Feb. 11, 2025 5:30 am ET

|

Warren

Buffett in Omaha, Neb., last year. Photo: Vincent

Tullo for WSJ

|

The investing secret that helped make Warren

Buffett a multibillionaire isn’t working anymore, though

probably not for the reason you would think.

Every decade or so someone will declare that the Berkshire

Hathaway boss has

lost his touch—usually a cue for the reasonably priced

stocks he prefers to come roaring back. Even so, value investing the

way that Buffett’s mentor Benjamin Graham practiced it and Nobel

Prize-winning economists defined it decades later has had too few

rebounds recently.

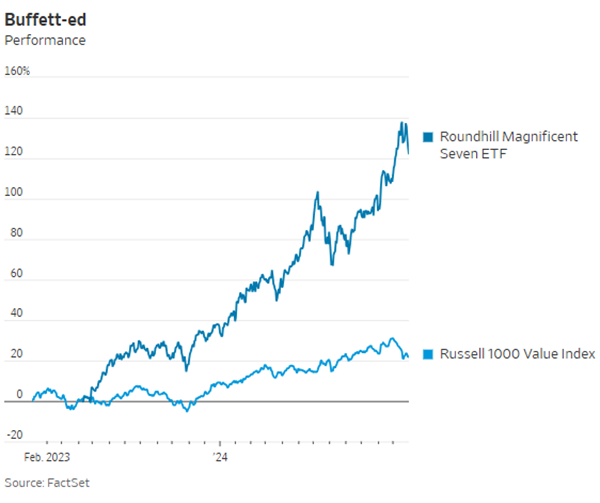

The reason isn’t that the “Magnificent

Seven” stocks such as

Nvidia,

Apple and

Tesla have rewritten the law of

gravity. Value investing just needed a tuneup. A slew of

exchange-traded funds, many without “value” in their names, have given

it one.

The classic value factor was described in a

landmark paper by economists Eugene Fama and Kenneth

French in 1992, and it was compelling: A portfolio of stocks that were

cheap relative to their book value trounced flashier stocks to the

tune of thousands of percentage points over the decades.

But the professors’ results covered a period when companies’ value was

mostly in property and machinery rather than brands and intellectual

property. Fifty years ago, less than a fifth of the S&P 500’s assets

were intangible. Today it is well over four-fifths, and many

top-performing companies like Microsoft are

“asset-light.”

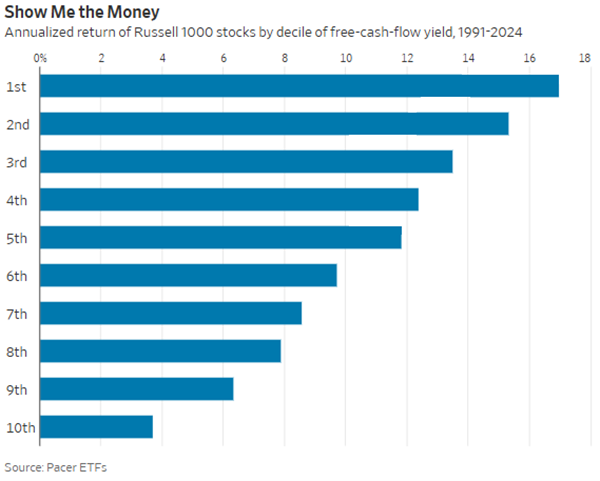

The results tell the story: Analysts

at fund manager Lord Abbett point out that a low

price-to-book-based portfolio returned 519% between 2002 and the

middle of last year. One based on free-cash-flow yield did more than

twice as well.

Free cash flow is generally defined as money left over after expenses

and capital expenditures that a company can return to shareholders.

The yield is usually calculated by dividing 12-month free cash flow by

enterprise value—market capitalization plus net borrowings.

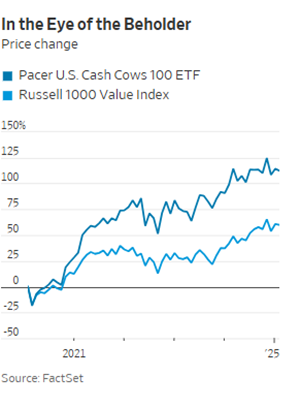

“We sort of caught on to this about 10 years ago,” says Sean O’Hara,

president at Pacer ETFs Distributors. Pacer’s U.S. Cash Cows Index

underpins an eponymous ETF, ticker symbol COWZ,

which has about $25 billion in assets. The index has returned 15.7%

annually over five years, a whopping 7 percentage points better than

the Russell 1000 Value Index. It even beat the plain-vanilla Russell

1000 index, dominated by the very much non-value Mag 7 stocks, by 1.4

points a year.

If imitation is the sincerest form of flattery, then the recent

popularity of funds that try to capture similar effects is high praise

for free-cash-flow yield. ETFs launched in 2023 alone include the

tickers FLOW from

Global X, QOWZ from

Invesco,

COWS from Amplify ETFs and VFLO from

VictoryShares.

Value investing was never dead—it just had a measurement problem.

Plenty of investors, including Joel Greenblatt of

“Magic Formula” fame, and even Buffett himself, ignore the

academic straitjacket plaguing some value indexes. Other fund managers

have accounted for the rise of intangible assets by tweaking the

classic book-value calculation, which also improves results. That is

harder to explain, though.

COWZ is simple: Its proprietary index picks the 100 highest

free-cash-flow yielders out of the Russell 1000 stock index and then

weights those 100 by their free cash flow in dollars, capped at 2% of

the index. The fund’s yield at the end of 2024 was 7.32% or 4.7

percentage points more than the overall Russell 1000 index. A small

company version, CALF (get

it?), yielded 9.94%.

Will the strategy work during tough times? S&P Dow Jones Indices has

constructed its

own free-cash-flow-based index based on the S&P 500. It

calculates that the index beat the broad market by the greatest margin

during times of falling economic growth and rising inflation.

With nervousness growing over the Mag 7 stocks, COWZ’s top seven

returners of cash recently—Qualcomm, Gilead

Sciences, Cencora, Tenet

Healthcare, Valero

Energy, Archer-Daniels-Midland and Bristol-Myers

Squibb—might be a sturdier alternative.

Just call them the “Munificent Seven.”

Write to Spencer Jakab at Spencer.Jakab@wsj.com