More than two dozen ostensibly unrelated letters contained the

same unusual error. Illustration: 731 |

When

Securities and Exchange Commission

Chairman Jay Clayton handed a policy win to corporate executives this

month, he pointed to a surprising source of support: a

mailbag full of encouragement from

ordinary Americans.

To hear Clayton tell it, these folks are really focused on the

intricacies of the corporate shareholder-voting process. “Some of the

letters that struck me the most,”

he said at a commission meeting in

Washington, “came from long-term Main Street investors, including an

Army veteran and a Marine veteran, a police officer, a retired

teacher, a public servant, a single mom, a couple of retirees who

saved for retirement.” Each bolstered Clayton’s case for limiting the

power of dissenting shareholders.

But a close look at the seven letters Clayton highlighted, and about

two dozen others submitted to the SEC by supposedly regular people,

shows they are the product of a misleading -- and laughably clumsy --

public relations campaign by corporate interests.

That

retired teacher? Pauline Yee said

she never wrote a letter, although the signature was hers. Those

military vets? It turns out

they’re the brother and cousin of the chairman of 60 Plus Association,

a Virginia-based advocacy group paid by corporate supporters of the

SEC initiative. That single mom? Data embedded in the electronically

submitted

letter says someone at 60 Plus

wrote it. That

retired couple? Their son-in-law

runs 60 Plus.

|

Jay Clayton

|

|

“I never wrote a letter,” said one of the retirees, Vytautas Alksninis,

reached by phone at his home in Connecticut. “What’s this all about?”

Then there’s the public servant Clayton mentioned. Marie Reed’s

letter has sharp words for proxy

advisers, firms that counsel fund companies on how to vote at

shareholder meetings. But when reached by phone in California, the

retired state worker said she wasn’t familiar with the term. She said

the letter originated with a public-affairs firm that contacted her

out of the blue.

“They wrote it, and I allowed them to use my name after I read it,”

she said. “I didn’t go digging into all of this.”

The SEC declined to comment on any irregularities with the letters. In

a Tuesday interview, Clayton sidestepped a question about how the

agency ensures comment letters are genuine. He did emphasize that the

regulator’s potential revamp of shareholder voting rules are

proposals, adding that there will be ample time for people on both

sides to weigh in before any changes are finalized.

“We welcome input in all ways,” Clayton said in the interview with

Bloomberg Television’s David Westin. “On this issue, where there are a

lot of different views and a lot of different interests, we encourage

people to come in and talk to us, send us their comments."

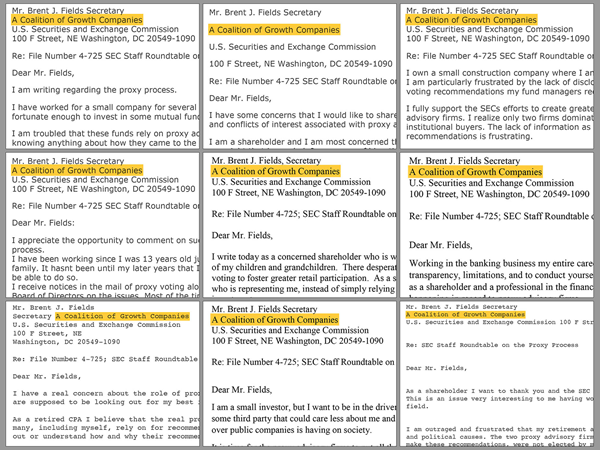

Unusual Error

Even a casual reading of the letters shows something amiss. Four of

the seven bear the same unusual error -- an out-of-context phrase

inserted into the SEC’s mailing address. The same mistake turns up in

at least 20 other letters submitted by supposedly ordinary Americans

in support of the change. It’s an inadvertent digital fingerprint

revealing the scope of the campaign.

At issue is the proxy process, the rules for how corporations conduct

shareholder votes, such as when directors stand for re-election at

annual meetings. Most of the time, management wins in a landslide. But

shareholders occasionally revolt over excessive pay or mismanagement,

or a small investor forces a vote on an issue that management doesn’t

endorse.

In recent years, more small shareholders have been

proposing resolutions about social

or environmental issues such as climate change. And investment

managers that control large numbers of votes, such as

BlackRock Inc., have begun

prioritizing these topics as well,

arguing that they’re relevant to the long-term sustainability of

business models. That’s an unwelcome change for some corporate boards,

especially in the fossil-fuel industry.

Last year, the National Association of Manufacturers

helped form the Main Street

Investors Coalition to oppose what it calls the “politicization” of

the investment process and to

argue that fund managers and

boards should focus on maximizing profits. One of its priorities is

changing shareholder voting rules.

Although the coalition has other members, NAM provided most of its

initial funding, according to a person with knowledge of the

arrangement who spoke on condition of anonymity. The manufacturers’

association represents corporate giants such as

Exxon Mobil Corp. and

Chevron Corp.

NAM said in a statement that it didn’t fund 60 Plus or direct any

advocacy efforts on the SEC issue. Chevron wouldn’t comment on the

coalition but acknowledged in a statement that it sometimes works with

trade associations to “help inform their understanding of issues.”

