|

Editor’s Note:

David F. Larcker is

the James Irvin Miller Professor of Accounting, Emeritus; and Brian

Tayan is

a Researcher with the Corporate Governance Research Initiative at

Stanford Graduate School of Business. This post is based on their

recent paper. |

We recently published a paper on SSRN (“Seven Questions about Proxy

Advisors”) that examines the role and function of proxy advisors.

The proxy advisory industry—in which independent third-party firms

provide voting recommendations to institutional investors for matters

on the annual proxy—has grown in size and controversy. Despite a large

number of smaller players, the proxy advisory industry is essentially

a duopoly with Institutional Shareholder Services (ISS) and Glass

Lewis controlling almost the entire market.

The recommendations of these firms are prominent, especially in

matters such as contested director elections, the approval of large

pay packages, corporate takeovers, and other closely contended issues.

Nevertheless, the degree to which these firms influence voting

outcomes and corporate choices is not established, nor is the role

they play in the market. Are proxy advisory firms information

intermediaries (that digest and distill proxy data), issue spotters

(that highlight matters deserving closer scrutiny), or standard

setters (that influence corporate choices through their guidelines and

models)? Because of the uncertainty around these questions,

disagreement exists whether their influence is beneficial, benign, or

harmful. Defenders of proxy advisors tout them as advocates for

shareholder democracy, while detractors fashion them as unaccountable

standard setters.

The tension has played out on the regulatory front with the Securities

and Exchange Commission (SEC) subjecting proxy advisory firms to

heightened standards in 2019 only to decline to enforce those

standards two years later.

In this Closer Look, we examine seven important questions about the

role, influence and effectiveness of proxy advisory firms.

Question #1: What Is the Market Role for Proxy Advisors?

Proxy advisory firms sell recommendations to institutional investors

on their view of how to vote proxy proposals across thousands of

companies. ISS describes its recommendations as “independent and

objective shareholder meeting research and recommendations… to help

[institutional investors] make informed investment stewardship

decisions, and to help them manage their voting responsibilities.”

Glass Lewis describes itself as “a trusted ally of more than 1,300

investors globally who use our high-quality, unbiased [research] … to

help drive value across all their governance activities.” These

descriptions are consistent with a role as information intermediaries,

with proxy firms offering the benefit of economies of scale to

aggregate and analyze information that would be costly for individual

investment firms to replicate on their own. Iliev and Vitanova (2023)

arrive at this depiction in their analysis of voting recommendations.

A second and related idea is that proxy advisory firms are issue

spotters. In this description, the value of proxy advice comes from

sifting through thousands of issues to identify those that require

additional attention and analysis—which the investment firm itself

then conducts. Sarro (2021) argues that this is the real role that

proxy advisors play, concluding, “[Their] influence derives primarily

from their ability to direct institutional investors’ attention away

from some proposals and toward others.”

Another theory is that proxy firms are controversy creators. Closely

contested proxy matters are beneficial to the proxy advisory firm

because close contests increase the economic value of a proxy

advisor’s recommendation. (In this way, proxy advisory firms do not

have the same economic interests as those of investment advisors.)

Malenko, Malenko, and Spatt (2023) argue that proxy advisory firms

benefit from “biasing” recommendations (their word) to increase the

frequency of close votes in order to increase demand for their

services.

