|

THE

WALL STREET JOURNAL.

Markets

|

Financial Services |

Hedge Funds

Giant Hedge Fund’s Radical Idea: Performance Guaranteed or Your

Money Back

By hedge-fund standards, their system is nearly unheard of

By

Rob Copeland

Sept. 10, 2015 12:15 a.m. ET

BOSTON—Hedge-fund

managers have long clung to a doctrine of high fees in good years and

bad, minting billionaires and riling investors along the way.

A pair of former Harvard

University endowment executives have built the world’s largest

stock-focused hedge fund with the opposite approach. Robert Atchinson

and Phillip Gross let investors in their $28 billion Adage Capital

Management LP keep almost all of their trading gains—and promise

refunds if the fund’s performance falters.

By hedge-fund standards,

the practice is nearly unheard of, and this year it may be

particularly costly. Adage has underperformed the S&P 500 through

August. If they can’t turn things around by the end of the year,

Messrs. Atchinson and Gross may hand out the biggest refunds in their

firm’s history.

Hedge-fund managers

typically collect about 2% of investors’ assets under management every

year and about 20% of profits—whether they beat the markets or

not.That has put the industry under increasing pressure for what is

viewed by critics as a heads-I-win, tails-you-lose proposition. Even

managers who fall short of their benchmarks can earn hefty paychecks

simply by riding markets higher.

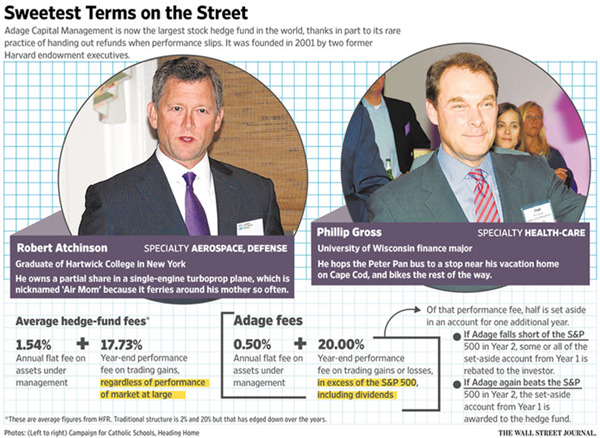

At Adage, Messrs.

Atchinson and Gross charge 0.50% of assets, less than at even many

actively managed mutual funds. They also pay themselves only for

trading profits that beat the S&P 500, including dividends—they take

20% of the returns above the S&P. And they pay back up to half of

those fees if they fall short of the benchmark in the subsequent year.

Its system pays off for

Adage in one important way: It collects its full incentive fees even

if it loses money, as long as it beats the benchmark. Most fund

managers collect performance fees only if they produce positive

absolute returns.

Adage is getting harder

to dismiss as an anomaly. The firm has nearly doubled in size over the

past four years and is now one of the world’s 10 largest hedge funds.

Its approach also reflects a bigger structural change in the industry.

Many of the public retirement plans and other institutional investors

that have poured money into hedge funds for years have hit their

limits on what they can allocate to the sector. To keep the gas pedal

on growth, hedge-fund managers are increasingly recasting themselves

as something closer to staid money managers like Fidelity Investments.

In many cases, that means taking a different tack on fees.

For instance, a new wave

of single-bet deals, known as co-investments when sold by firms like

Magnetar Capital LLC and Trian Fund Management LP, often carry

half-off prices on performance fees compared with traditional hedge

funds.

“That’s how I think the

world should look,” said Jack Meyer, the former head of Harvard’s

endowment. Mr. Meyer’s $10 billion Convexity Capital Management LP

only collects performance fees when it exceeds a market benchmark.

“I’m surprised it has taken the world so long to get there,” he said.

Despite the drumbeat for

change, hedge funds as a group haven’t altered their practices. Money

continues to pour into the $2.9 trillion industry as plenty of wealthy

investors still appear willing to pay high fees for access to

complicated strategies and the promise of protection against market

swoons. The average hedge fund charges a 17.7% annual incentive fee,

down from 19.3% at the start of 2008, according to HFR Inc.

Still, the industry has

come under an unusual amount of pressure that threatens its ways of

doing business long term. The California Public Employees’ Retirement

System, the nation’s largest public pension, said last fall it would

eliminate its entire $4 billion investment in hedge funds due in part

to concerns about high costs, and other public pensions have followed

suit.

