|

Buzzkill Profs: Hedge Funds

Do Half as Well as You Think

by

Michael P Regan

August 17, 2015 —

10:59 AM EDT

n

Here's Why Hedge

Funds Don't Perform All That Well

It's the dog days of summer, when

college professors are supposed to be doing nothing but mimeographing

their syllabus and mending the elbow patches on their blazers (or

whatever it is that they do in the summer.)

But that's not stopping some academics

from throwing shade, as the kids say, in the general direction of the

hedge fund industry.

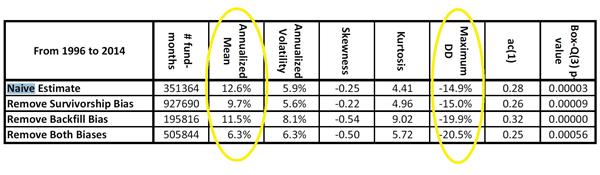

Their study shows

that due to inherent biases in the way hedge-fund databases compile

results, the industry's returns have been about half as strong as they

appear. The average annualized return for the industry since 1996 goes

from 12.6 percent to 6.3 percent when the biases are removed from the

data, according to the paper.

The volatility of the funds increases

along with their maximum drawdowns. Also, measures of how the returns

data are distributed, known as kurtosis and skewness, also change

noticeably.

n

From:

"Hedge Funds: A Dynamic Industry

In Transition" by Mila Getmansky, Peter A. Lee and Andrew W. Lo.

(Yellow circles added for emphasis.)

(The researchers -- Mila

Getmansky

of the University of Massachusetts Amherst,

Andrew Lo

of the Massachusetts Institute of Technology and

Peter Lee

of Lo's firm AlphaSimplex Group -- used data from Lipper TASS, though

the same biases exist in other services. Bloomberg also compiles

hedge-fund results and maintains indexes of returns for various

strategies.)

The biases stem from the fact that hedge

funds

voluntarily

report results to these databases. The

main reason they cough up the data is for marketing purposes,

according to the paper, and funds generally begin contributing their

returns once they have results worth bragging about. And since the

funds include prior returns when they first enter the database, it

leads to a “backfill bias” or “instant history bias” that boosts the

average returns. (Hat tip to

CXO

Advisory

for spotting the study last week.)

Since funds can stop reporting to the

database at any time -- say, for example, if returns are terrible --

this can cause an "extinction bias." In 2014, they note, the

attrition rate rose to 26 percent in the database studied, suggesting

that either the number of hedge funds is declining or that fewer hedge

funds are choosing to report their returns.

After scrubbing the data in an attempt

to remove the biases, they conclude: "The historical data show that

hedge funds have not, on average, meaningfully outperformed

traditional portfolios of stocks and bonds after fees. On average,

once returns have been adjusted for various sampling biases, hedge

funds do not routinely generate double-digit returns."

At any rate, another thing this study

shows is that sometimes finance professors can have sharp elbows! No

wonder so many have patches on their blazers.

©

Bloomberg L.P. |