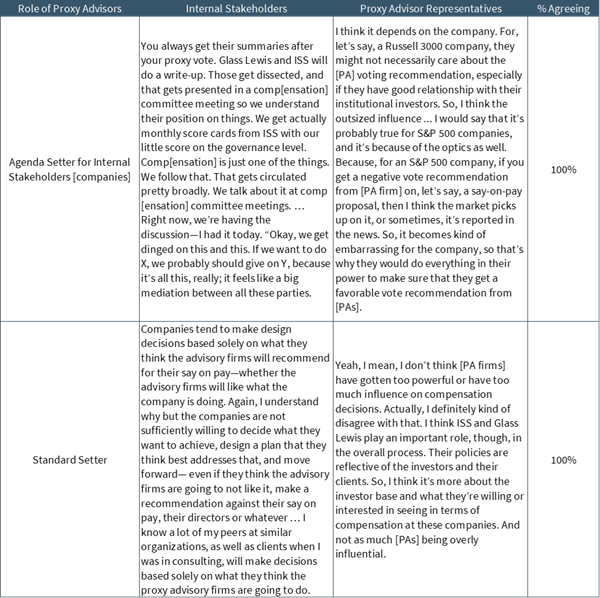

Another theory is that proxy advisors are agenda setters. Through

survey data, Hayne and Vance (2019) demonstrate that boards feel

pressure to alter their governance practices to conform to the

standards of proxy advisory firms, despite a preference for

alternative structures (see Exhibit 1). They conclude that proxy

advisors are not merely information intermediaries but agenda setters

because the one-size-fits-all nature of their voting guidelines

compels conformity among corporate practices.

Currently, we do not have consensus about the role or roles that proxy

advisory firms play.

Question #2: How Do Proxy Advisors Derive Their Influence?

Proxy advisor recommendations influence voting outcomes. The degree of

influence, however, is not established. Brav, Cain, and Zytnick (2022)

show that institutional investors are highly sensitive to an opposing

recommendation from proxy advisory firms, with opposition from ISS

associated with a 51 percent difference in institutional voting

support compared with only a 2 percent difference among retail

investors. Malenko and Shen (2016) estimate a negative recommendation

from ISS leads to a 25 percentage point reduction in voting support

for say-on-pay proposals. Data from Copland, Larcker, and Tayan (2018)

show a negative recommendation from ISS is associated with a 17

percentage point reduction in support for equity-plan proposals, 18

points for uncontested director elections, and 27 points for say on

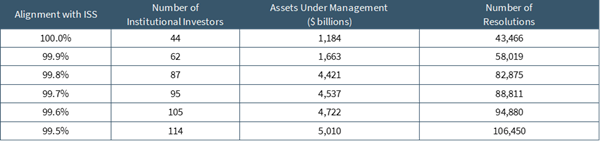

pay. Rose (2021) examines “robo-voting”—the practice of fund managers

voting in lock-step with the recommendations of ISS (defined as 99.5

percent alignment). He identifies 114 institutions managing $5

trillion in assets that robo-vote (see Exhibit 2). Iliev and Lowry

(2015) find that 25 percent of institutional investors vote

“indiscriminately” with ISS (see Exhibit 3).

What is unknown is whether the influence proxy advisory firms exert on

voting practices is evidence of the value of their services (i.e., the

quality of their recommendations) or distortions caused by the

regulatory environment. Generally, firms purchase services because of

the value vendors provide, and it might be the case that institutional

investors purchase voting recommendations from ISS and Glass Lewis

because they are a cost-effective means of making informed voting

decisions.

On the other hand, it might be that economic demand for voting

recommendations is artificially inflated by the regulatory

environment. The SEC requires institutional investors to vote all

matters on the proxy and to make their votes public. To satisfy this

obligation, institutional investors must develop proprietary

guidelines or rely on guidelines developed by third parties. Firms

whose voting patterns are closely correlated with ISS or Glass Lewis

recommendations apparently have elected to rely extensively on these

guidelines. Whether they do so because they find these guidelines

value-enhancing to their shareholders or an inexpensive way of meeting

a regulatory requirement to vote is uncertain.

Question #3: How Do Proxy Advisory Firms Test the Validity of Their

Recommendations?

Because institutional investors rely on proxy voting guidelines to

inform their voting decisions, it is important that proxy advisory

firms test their standards through a rigorous analytical process to

ensure accuracy.

We do not have detailed information about how policy guidelines are

developed. ISS discloses some information about how it updates

policies; Glass Lewis does not disclose this information. The ISS

annual update cycle includes the following steps:

-

Internal review of emerging issues, regulatory changes, and trends

-

Review of academic literature, empirical studies, and market

commentary

-

Survey of and roundtable discussion with investors and corporate

issuers

-

Release of draft policy updates

-

Open review and comment period

-

Release of final policy updates

We do not know whether, as part of this process, ISS tests existing

guidelines through empirical analysis to ensure they are associated

with positive outcomes, such as increased operating- or stock-price

performance or a lower incidence of governance failures (such as

restatements, regulatory violations, lawsuits, or bankruptcy). Without

empirical evidence demonstrating these associations, we will not know

whether proxy advisory firm guidelines are in the interest of

shareholders.