From offices high in

Boston’s John Hancock Tower, Adage’s founders preside over an

operation that bears little resemblance to most hedge funds. There is

no central trading desk or bullpen area to swap ideas, people familiar

with the firm said.

Investment analysts, 26

in total including the founders, work silently in separate offices

ringing the floor. Six golf putting holes dot the space, people

familiar with the firm said, though they are rarely used except for a

half-hour tournament each December in which the winner gets no money.

A person who has been inside described it as a “library.”

Adage’s founders still

make plenty of money. Last year, the founders and staff split an

estimated $400 million in gross earnings after the firm’s main fund

rose 18.4%, people familiar with the matter said. Still, that is less

than a third of the more than $1 billion they would have collected

under a typical hedge-fund fee structure.

The founders break from

tradition in small ways, too. Mr. Atchinson drives a seven-year-old

Nissan Altima, and Mr. Gross takes the Peter Pan bus to his summer

home on Cape Cod.

“That’s just how they

approach life in general,” said Timothy Peterson, founder of Regiment

Capital Advisors LP and a former Harvard colleague of the founders.

“They feel very comfortable not being the center of attention.”

Because of its unusual

practices, Adage is viewed by its large investors as its own breed.

The University of California system’s $98 billion endowment has $1.4

billion riding on Adage—more than in any other stock investment except

for three low-cost index funds, which it considers to be in the same

category. Endowment Senior Managing Director Scott Chan said, “a lot

of people would call them a hedge fund,” but that he isn’t

particularly concerned about the distinction.

Since it was started

with $3.8 billion in October 2001, Adage has produced an average

annualized return, after fees, of about 9.7%, beating the S&P 500’s

6.4% pace, including dividends. The average stock-focused hedge fund

averaged 5.3%. Adage is down 3.53% this year through the end of

August, worse than the benchmark’s drop of 2.88%, including dividends.

Until this year, Adage

fell short of the benchmark and passed out refunds only twice. That

happened in 2002 and 2008, after it lagged behind the S&P 500 by 0.18

percentage point and 0.75 percentage point, respectively.

Unlike most hedge funds,

which juggle a variety of offsetting bets, Adage holds far more

bullish bets than bearish ones and keeps its proportion of the wagers

static. Bets on industries must be equal, percentagewise, to that

sector’s representation in the S&P 500. That means the firm’s more

than 1,500 stock positions tend to ride the ups and downs of the

benchmark. Any difference comes from individual stock picks, such as

the firm’s roughly $500 million position in Puma Biotechnology Inc.,

which has more than quadrupled in value since the start of 2013.

Messrs. Atchinson and

Gross met as investment analysts in the mid-1980s at Harvard’s

endowment. Mr. Atchinson, 57 years old, traded mostly aerospace and

defense firms, while Mr. Gross, 55, focused on drug companies and

other health-care stocks.

When Mr. Meyer took

charge of the endowment in 1990, he put his traders on notice: Beat

the benchmark or find a new job. Many left. Messrs. Atchinson and

Gross took on the challenge, initially topping the benchmark by 0.50

percentage point and more in subsequent years. They got rich—Harvard

paid them a bonus of around 4% of their outperformance, at peak

amounting to more than $10 million apiece—but drew scorn from some

alumni and professors unhappy about the hefty paydays for an academic

institution.

In part because of the

scrutiny, Mr. Atchinson persuaded Mr. Gross to leave in 2001. They

took with them an 18-person team and $1.8 billion day-one investment

from Harvard in exchange for an agreement, since phased out, to tithe

a portion of their firm’s future earnings to the school.

The founders’ move from

academia to hedge funds came with an added bonus: a chance to

refashion themselves as symbols of frugality after years of criticism

for their pay. Adage’s unique position, with one foot inside the

lucrative hedge-fund industry and one foot out of it, is perhaps most

plain on weekends during the summer.

Like many hedge-fund

managers, Mr. Atchinson, who goes by Bob, heads to his vacation home

on Nantucket. Unlike his peers, Mr. Atchinson usually hops on a

commercial Cape Air flight. When he does fly private, it is on “Air

Mom,” his name for the single-engine turboprop in which he owns a

one-eighth share and often ferries around his mother.

Back at Boston’s Logan

Airport on Monday mornings, he waits for a taxi to take him into the

office.

Write to

Rob Copeland at

rob.copeland@wsj.com

|