The

surprise wasn’t as surprising as it looked. Before AT&T’s

announcement, investor-relations employees at the telecommunications

giant encouraged analysts to look back at comments made by finance

chief John Stephens in early March, say analysts who spoke with the

company. He had implied some customers were waiting longer to upgrade

their mobile phones, an important revenue source.

Analysts at three research firms cut their sales estimates by an

average of about $1 billion in the week before AT&T issued

first-quarter numbers. William Blair & Co. analysts cited Mr.

Stephens’s comments. The average estimate of all 22 firms following

AT&T fell $323 million in three weeks, according to FactSet.

AT&T wound up reporting $40.54 billion in quarterly revenue, beating

the lowered target by $76 million.

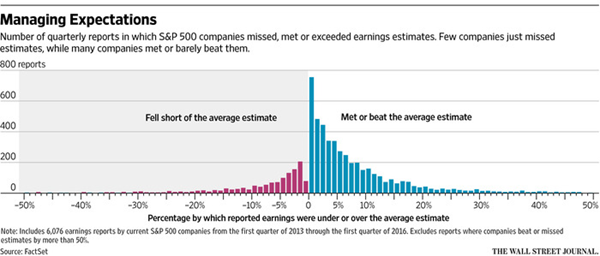

Quarter after quarter, about 75% of companies in the S&P 500 index

meet or exceed analysts’ earnings forecasts, a statistic that has held

up in good times and bad. One reason for such consistently impressive

results is that some companies quietly nudge analysts’ numbers, almost

always lower.

A

federal rule bars companies from

selectively disclosing material nonpublic

information but doesn’t prohibit private conversations in

which companies can gently push analysts in helpful directions, as

AT&T did.

“We

understand the rules, and we follow them diligently,” says Mike Viola,

senior vice president of investor relations at AT&T, based in Dallas.

Some analysts, investor-relations officials, securities lawyers and

executives say the signals have become so commonplace that the

all-important question of whether a company beat estimates is more

about theatrics than reality.

Companies send the signals to make themselves look better—and boost

their stock prices—even though their fundamentals haven’t changed at

all. And the signals often go to just a small number of analysts,

giving them and their investing clients a potentially unfair

advantage.

Media mogul

Barry Diller, chairman of

Expedia Inc. and IAC/InterActiveCorp,

says analysts and investor-relations executives work together to keep

estimates low. “It is a rigged race,” he says, adding that the problem

exists even at those two publicly traded companies.

An

analysis by The Wall Street Journal found that earnings estimates

often decline steadily after the end of a quarter. That can turn what

might have been an embarrassing “miss” for the company into a positive

surprise.

The

Journal examined daily changes in analysts’ estimates at S&P 500

companies since the start of 2013, comparing the estimates with what

the companies ultimately reported for each period.

Nearly 2,000 times from the start of 2013 through this year’s first

quarter, companies would have missed the average earnings estimate if

analysts hadn’t changed their numbers in the 40 trading days before

the company’s quarterly earnings report.

In

about one-fourth of the instances where companies would have missed

the average earnings estimate, the average projection fell enough that

the company wound up meeting or beating analysts’ expectations

instead, the Journal’s analysis shows. The 40 trading days cover the

period from when companies typically have a good sense of the

quarter’s performance to the day before earnings are announced.

Lowered earnings forecasts helped 66

companies, including

Citigroup Inc.,

Coca-Cola

Co.

and

Viacom Inc.,

each meet or exceed earnings expectations

during at least three of 13 quarters examined by the Journal.

CBS Corp.,

U.S.

Bancorp

and seven other companies met or beat reduced estimates

in about half the quarters.

Viacom says its analyst interactions are consistent with industry

practice. Citigroup says it provides financial updates at conferences

between earnings releases. Coca-Cola, CBS and U.S. Bancorp wouldn’t

comment.

The

opposite almost never happens. Companies wound up missing earnings

estimates just 1% of the time after being on track to beat them 40

trading days earlier, the Journal’s analysis shows.

The

stakes are high. In the past five years, the share price of companies

in the S&P 500 that fell short of analysts’ average earnings estimate

dropped 2.2% on average in the two days before and after reporting

quarterly results, according to FactSet.

Companies have different ways of coaxing analysts to shrink their

estimates. Investor-relations officials sometimes point out to

analysts where their estimates are in relation to other analysts.

Analysts whose forecasts are far from what companies end up reporting

risk losing credibility with clients and could get less access to

company management. Those are reasons to listen if a company calls

with a suggestion, according to analysts.

