|

CFO Journal

Exclusive

reporting and analysis for corporate-finance executives.

|

|

Tax Policies Spur Companies to Offer

Pension Buyouts |

|

By

Emily Chasan and

Kristin Lin

|

—Heath

Hinegardner |

More companies are preparing to offer lump-sum pension buyouts to

their former employees, taking advantage of tax policies that make it

possible to reduce their pension obligations and lower their costs.

In coming months, employers including Newell

Rubbermaid Inc. and E.W.

Scripps Co.will try to persuade former employees to take

their retirement money early, and in the form of a lump sum, rather

than as a series of pension payments after retirement. In making the

offers, they hope to get part of their pension liabilities off their

books, and to cut the costs of maintaining their pension plans.

Thanks to years of low interest rates, pension liabilities of S&P 500

companies are ballooning. S&P says the gap between the amounts the

companies will owe retirees and their pension assets was about $389.1

billion at the end of last year, up from $224.5 billion in 2013.

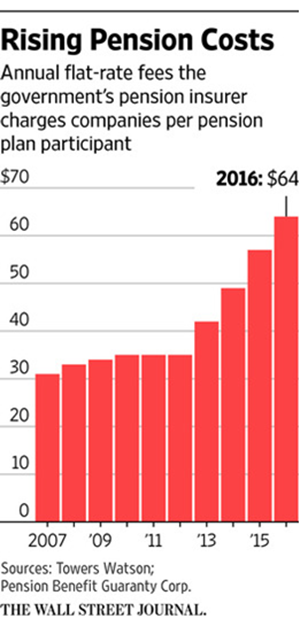

Servicing costs also are growing. Premiums companies must pay to the

government’s pension insurer this year climbed to $57 for each

pension-plan participant, up from $49 last year, and they will hit $64

next year.

Market returns, meanwhile, are shrinking. Companies expect to earn a

7% return on pension assets this year, down from 9.1% in 1999, S&P

says.

As a result, more companies are eager to take advantage of a decision

by the Internal Revenue Service to continue using its current

life-expectancy calculations, which will make it cheaper for them to

offer pension buyouts before 2017, when the IRS is likely to adopt

new, longer lifespan estimates.

Newell Rubbermaid said in August that it plans to offer 3,300 former

employees a lump-sum pension buyout to “reduce the size” of its

pension obligation and related expenses—its second lump-sum offer in

two years. The offer is equivalent to about $120 million of its total

$1.73 billion pension liability.

Last September, Newell Rubbermaid, which is based in Oak Brook, Ill.,

offered 5,700 former employees the chance to cash out their pensions.

Typically, about 50% of former workers accept such offers, it says.

A spokesman for the company declined to elaborate.

Media company E.W. Scripps said last month that it plans to offer as

many as 4,300 former employees lump sums or annuities, rather than

conventional pension payments. It wanted the chance to reduce

liabilities, and said it got “many requests” from former employees for

a buyout option, a spokeswoman said. The company expects about 60% to

80% of those offered buyouts to take them.

The IRS helped to fuel the trend toward lump-sum offers when it said

in July that it would put off using new mortality-rate calculations

based on longer lifespans until 2017. That suddenly made it cheaper

for companies to offer pension buyouts now than in the future. The new

assumptions that people will live longer will make lump-sum offers

more expensive to companies.

“We’re warning clients that if you want to shed this liability, do it

now or by the end of 2016, because it is just going to be a different

ballgame in 2017,” said Amy Gentile, senior actuarial consultant at

Findley Davies, who advises corporations on pension benefits.

For former employees, a lump-sum buyout is often

a bad option. In many cases, if they took the payout and

bought an annuity from an insurer, or invested the money, they would

earn less than the monthly pension income they sacrificed.

Donna Johnson, of Hannibal Mo., decided to take a lump-sum offer of

less than $50,000 in 2002 from AT&T Inc. when

it closed the office where she was a group manager. At the time, she

and her husband, Dave, said they thought they would do better by

putting the money into high-yielding certificates of deposits than in

an annuity. But “little did we know the Fed would [in effect] lower

rates to zero, and keep them there so long,” said Mr. Johnson. “The

decision has given us a little less income in retirement.”

|

Food-storage

container maker Newell Rubbermaid is one of the companies trying

to persuade former employees to take their retirement money as a

lump sum.

—Bloomberg News

|

|

Still, many people offered a lump sum will choose to take it, benefits

consultants say, and pension-plan participants may find this is a

better year to take the buyouts—if they want them.

The possibility that the Federal Reserve may raise interest rates

later this year means that the lump sums companies offer may be larger

now than in future years. If rates rise, companies can offer smaller

lump sums because their obligations shrink.

“Interest rates are the single most important factor in the size of a

lump sum,” said Stuart Schulman, a consulting actuary at Buck

Consultants, which advises companies on pensions. Some companies will

try to time their offers to the start of a rise in interest rates, but

before the new mortality rules take effect in 2017, he said.

In May, Alcatel-Lucent said

it would offer lump-sum buyouts. About 86,000 retirees and former

employees have until Sept. 25 to tell the company their decisions,

according to the company. .

Payments will be made Nov. 2 to those who elect the buyouts, an

Alcatel-Lucent spokesman said

The IRS said in July that it would no longer allow companies to make

lump-sum offers to people who had already retired. “There’s not going

to be another lump-sum offer…people know that,” said Frank

Minter, pension director for the Lucent Retiree Organization.

Walt Greenwood, a retiree who lives in Everett, Wash., said he chose

not to take Alcatel-Lucent’s lump-sum offer. He calculated that he

would have to earn near 7.5% annually to do better than his current

pension. “And that ain’t happening,” he said.

.”

|