BlackRock’s big deal this week has little to do with its core

business, the

one it’s known for: managing $10 trillion of our money. Financial-data

providers like Preqin, which BlackRock is buying for

$3.2 billion, are arms dealers, not warlords. They’re more valuable as

neutral brokers than as a secret sauce for any one fund manager.

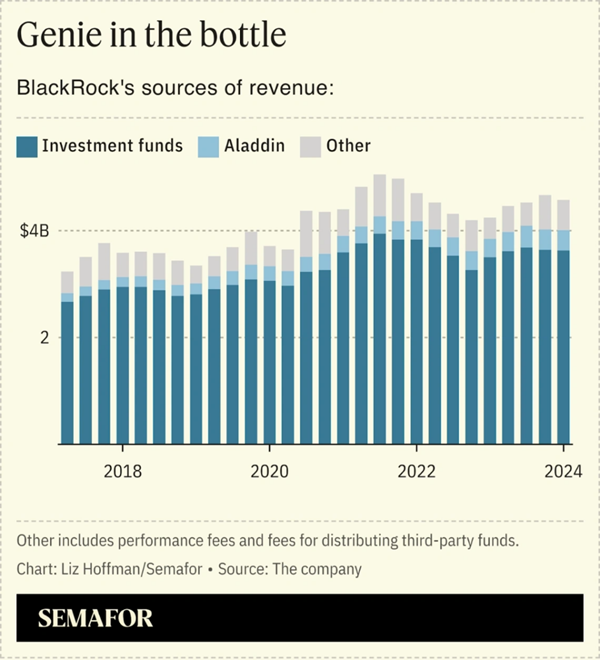

This is about BlackRock’s other business, one that it would

like its stockholders to pay more attention to. Its Aladdin software,

which lets money managers analyze and spot risks in their portfolios,

accounts for a small but growing slice of BlackRock’s revenue, 8% last

year. What began as BlackRock’s own central nervous system — this

being finance, its name is obviously an insane

acronym — was offered to outside firms starting in the

1990s.

Aladdin is to BlackRock what cloud provider AWS is to Amazon: an

internal tool that turned into a serious venture in its own right —

and one that is in a different, more valuable business than its

corporate owner. If stockholders valued Aladdin’s revenue like they

value that of S&P Global and Moody’s, it would be worth an extra $10

billion in market capitalization to BlackRock. That’s another way of

saying that Aladdin could be more valuable outside BlackRock than

inside, which is why every few years, there’s some spinoff chatter

that BlackRock quashes quickly.

The other path is to grow it and try to get shareholders to revalue

the entire company, bit by bit. Thus this week’s deal. That’s hard to

do, and Preqin is a drop in the bucket, but it is strategic M&A at its

absolute purest.

© 2024 SEMAFOR INC. |