“Companies have called to ask if I was aware of their guidance and

incorporated it into my models,” says Jeffrey Harte, a banking analyst

at Sandler O’Neill + Partners LP in Chicago.

Roger Freeman, who left the stock-research industry in 2014 and now

works at a technology startup, says: “If someone is trying to get your

numbers down, they will highlight all the negatives and not positives,

and you’ll come away thinking: ‘Gee, that sounds pretty bad,’ and

sometimes take your numbers down.”

The

Securities and Exchange Commission says companies may privately

comment on analysts’ financial models as long as the companies are

correcting historical facts in the public domain or sharing “seemingly

inconsequential data,” even if analysts use the information to draw

significant conclusions.

The

SEC says companies shouldn’t use private discussions to selectively

communicate material nonpublic information “either expressly or in

code.” A federal rule called Regulation Fair Disclosure was adopted in

2000 to stop companies from leaking earnings forecasts to selected

analysts, who passed along market-moving information to their clients.

In 2010,

Office Depot Inc.

paid $1 million to settle SEC

allegations that the retailer had

selectively informed analysts that it wouldn’t meet their forecasts by

talking down analysts’ expectations in one-on-one phone conversations.

The

company’s shares tumbled after it began contacting the analysts, and

Office Depot ended up publicly disclosing a profit warning in a

regulatory filing.

The

SEC said Office Depot didn’t regularly make such calls to analysts.

The company didn’t admit or deny wrongdoing as part of the settlement.

|

An

Office Depot store in New Albany, Ind. In 2010, the retailer

paid $1 million to settle allegations that it selectively called

analysts to inform them that Office Depot wouldn’t meet their

financial forecasts.

Photo: Luke Sharrett/Bloomberg

News |

The

modern landscape of earnings announcements and consensus estimates was

created in the 1970s when federal regulators began requiring companies

to issue quarterly financial reports. In 1976, a unit of brokerage

firm Lynch, Jones & Ryan began collecting analysts’ earnings estimates

and tallying “surprises,” or results that beat or missed expectations.

At

least six firms now collect and disseminate estimates that often

include earnings per share, sales, profit margins and cash flow.

Investors usually focus much of their attention on revenue and profit

estimates.

Near the end of each quarter, an elaborate dance occurs between

analysts and companies. The companies want to avoid missing

expectations, and analysts are striving to come up with the most

accurate numbers.

Some companies refuse to have any contact with analysts. Matthew

Stroud, who used to run investor relations at

Darden Restaurants Inc., says he

wouldn’t answer calls from analysts before it reported results. He

tells companies he does consulting work with now to do the same.

Analysts “may pry and probe, and there’s the chance you could

inadvertently give someone a sense of tone around earnings,” says Mr.

Stroud, now at Arbor Advisory Group LLC, an investor-relations

consulting firm.

Johnson & Johnson

doesn’t field calls from analysts between quarter end

and its earnings release, though investor-relations personnel will

occasionally answer “fact-based questions” sent by email, the company

says.

Near the end of the first quarter, AT&T

steered analysts back to

Mr. Stephens’s comments at a

Deutsche Bank AG

conference on March 9, say five analysts who spoke to

the telecom company.

AT&T’s finance chief said last year’s fourth quarter included

“a slowdown in the handset upgrade cycle.”

He added that he “wouldn’t be surprised to see that continue.”

Jeffrey Kvaal of Nomura Securities says AT&T’s investor-relations team

“is very diligent” before earnings releases “about making sure that

the comments from the executives are reflected in the commentary from

the sell side.”

A

week before the announcement, Mr. Kvaal cut his first-quarter sales

estimate by $837 million to $40.54 billion, citing lower equipment

sales. Two days before the results, the William Blair analysts cut

their sales estimate by about $1 billion. With one day to go,

Buckingham Research Group reduced its sales estimate by more than $1.1

billion, also noting the slower pace of upgrades.

Analyst James Breen of William Blair says he talks to

investor-relations personnel at AT&T “all the time.” He adjusted his

forecast because the previous estimate hadn’t taken into account the

comments from AT&T’s management at several investor conferences. Mr.

Breen says he also didn’t want to be an outlier compared with other

analysts who follow AT&T.

Mr.

Viola, AT&T’s investor-relations chief, says “companies can and do

talk with analysts about their latest, publicly available information.

That’s the job of investor relations, and it benefits the investing

public.”

He

adds: “Analysts change their estimates for many reasons, and do so

throughout the quarter.” About half the changes in the first quarter

were made a week or less before the April 26 earnings announcement.

