|

The Oldest Established Permanent Corp Gov Proposal in US Equity

Markets*

Activists submit hundreds of ESG proposals

each year at US public companies (this year it seems they will submit

significantly fewer

than in past years). A few times each year an activist submits an

AGM proposal that the company recommends shareholders vote for. This

might impress the activist, that it wrote a proposal that the

portfolio company wants to adopt.

The idea that a company urges shareholders to

vote for a precatory proposal actually bothers us. Duke Energy (DUK)

takes it to an absurd extreme.

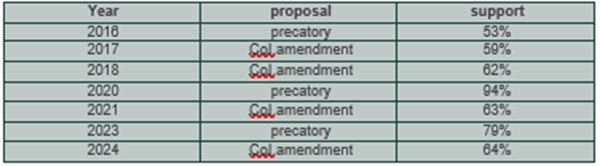

DUK has tried this since 2016

ValueEdge Advisors

reminded us

recently of this long-running farce. It noted DUK recommends

shareholders vote for a precatory proposal to adopt simple majority

voting, submitted by corp gov maven John Chevedden for the

2025

AGM

(Proposal 4). It might flatter us corp gov types that a company

such as DUK supports this.

The history of this particular effort betrays

any such warm feelings. It started in 2016, when Chevedden proposed

the exact same thing. You see, DUK has a now-uncommon (but not

uniquely rare) term in its governing documents that requires support

of 80% of outstanding shares to amend the certificate of incorporation

(CoI) or bylaws. On the latter, the

BoD can of course amend the

bylaws whenever it likes. The CoI provides that

shareholders can amend the

bylaws pursuant to that 80% supermajority. And, as with most public

companies, any CoI amendment requires shareholder approval, in this

case with the same 80% supermajority. This of course makes it

practically impossible for activists to win support for any kind of

bylaw or CoI amendment.

The 2016

precatory proposal, which DUK opposed, won support from a majority of

shareholders (see chart below). DUK waited a year, and in 2017 dutifully

proposed to amend the CoI as shareholders desired. The CoI amendment

at the 2017 AGM won 59% of

the outstanding shares, a decent outcome

but not

the needed

80%. DUK

magnanimously tried

again the

next year and

won 62%

of the

outstanding shares,

again failing

to win

the needed

shareholder support.

Chevedden took a year off, and in 2020 submitted the same precatory

proposal. This time DUK neither opposed or supported it. It won 94% of

the votes, as

good as

it gets.

So, in

2021 DUK

again put

the CoI

amendment to

a vote, which won support from 63% of shareholders. While

better than 2017 and 2018, it still wasn't the 80% it needed.

Chevedden waited

another year,

and in

2023 tried

another time

(he's nothing

if not determined, as many companies have learned). DUK again

neither opposed or supported it. His precatory proposal won 79% of the

votes, not as good as

in 2020

but still

a healthy

majority. DUK

dusted off

the CoI

amendment the next year, and in 2024 it won 64% of the votes.

The upward trend in support still could not break the 80% barrier.

For this

year, now

DUK recommends

shareholders

support the

proposal. We're

eager to

see how

much better

it does

relative to

the 94%

support in

2020. With the

expected support, DUK would put it up for yet another shareholder vote

(fifth time is the charm?) in 2026.

Company support

means

little

Other companies

do this.

For example,

CAT received

a precatory

proposal for a

climate policy report for a vote at its

2022 AGM

(Proposal 4). CAT recommended

its shareholders support it, so it received 96% of the votes.

Last year,

HCC recommended

its shareholders

support a

shareholder

proposal for a

proxy access

bylaw. Of

course, this

was the

memorable situation

at which the United

Mine Workers submitted four proposals and

solicited proxies

itself.

Among those

four was

the proxy

access bylaw

proposal, which

then won 99%

support.

It bothers us that CAT didn't simply write the climate policy report,

or HCC didn't just amend the bylaws to provide for proxy access. If

they wonder whether shareholders really want this stuff, then their

investor relations folks could easily tell them. Endorsing the

shareholder proposal might make the activist

or others

feel good.

It mostly

serves to

delay even

longer responding

to the proposal.

DUK takes

this approach

to an

extreme. Activists

like that

it supports

this year's majority

vote proposal. Instead, it merely reveals how little DUK wants it.

We suspect DUK hasn't made any serious attempt to round up the needed

80% of outstanding shares. We found no evidence of extra shareholder

communication or

solicitation in

the four

years with

the CoI

bylaw amendment on

the AGM agenda.

Also, three times DUK shareholders endorsed a precatory

proposal to

eliminate the

supermajority

provision. DUK

could have quickly

called a

special shareholder

meeting or

solicited written

consent from

shareholders to

implement the

change. Instead,

it waited

a year

until the

next AGM to put it to a shareholder vote.

DUK

also has

abundant experience

with this

particular proposal

and a

good idea of how much shareholders want it. Instead of merely

endorsing the Chevedden proposal, why not put the CoI amendment on the

2025 AGM agenda and

(finally) solicit aggressively?

Look,

we know

why. DUK

doesn't want

shareholders to

amend the

bylaws, and doesn't

need any amendments to the CoI. If it did, we can be quite sure it

would hire multiple solicitors and communicate creatively with

shareholders to bring out the needed participation. Otherwise, it can

continue to slow-walk the proposal and blame shareholders for failing

to turn out for the AGM.

So,

let's not

get excited

that DUK

supports activist

John Chevedden's

precatory proposal. Let's get angry it hasn't done more.

*with apologies

to and

affection for

Guys and

Dolls.

|