|

THE

WALL STREET JOURNAL.

Markets

|

Your Money

|

Weekend Investor

Some Funds in Your 401(k) Aren’t Really Mutual Funds After All

Collective investment trusts, or CITs, have lower fees but less

transparency

|

Fidelity Investments has joined a growing number of companies

using collective-trust versions of actively managed mutual

funds. The fees on the trusts are about 25% to 50% below the

lowest-cost shares of the mutual funds. PHOTO: BRIAN

SNYDER/REUTERS |

By

Anne Tergesen

Sept. 25, 2015 5:30 a.m. ET

Don’t look now, but the

mutual funds in your 401(k) may not be mutual funds after all.

In recent years, more

401(k) plans have replaced the mutual funds in their investment

lineups with collective investment trusts. These investments look and

act a lot like mutual funds, but generally have lower fees and

disclose less about their inner workings to 401(k) participants.

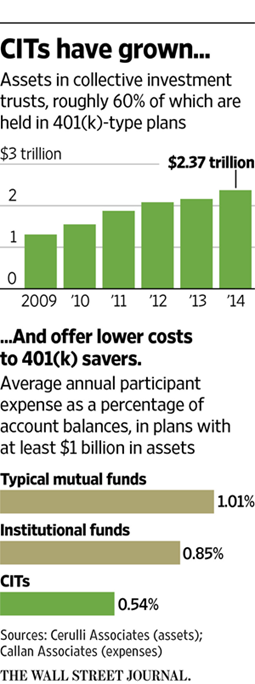

Also known as collective

trust funds, such investments currently account for $2.4 trillion, or

16%, of the $15 trillion in 401(k)-style and pension plans, up from

$1.3 trillion (and 12.7% of the total) in 2009, according to the

Investment Company Institute and Cerulli Associates, a research firm

that specializes in the asset-management industry. The trusts are

accounts available only to retirement plans. They are sponsored by

banks and trust companies and are primarily overseen by banking

regulators, rather than subject to mutual-fund rules enforced by the

Securities and Exchange Commission.

By and large, experts

say, the trend has been positive for 401(k) investors. For 401(k)s,

“collective trusts are often the lowest-cost option on the market,”

says Nathan Voris, director of sponsor and workplace investments at

Morningstar Inc.

Many collective trusts

track indexes, like index mutual funds. Over the past two years,

Fidelity Investments joined a growing number of companies introducing

collective-trust versions of actively managed mutual funds, when it

made the move with eight funds, including Fidelity Contrafund and

Fidelity Low-Priced Stock Fund. The fees on the trusts can “be as much

as 0.2 or 0.3 percentage points” cheaper than the shares of the mutual

funds, says Chuck Black, Fidelity’s senior vice president of

investment services.

Savings of that

magnitude aren’t unusual. According to investment consulting firm

Callan Associates Inc., participants in 401(k) plans with $1 billion

in assets pay an average of 1.01% in fees for an investment lineup of

retail mutual funds. Average participant costs decline—to 0.85%—when

these plans use institutional share classes of the same mutual funds,

an option available to most 401(k) plans, says Lori Lucas,

defined-contribution practice leader. But with collective trusts,

average costs fall to 0.54%—“almost half the retail price,” she adds.

Collective trusts’ cost

advantages stem mainly from the fact that they are exempt from the

Investment Company Act of 1940, which governs mutual funds. Funds are

required to deliver prospectuses and periodic reports to investors, as

well as to make certain filings to the SEC. Without those rules,

trusts save on legal and distribution costs, attorneys say.

Because of their

narrower audience, collective trusts also typically spend less on

marketing than mutual funds, Mr. Voris says.

The trusts’ low expenses

are attractive to employers seeking to reduce 401(k) participants’

costs amid a wave of litigation over high 401(k) fees and the 2012

introduction of federal regulations that mandate 401(k) fee disclosure

to participants.

Collective trusts—which

have been around since the 1920s—are most commonly used by the biggest

401(k) plans. But they have become accessible even to midsize 401(k)

plans with $100 million in assets or more, says Drew Billingsley, vice

president at American Century Investments. The Kansas City investment

company began offering collective trusts to 401(k)-style plans in 2007

and this summer reduced the minimum required investment on its

target-date collective trusts from $50 million to $15 million.

Still, the trusts’ lower

fees come with trade-offs. Collective trusts don’t have ticker

symbols, and 401(k) participants can’t track their performance or

compare them with other investments using public websites including

Morningstar.com, Yahoo Finance, and newspapers such as The Wall Street

Journal, which publish mutual-fund performance data.

Moreover, while

mutual-fund investors can simply download fund prospectuses and other

standardized materials from fund-company websites, 401(k) participants

in collective trusts may have to request similarly detailed documents

from their 401(k) plan or the company running the trust.

In comparison with

mutual funds, collective trusts are “less transparent,” says Brooks

Herman, head of data and research at BrightScope Inc., which tracks

401(k) plans. “It’s the tradeoff people are willing to make for their

lower fees.”

Still, as collective

trusts have caught on with 401(k) plans in recent years, many have

increased voluntary disclosures to 401(k) participants. While

collective trusts are not required to provide daily pricing, that has

become a standard feature.

On websites for 401(k)

plan participants, the information about trusts may look a lot like

that on funds. That is partly a function of trusts increasingly being

provided by banking units of big asset managers and 401(k) record

keepers.

‘Collective trusts don’t have ticker symbols, and 401(k)

participants can’t track their performance or compare them with

other investments.’

|

|

Many plan administrators

publish fact sheets that disclose information including a collective

trust’s performance and top holdings. Invesco Ltd.’s trust company,

which sponsors 45 collective trusts with approximately $60 billion in

assets, updates holdings on a monthly basis, says senior vice

president Betsy Warrick. For its collective trusts, Fidelity publishes

a document that resembles a slimmed-down prospectus, says Mr. Black.

“There is a movement

among trust sponsors to make their products look more like mutual

funds,” says Ms. Lucas. “More and more trusts are offering

prospectus-like documents. They recognized that plan sponsors and

participants want that level of transparency.”

Under the federal rules

for 401(k) fee disclosure, meanwhile, plans must disclose in annual

statements distributed to participants the cost to workers of

investing in the plans and the performance of the investment options,

including any collective trusts.

Collective trusts must

also issue certain disclosure documents to employers. Examples include

an audited annual financial statement detailing the collective trust’s

fiscal year-end holdings or a document—often called an offering

memorandum or an offering circular—that broadly resembles a

mutual-fund prospectus, according to John Schadl, principal and head

of Vanguard Group’s Erisa and Fiduciary Services.

Many of those documents

are available to 401(k) participants upon request, he adds.

Write to

Anne Tergesen at

anne.tergesen@wsj.com

|