Shareholder Meetings: Unearthing the history

By Tanya Mohn

|

Wilma Soss, president of the Federation of Women Shareholders asks a

question at the General Electric annual meeting in 1962. Beatrice Kelekian

is on the left.

|

|

Nearly 400 years ago, angry shareholders of the Dutch East India

Company pushed for more rights and accused directors of self-dealing. In 19th

century America, stockholders kept a close watch on public companies that

operated bridges, canals, banks and especially railroads, which resulted in

numerous fights for control.

Not much more is known about the early days of shareholder

activity, says Colleen Dunlavy, a professor in the Department of History at the

University of Wisconsin-Madison. There is a dearth of documentation, including

in companies’ archives.

But there were two key institutional developments in this

country. “One of the big changes over the 19th century was the increasing use of

proxies and the corresponding decline in in-person attendance at shareholder

meetings,” says Dunlavy, whose research focuses on the history of shareholder

voting rights.

Attendance — and therefore in-person voting — was more robust

before the Civil War. The voting model for business corporations was based on

municipal corporations, according to Dunlavy. City residents could not vote by

proxy, and neither could early shareholders without explicit sanction in law.

Voting by proxy became common after the Civil War, as more companies expanded

their geographical reach, although some railroads in the 1850s offered free

passes to shareholders to make it easier and less costly to attend, she says.

A second significant modification was the move to cumulative

voting, a system that fosters consolidation of votes for better representation.

If a shareholder has 100 shares and three directors are being elected, the

shareholder — instead of casting 100 votes for each director — may cast all 300

votes for a single director. “By the 1880s, one vote per share was the norm in

the U.S.,” Dunlavy said. “Cumulative voting was a modest effort to counteract

the dominance of the largest shareholders and push the balance of power back to

the small shareholder.”

But it is the last century that has been the most turbulent

period for corporate oversight and power struggles between management and

shareholders, says Jeff Gramm, author of Dear Chairman: Boardroom Battles and

the Rise of Shareholder Activism, which chronicles the evolution of

shareholder behavior, highlighted by letters from activist investors like Warren

Buffett and Ross Perot. “If no one is paying attention, most boards will act in

self-preservation rather than doing right by shareholders,” he says.

A letter written in 1927 by Benjamin Graham, a professional

investor, aimed to convince John D. Rockefeller Jr., Northern Pipeline’s biggest

shareholder at the time, to distribute the company’s excess capital to

shareholders. “The letter ultimately failed,” as Rockefeller did not support

Graham’s request, “but he still won the vote,” says Gramm, a move he credits as

the birth of modern shareholder activism.

| |

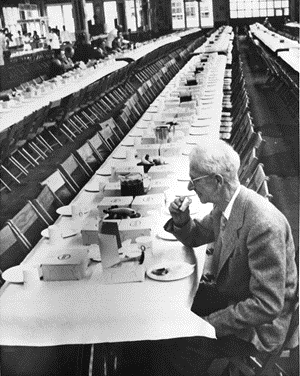

Robert G. Wood of Middletown, N.Y., beats the others attending the annual

shareholders meeting for Standard Oil Company for a boxed lunch including

fruit, ice cream and coffee.

|

“For most of history, including now, most annual shareholder

meetings were uneventful formalities. But they take on a special meaning when a

company is doing very poorly,” said Gramm. “If there is no accountability, bad

things can happen.”

Shareholders and their meetings in the 1920s were made up mainly

of founding partners and strategic investors. It was a group that tended to be

engaged. Only the largest railroad companies had diverse shareholder bases.

The first modern public corporations in the United States became

recognized in the 1930s, following the great stock market crash of October 1929,

explains Alexandra Lajoux, chief knowledge officer emeritus for the National

Association of Corporate Directors. In their 1932 book The Modern Corporation

and Private Property, Adolf Berle and Gardiner Means noted with alarm a

separation of ownership and control in some companies due to dispersion of

holdings among many owners, and flagged such corporations as “quasi-public,” in

contrast to private companies.

Rules for such “public” entities became enshrined in the

Securities Act of 1933 and Securities Exchange Act of 1934, which jointly

established the Securities and Exchange Commission, says Lajoux. The main focus

of the securities laws and the SEC was to ensure proper communications from

companies to shareholders and the annual meeting was an important venue for this

transfer of information.

Section 14 of the Securities Exchange Act, she points out, is

entitled Proxies and it regulates annual communications from companies to

shareholders in the proxy statement, so named because it enables votes (via

proxy) by shareholders who are not at the meeting in person.

“While annual meetings existed before then,” she adds, “the 1934

act and its Section 14 brought discipline to the communications leading up to

the annual meeting.” Another milestone occurred in the 1940s, when the SEC

passed its first rules mandating inclusion of shareholder resolutions in proxy

statements.

By the 1950s, the shareholder base of public companies had

rapidly diffused. That decade saw a proxy fight movement, which put hostile

shareholders in the public eye for the first time. From the 1960s and continuing

until today has been a second period of concentrated ownership, this time by

large institutional investors, like pension and mutual funds.

|

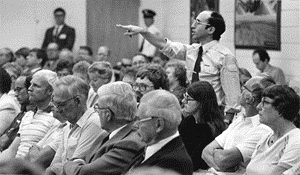

Frank Shansky, a member of United Auto Workers Local 248, asks David S.

Scott, chairman of Allis-Chalmers Corp., "How do you sleep at night?"

|

|

An October 8, 1966 column from The New Yorker provides

insight into the time period. John Brooks detailed his experiences attending a

number of annual meetings, including one held by AT& T, then the world’s largest

company, in “A Reporter at Large: Stockholder Season.” Brooks, who referred to

corporate power as making the medieval feudal system look like a Sunday school

party, noted that many companies were beginning to hold the yearly gatherings

away from headquarters, officially, they claimed, to make it easier for

stockholders from other areas of the country to attend. But the real reason,

Brooks surmised, was so management could avoid “most of the noisiest dissident

stockholders.”

Meetings and shareholder involvement was very hands-off until the

1980s, a period of corporate exploitation during which hostile raiders and

management teams sometimes took advantage rather than protected the interests of

passive investors, says Gramm, the author who runs the Bandera Partners hedge

fund. “Shareholder actions during that time pushed big institutions to really

mind their business again.”

But despite notable discord through the years, the fundamentals

of annual shareholder meetings have changed little since becoming part of the

American corporate fabric and remain true to their Roman-inspired heritage.

“It’s a representative democracy,” an important check and balance

between those who run the company day-to-day and investors, says Wei Jiang, a

professor in the finance and economics division and vice dean for curriculum and

instruction at Columbia Business School. “It’s practically the only opportunity

for managers to meet shareholders face to face.”

And the combination of annual meetings and shareholder activism

“is a good thing” says Jiang, spawning engagement that challenges companies “to

act in their own best interests.”

Tanya Mohn

frequently writes about business topics, from personal finance issues to the

changing workplace, for a host of publications including

The New York Times, Forbes, BBC and NBC

News.

| © 2017

Directors & Boards. All rights reserved. |

|