Professional researchers have examined some aspects of ISS and Glass

Lewis policies, and the results of these studies are mixed. Alexander,

Chen, Seppi, and Spatt (2010) find ISS recommendations in contested

director elections are positively associated with shareholder returns.

Larcker, McCall, and Ormazabal (2013) study stock option repricing

plans and find that plans that conform to ISS criteria are associated

with lower returns, lower future operating performance, and higher

employee turnover. In a separate study, Larcker, McCall, and Ormazabal

(2015) find shareholders react negatively to companies that revise

their executive compensation programs to make them more consistent

with ISS guidelines for say on pay. Conversely, Dey, Starkweather, and

White (2023) find that companies that receive relatively low

say-on-pay support and engage with ISS exhibit positive future

returns. Daines, Gow, and Larcker (2010) study ISS governance ratings

and find they are not predictive of future operating performance,

stock-price performance, or governance failure.

Our understanding of the rigor and reliability of proxy advisor

guidelines would be greatly enhanced through additional study.

Unfortunately, ISS voting recommendations have been removed from the

databases that academics previously have used to conduct these

studies, making future studies impossible. (In response to questions

from the Stanford Graduate School of Business Library about how to

access ISS voting recommendations for research purposes, ISS responded

that it “will not be able to offer any options / channels to access

that data set moving forward.”) Without access to voting

recommendations, researchers are unable to assess the reliability and

validity of proxy advisory firm guidelines.

Question #4: How Do Proxy Advisory Firms Evaluate Individual

Directors?

Proxy advisory firms provide voting recommendations on individual

director nominations at all public companies. The sheer number of

directors makes this work onerous. By one count, there are

approximately 40,000 directors of public companies in the U.S. alone.

To provide an accurate assessment requires knowledge of the skills,

domain expertise, and boardroom contribution of each director. From a

practical perspective, it is challenging to develop an informed view

of each director without access to the individuals themselves or some

insight into how board meetings are conducted.

Proxy advisors say little about how they determine the effectiveness

of directors. Glass Lewis says it assesses directors on their

independence and performance. ISS evaluates them on independence,

board composition, responsiveness, and accountability. Beyond, this,

we do not know how proxy advisors measure the effectiveness of a

director at the individual, committee, or board level.

Cai, Garner, and Walkling (2009) and Choi, Fisch, and Kahan (2010)

show that ISS and Glass Lewis recommendations influence the voting

results of uncontested director elections, while Alexander, Chen,

Seppi, and Spatt (2010) show they heavily influence contested

elections.

The recommendations of proxy advisors will take on newfound importance

in the age of universal proxies, in which activist investors are able

to directly nominate dissident board members side-by-side with the

company’s nominees on the annual proxy. Proxy advisors will be

positioned to directly influence the composition of public boards by

recommending a vote for certain individual candidates over others.

Whether they are able to reliably weigh the merits of competing

individual nominees is an open question.

Question #5: Can Proxy Advisors Detect “Excessive” CEO Pay?

Few matters in corporate governance are more controversial than

executive compensation. According to one survey, 75 percent of

Americans believe CEO pay is too high.

For this reason, stakeholders pay considerable attention to the voting

recommendations of proxy advisory firms. One study shows negative

recommendations from ISS and Glass Lewis reduce support for say-on-pay

by around 30 percent. Another estimates 25 percent. Data on equity

plan proposals suggest an impact of approximately 20 percent.

ISS and Glass Lewis have developed elaborate models to inform their

voting recommendations for executive pay plans. Glass Lewis takes into

account the relation between pay and company performance, the mix of

short- and long-term incentives, the mix of variable and fixed

elements, the relation between pay and risk, the choice of peer

groups, and disclosure practices. It recommends against “excessive

bonuses,” “excessive risk-taking,” and “excessive payouts.”