AT&T says it falls short of analyst estimates about as often as it

meets or beats them when looking at five commonly followed financial

measurements. In the second quarter, AT&T narrowly missed analysts’

revenue projections.

According to data from FactSet, AT&T met or beat the average earnings

target in 10 of the last 13 quarters and missed by a penny per share

three times.

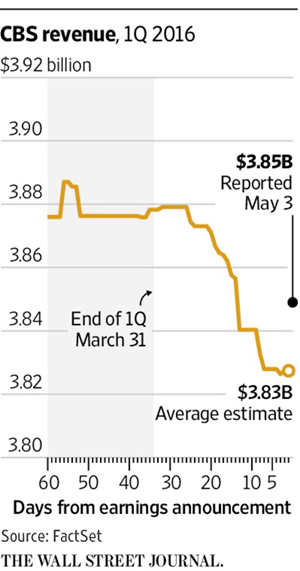

CBS

has surpassed the average earnings estimate in 19 of the past 20

quarters. Several analysts who follow CBS say its investor-relations

staff regularly contacts them to discuss their financial models.

One

analyst says CBS is “more aggressive than most” media companies in its

interactions with analysts. A CBS spokeswoman wouldn’t comment.

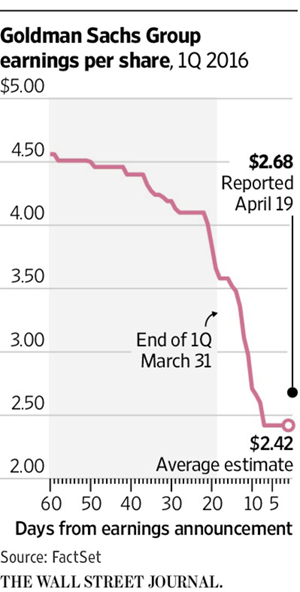

This spring, many analysts were struggling to figure out how Goldman

Sachs Group Inc. would fare amid the first quarter’s market

turbulence. From mid-March to mid-April, 16 analysts cut their

earnings estimates by an average of 41%.

When Goldman

released results April 19, it had

$2.68 a share in earnings, more than 10% higher than the lowered

target. The stock rose 2.3%.

Around the end of the first quarter, the bank’s investor-relations

staff answered calls from analysts, many of whom routinely check in

with the firm when updating their financial models and targets.

Some conversations included discussions about comments from rival

executives at investor conferences during the first quarter, some

analysts say.

Michael DuVally, a Goldman spokesman, says the discussions were

appropriate, partly because analysts “are overloaded with data.” He

adds: “Serving as a resource for public information is a sensible

market practice.”

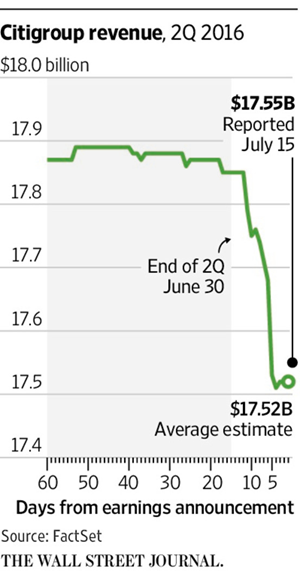

Some analysts who called Citigroup’s investor-relations department

near the end of the second quarter say they were referred to comments

made by Chief Executive

Michael Corbat at a June 2

investor conference.

Mr.

Corbat had said the bank’s second-quarter profits were

likely to be “roughly flat”

compared with the first quarter, when Citigroup earned $1.10 a share.

In late June, the average earnings estimate for the second quarter was

$1.18 a share. The number drifted down to $1.10 a share by July 14,

the day before Citigroup announced results.

After the quarter ended June 30, analysts also trimmed their revenue

estimates for Citigroup by $237 million to $17.52 billion.

Citigroup spokesman Mark Costiglio says investor-relations personnel

didn’t provide any updates to Mr. Corbat’s comment. Any discussions

with analysts “rely entirely on public disclosures the company has

made as of those dates,” Mr. Costiglio adds.

On

July 15, Citigroup

reported second-quarter profit of

$1.24 a share, nearly 13% higher than the average estimate. The bank’s

revenue of $17.55 billion topped analysts’ latest target by about $31

million.

Citigroup executives said the bank’s performance was better than Mr.

Corbat anticipated because of improved market conditions and a pickup

in trading activity near the Brexit referendum on June 23.

Write to

Thomas Gryta at

thomas.gryta@wsj.com, Serena Ng

at

serena.ng@wsj.com and Theo

Francis at

theo.francis@wsj.com

|