|

THE

WALL STREET JOURNAL.

Markets

Companies to Workers: Start Saving More—Or We’ll Do It for You

Firms are boosting the automatic retirement-savings rate—and

finding little pushback from employees

By

Kirsten Grind

Oct. 15, 2015 5:33 a.m. ET

Bosses are turning to a

new way of convincing employees to save more: make them do it.

Companies from Apache

Corp. to Google Inc. to Credit Suisse Group AG have boosted the

percentage of worker paychecks automatically diverted to 401(k) plans

well above the long-held standard of 3%.

Some are setting aside

as much as 10% of their workers’ money or automatically increasing the

amounts by 1% a year unless employees opt out. But not all are

matching the increased savings with company contributions.

The moves are the latest

attempt by companies to transfer the burden of retirement costs to

workers. Millions of Americans

aren’t putting enough money aside,

despite reforms designed to bulk up nest eggs and encourage employees

to sock away more.

There are incentives for

companies to urge more-aggressive savings. They want to ensure they

can make room for younger employees and aren't left with an aging

workforce that doesn’t have enough money “to retire and move on,” said

Douglas Fisher, Fidelity Investments’ head of policy development on

workplace retirement.

Houston oil producer

Apache was among the companies to test out higher rates. It boosted

its automatic employee contribution to 8% in 2012 as it tried to

attract new workers. Its 401(k) costs have increased by between $4

million and $5 million annually as Apache matched the full amount for

employees, executives say, but roughly 97% of its employees now

participate.

“If I put in less than

8%, I’m throwing money away,” said Chris Lurix, a 44-year-old Apache

systems analyst in Houston, who cited the company’s willingness to

match the higher savings rate as a partial reason why he took a job

there three years ago.

About 40% of working

households with those aged between 25 and 64 have no retirement

savings, according to a study released last spring by the nonprofit

National Institute on Retirement Security. For those that do, the

median balance for households with workers approaching retirement age

is $104,000, a rate that experts say is one-fifth of an ideal balance,

based on a retirement age of 67.

“The typical American

household has almost nothing saved for retirement,” said Nari Rhee,

manager of the retirement-security program at the Institute for

Research on Labor and Employment.

Many employers in recent

decades shed costly retirement obligations by eliminating traditional

pensions that guarantee a set payout for life and replacing them with

tax-deferred 401(k) plans where employees are largely responsible for

saving and investment choices.

|

|

An Apache Corp. worker at a drilling rig in Mentone, Texas.

Apache is among companies that have boosted the automatic

savings rate for employees.

Photo: Spencer Platt/Getty Images

|

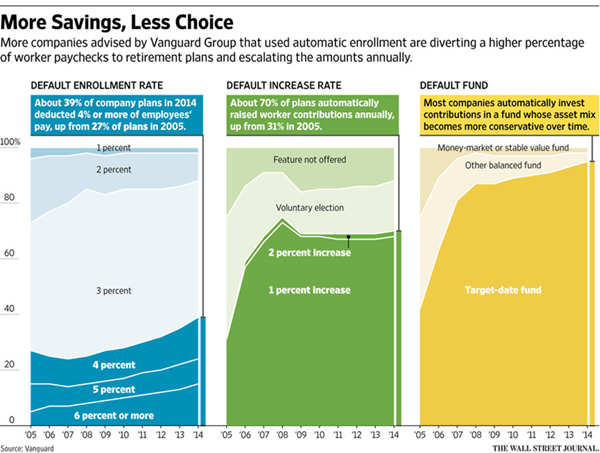

Millions of new savers

joined 401(k) plans but companies enrolled most participants at a 3%

savings rate, partly because of guidance from the Internal Revenue

Service in 1998. Companies were long reluctant to take a bigger chunk

out of paychecks for fear of stirring employees’ ire or taking on

higher costs if they matched the larger contributions.

Companies softened that

stance as they recovered from the 2008 financial crisis and looked to

attract new workers. Large money managers also lobbied employers to be

more aggressive.

The number of plans with

contribution rates above the old default rate climbed to 40% for the

first time in 2013, according to the latest data available from the

Plan Sponsor Council of America, compared with 23% in 2006. More are

currently discussing moves higher, according to industry consultants

and money managers.

Google began boosting

its automatic savings rate in its 401(k) plan from 4% in 2008 to 6% in

2010, according to retirement researcher BrightScope Inc.. It now

enrolls employees at 10%. John Casey, Google’s director of

international benefits, said in a statement that the company wants

“Googlers saving for the long-term so they can have the retirements

they want.”

|

|

‘The typical American household has almost nothing saved for

retirement.’

—Nari

Rhee, Institute for Research on Labor and Employment.

|

Fidelity, Vanguard Group

and other large money managers also benefit by collecting more fees on

assets under management. Fidelity manages accounts for 13 million

401(k) investors across 21,000 plans, and Vanguard manages retirement

accounts for 3.6 million people and 1,900 plans.

Companies that have

bumped up the default savings rate say they’ve been surprised by the

lack of pushback from employees, who are free to lower their savings

rate or opt out of the automatic increases.

Credit Suisse braced for

complaints last year when it upped its initial automatic savings rate

for new employees to 9% from 6%. It did so after years of experiencing

lackluster interest from the firm’s roughly 8,500

employees—specifically younger workers—in the U.S. when meeting to

discuss increasing retirement savings, said Joseph Huber, chairman of

the bank’s pension-investment committee.

But Mr. Huber said the

bank heard concerns from only two people, who weren’t previously

putting any money into their 401(k) plans. Credit Suisse also decided

to automatically increase the default rate by 1% a year until an

employee reaches 15%. It doesn’t match contributions up to the highest

rate.

“It’s companies’ biggest

fear and it was radio silence,” he said.

Jeffrey Barnett, a

24-year-old clinical research assistant at Ohio State University who

makes about $28,000 a year, said some of his co-workers grumbled at

the university’s 10% default savings rate. But it doesn’t bother him.

“It has definitely put

employees in a good position, whether or not they feel that way from

the start,” Mr. Barnett said.

Write to

Kirsten Grind at

kirsten.grind@wsj.com

|