ISS considers many of these same factors and generally recommends

against pay packages that include what it describes as “problematic”

elements. These include “egregious” pay contracts, “overly generous”

new-hire packages, “abnormally large” bonuses without a clear link to

performance, “excessive” perquisites, and “problematic” severance. ISS

also recommends against multi-year employee equity plans that exceed

proprietary thresholds for total shareholder value transfer (SVT).

While both firms provide extensive disclosure about their pay

recommendations, we do not know how these firms determine which

practices are excessive or egregious. Professional researchers have

extensively studied CEO pay and, overall, little consensus exists

about whether CEO total compensation on average is set at the right

levels, whether it is properly aligned with performance, and whether

it encourages appropriate risk-taking. It might be that proxy advisory

firms have independently developed frameworks to distinguish fair and

unfair pay practices; if so, these models have not been externally

vetted.

Nevertheless, companies pay careful attention to proxy advisory

guidelines when designing pay. A study by The Conference Board,

NASDAQ, and the Rock Center for Corporate Governance at Stanford

University finds that approximately three-quarters (72 percent) of

publicly traded companies review the compensation policies of a proxy

advisory firm and a significant percentage of these make changes to

pay structure in response.

Edmans, Gosling, and Jenter (2023) find that approximately half of

companies (53 percent) offer less pay to the CEO than they otherwise

would in order to avoid a negative recommendation from a proxy

advisory firm. Jochem, Ormazabal, and Rajamani (2021) find that CEO

pay levels have declined in variation within industry and size groups,

with proxy advisor influence being one cause of this decline; they

find negative shareholder outcomes associated with this trend. Cabezon

(2024) finds that the distribution of pay components—salary, bonus,

equity, and other elements—across firms has also become more

standardized, with pressure from proxy advisors one cause of this

trend; he too finds standardization to be associated with lower

shareholder value. It is far from clear that these outcomes are

beneficial to shareholders and stakeholders.

Question #6: Does a Proxy Advisor’s View of ESG Influence Its

Recommendations?

Proxy advisory firms are known primarily for recommendations on

traditional corporate governance concepts. While they also provide

recommendations for shareholder resolutions on environmental and

social matters, their support—at least historically—was fairly muted.

For example, ISS generally has supported proposals to the extent they

“enhance or protect shareholder value,” address “business issues that

relate to a meaningful percentage of the company’s business,” but do

not concern matters “more appropriately / effectively dealt with

through governmental action” or are otherwise “best left to the

discretion of the board.”

With the rise of ESG investing and ESG issues, ISS has entered the

business of providing ESG ratings. A rating is fundamentally different

from a recommendation on a proposed corporate provision. According to

ISS, its ratings are

designed to enable institutional investors to support their investment

strategies by assessing the environmental, social, and governance

(ESG) performance of corporate issuers. In the context of the ESG

Corporate Rating, ESG performance refers to a company’s demonstrated

ability to adequately manage material ESG risks, mitigate negative and

generate positive social and environmental impacts, and capitalize on

opportunities offered by transformation towards sustainable

development.

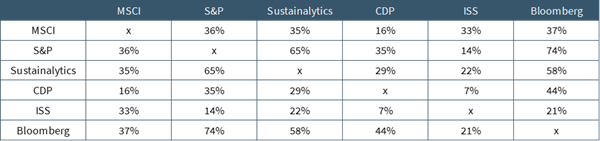

The evaluation of ESG performance is a phenomenally complicated

undertaking. Professional researchers have painstakingly scrutinized

the methodologies and predictive ability of ESG ratings and are

divided whether it is possible to evaluate ESG quality and, if so,

whether a single rating has informational value. (ESG ratings are also

known to have low correlation across providers, suggesting they are

either not reliably measuring the same construct or they are measuring

different constructs—see Exhibit 4).

The risk for issuers is that a proxy advisor’s view of ESG quality

might influence its recommendations on proxy items in a way that is

not in the interest of shareholders. For example, in the 2021 proxy

contest between ExxonMobil and Engine No. 1, ISS backed three of the

four directors put forward by Engine No. 1 because of their advocacy

for ESG concepts, swinging the outcome of a closely run election just

before a sharp upturn in traditional energy markets. In 2024, ISS

recommended against the reelection of five directors to the board of

Berkshire Hathaway because of ESG factors, without regard to the

recent or long-term success of the company.