Exxon Mobil said it had no immediate comment.

Public Comments

Last

year, Clayton signaled he was considering changes to the rules and

issued a call for public comments.

Letters poured in. Most were from investment firms, corporations,

trade groups and other interested parties that openly identified

themselves. Many fund managers wrote to say some of the changes under

consideration would be counterproductive.

The National Association of Manufacturers, Exxon Mobil and Chevron all

called for new limits on shareholders’ proposals. So did two ordinary

citizens who identified themselves as members of Main Street

Investors. Other letters were ostensibly written by regular folks.

But more than two dozen of them appear to have ties to 60 Plus, a

member of the Main Street Investors Coalition. While the nonprofit

group calls itself an advocate for senior citizens’ issues, it

routinely takes money from corporations and advocates for their causes

on issues as varied as

sugar subsidies and

Alabama utility commissioners.

The group didn’t cast a wide net in recruiting letter-writers. Names

included those of a

woman who used to work at 60

Plus’s accounting firm; a

former secretary at 60 Plus; and

various friends and relatives of Saul Anuzis, the 60 Plus president.

None mentioned a connection to the organization.

One

letter bore the name of Chad

Connelly. In an email, Connelly acknowledged being friends with Anuzis

but disavowed the letter. “Someone apparently used my name,” he wrote.

“That’s not a letter I’ve ever even seen.”

Even Scott Hogenson, a contractor for 60 Plus who has appeared in the

press as its spokesman, submitted a

comment. The letter gives his name

as S. Alan Hogenson and doesn’t mention his relationship to the group.

In an interview, Hogenson said he wrote the letter and stands by it.

Anuzis, the 60 Plus president, acknowledged that his group recruited

submitters, provided drafts and, in two cases, sent letters on

members’ behalf. He also acknowledged getting money from members of

the coalition. “We don’t get paid for specific projects,” he said in

an interview. “We get contributions from members who are part of the

coalition. We’re not getting paid for a specific letter.”

Anuzis said the project aligns with 60 Plus’s policy goals and that no

names were used without permission. Those who said they hadn’t agreed,

such as his in-laws, were mistaken. “They are 80-some-years old,” he

said. “This happened months ago. I’m sure it’s not top of their

minds."

Clandestine Aid

Two

letters point to another source of clandestine aid for the

coalition. Reed, the retired state worker from California whose letter

was cited by Clayton, said the man who provided her with a letter

worked at

FSB Core Strategies, a California

public-affairs shop, and said he was working on behalf of a group

called Protect Our Pensions. Another SEC letter containing similar

phrases, also cited by Clayton, came from a

California sheriff who said in a

2017 interview that he was introduced to Protect Our Pensions by the

same FSB staffer. An FSB executive didn’t respond to requests for

comment.

Protect Our Pensions, whose talking points align with those of the

fossil-fuel industry, was the subject of a 2017 Bloomberg Businessweek

article showing it was put

together by corporate public-affairs employees and that some of its

alleged members, including the retired firefighter identified as its

founder, said they had nothing to do with it or couldn’t remember

agreeing to join.

Opponents of changes to the voting system stuffed the SEC’s mailbox

too. The agency reported getting more than 18,000 identical

form letters supporting the

current rules. Those letters were obvious duplicates and are grouped

together on the SEC’s comments page. Clayton’s speech didn’t mention

them.

In his Nov. 5 remarks, Clayton unveiled proposals along the lines of

those pushed by Main Street Investors Coalition and its corporate

backers that would shift power from investors to corporate boards. In

addition to Clayton, who was appointed by President Donald Trump, the

changes are backed by two Republicans on the five-member commission.

For the changes to take effect, the SEC will have to vote again to

finalize the rules after a 60-day public comment period.

The SEC’s proposal would increase the amount of stock newer

shareholders must own to get a proposal on the ballot, aligning with

corporate claims that many resolutions are wastes of time and money.

Under current rules, investors must have owned at least $2,000 of

stock for a year before they can submit resolutions. The SEC’s

proposal would raise that dollar threshold to $25,000 for shareholders

of less than two years and $15,000 for shareholders of less than three

years, while leaving the $2,000 threshold in place for longer-term

holders.

The proposal also would impose new restrictions on proxy-advisory

firms, whose recommendations are often decisive on shareholder votes.

Corporations complain that their advice is sometimes poorly reasoned

or inscrutable. Clayton would require the firms to show their

recommendations to companies before issuing them.

Fund managers warn the measure may have a chilling effect on proxy

advisers, because a corporation could threaten a lawsuit if a draft

recommendation isn’t revised.

Anuzis said he was glad to hear that Clayton had cited letters

generated by his organization. “I’m extremely proud that we were very

effective,” he said. “If four of our letters were quoted, that means

we did a great job.”

— With assistance by Benjamin Bain

(Adds comment from Jay Clayton in the eighth and ninth paragraphs.)

©2019 Bloomberg L.P. All Rights Reserved