Spatt (2021) finds the proxy-maximizing incentives of proxy advisory

firms are not aligned with those of investors and can encourage these

firms to promote controversy or cater to ESG investors to increase own

market share at the expense of beneficial owners.

Question #7: Are Proxy Advisory Firms Independent?

Institutional investors rely on proxy advisors to provide an

independent assessment of proposed corporate and shareholder actions.

However, whether proxy advisory firms are independent is an unresolved

question. Some proxy advisors receive consulting fees from the same

companies whose governance and ESG practices they evaluate, and the

potential exists that they alter their voting recommendations to gain

or retain business. Ma and Xiong (2021) show, using a theoretical

model, that conflicts of interest can bias voting recommendations and

decrease firm value.

Some evidence suggests this might be occurring. Li (2018) examines

voting recommendations and finds that ISS shifts its positions to make

them more favorable to the preferred position of the client company

when Glass Lewis initiates coverage of that company. He concludes

“conflicts of interest are a real concern.”

Policymakers have the option to introduce safeguards to assure the

independence of proxy advisory firms. One approach is increased

disclosure. Malenko and Malenko (2019) and Edelman (2013) argue the

quality of recommendations would improve through greater transparency.

An alternative approach would be to designate proxy advisory firms as

fiduciaries. Spatt (2021) points out that these firms are outliers in

the financial services industry, being subject to lower standards of

accountability than institutional investors, auditors, and credit

rating agencies. He argues that a fiduciary standard would align the

interests of proxy advisors with those of shareholders. Sharfman

(2020) also makes this point. Another approach, put forward by Manna

(2021), would be to require greater separation between the consulting

and advisory businesses of these firms.

Why This Matters

-

The proxy advisory industry is marked by

considerable controversy regarding its purpose, influence, value,

and objectivity. What is the reason for this controversy? Why have

researchers been unable to demonstrate the purpose and role of

these firms? Why do market participants and regulators disagree so

starkly over their contribution? Is the proxy advisory industry—as

currently structured—a net benefit or cost to shareholders?

-

Considerable disagreement exists over the

influence that proxy advisory firms have on voting outcomes. What

explains the large swings in voting outcomes that seem to be

associated with their recommendations? Are investors making

“informed decisions” based on information provided by these firms,

or are they “blindly following” recommendations? Would the

influence of proxy advisors be lessened if institutional investors

were not required to vote?

-

Considerable evidence suggests that proxy

advisor guidelines influence corporate practices, particularly in

the area of compensation design. Are these guidelines associated

with improved outcomes? What research do proxy advisory firms

conduct to satisfy themselves that their guidelines are beneficial

to shareholders and stakeholders? Why don’t these firms provide

greater transparency around their methodologies?

-

Proxy advisory firms have recently made

the decision to remove their voting recommendations from research

databases that professional researchers have used to conduct

empirical studies on voting practices. As a result, future

research into the questions discussed in this Closer Look will be

greatly inhibited. What is the justification for this decision?

Links to SSRN: 20240429_Larcker-Tayan.pdf

Exhibit 1: Perceived Market Role of Proxy Advisory Firms

Source: Hayne and Vance (2019).

Exhibit 2: Institutional Investors Voting in Alignment with ISS

Rose (2021).

Exhibit 3: Institutional Investors Voting with ISS, By Issue

Iliev and Lowry (2015).

Exhibit 4: Correlation among ESG Ratings Providers

CFA Institute (2021)

Kevin Prall, “ESG Ratings: Navigating Through the Haze,” blog posting

at CFA Institute (August 10, 2021).

Berg, Kӧlbel, and Rigobon (2022)

Florian Berg, Julian F. Kölbel, and Roberto Rigobon, “Aggregate

Confusion: The Divergence of ESG Ratings,” Review of Finance (2022).

|

Harvard Law School Forum

on Corporate Governance

All copyright and trademarks in content on this site are owned by

their respective owners. Other content © 2024 The President and

Fellows of Harvard College. |