If

the Department of Labor’s Fiduciary proposal goes into effect,

advisors may find themselves taking a closer look at low-cost

annuities.

The push by regulators for greater advisor accountability and more

prudent investment recommendations will be a boon for products that

offer client-friendly features and lower costs. This may encourage

more annuity providers to compete on price.

Advisors have slowly embraced low-cost annuities in recent years, and

their sales have jumped from $3.6 billion in 2010 to nearly $6 billion

in 2014, according to the Insured Retirement Institute, the trade

association that represents annuity sellers. The IRI defines low-cost

as variable products that have no sales commissions or surrender

charges and keep their annual expenses under 1%.

Bells and whistles like income guarantees, living benefits and payouts

indexed to stock market returns have increased these products’

popularity among some advisors and their clients. Although relatively

unheard of 15 years ago, there are now more than 220 living benefit

products in the variable annuity space, Morningstar analyst John

McCarthy says.

DRILLING DOWN ON VARIABLES

Variable annuities are complex beasts. Since they are amalgams of

mutual funds with myriad benefits, they have several layers of fees.

The mortality, expense and administrative charge pays for the cost of

the insurance, administration and commissions; this is expressed as a

percentage of the amount in the account. According to AnnuityFYI, an

online annuity service, the average industrywide fee is 1.4%. Charges

below 1% put the product in a low-cost category. So-called no-load

annuities don’t pay commissions.

Insurance companies don’t want customers withdrawing too much of their

money too quickly, so they impose surrender fees if funds are

withdrawn before a certain time period (seven years on average).

Low-cost products don’t have surrender fees, and there are also short

surrender products that are subject to withdrawal surcharges for only

a few years.

Variables also charge subaccount fees, known as expense ratios in the

mutual fund world. These are what fund companies charge for managing

funds within the annuity, and they vary widely from more than 1% to

under 0.3%.

There are also miscellaneous fees such as maintenance charges, which

are usually flat fees. The industry average is $35, which may be

waived for accounts over $50,000.

SPECIAL RIDERS

As

with most insurance products, clients pay extra for special riders

such as lifetime income and enhanced death benefits. Those options

tend to add 0.4% to 1.1% to annual expenses. Here are two examples of

popular riders and their average cost:

Guaranteed Minimum Income Benefits:

For clients who want to lock in a payment, these riders guarantee a

minimum monthly benefit regardless of the underlying performance of

the product. But they typically don’t kick in until after the 10th

year of the contract and they apply only when the client annuitizes.

But they also add from 1% to 1.15% to the annual expense.

Lifetime Income Benefits:

A form of longevity insurance, this is another failsafe that

guarantees a payment even if the account balance goes to zero. Say

your client purchased a $100,000 annuity with this rider guaranteeing

a 5% return. If the balance went to nothing, there would still be a

$5,000 annual withdrawal.

To

cover a spouse along with your client, you can also buy a joint and

survivor product. Expenses are 0.35% to 1.25% annually.

Keep in mind that there are hundreds of variations of these products

with specific rules on withdrawals, rates of return and other

contingencies. The more features you want, the more you’ll have to vet

the product for its suitability and cost.

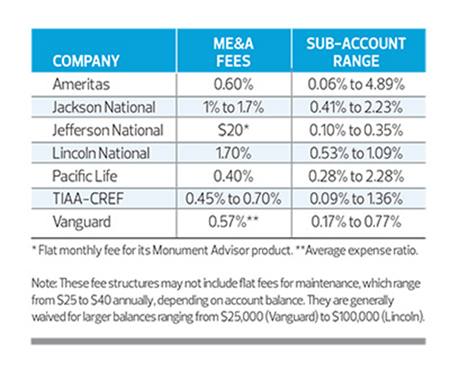

THE LEADING PROVIDERS

There are a handful of companies that are acknowledged to have the

lowest cost structures. All of the variables offer an array of mutual

funds, but they vary in cost depending upon their objective.

You’ll pay the least for a broad-index fund — like those offered by

Vanguard — and the most for those with more specialized objectives.

The average subaccount expense is 0.96%, which is slightly lower than

stand-alone mutual funds, according to Morningstar.

Here’s a sampling of mostly direct-sold products that don’t pay

commissions:

Generally, the largest low-cost providers have been in the business

for decades, are active in the institutional market and offer

economies of scale. TIAA-CREF, for example, a retirement plan manager

(originally for college professors), offers an Intelligent Annuity

product with subaccount fees as low as 0.09% annually.

Pressure to achieve cost savings has led to quite a bit of

cross-pollination among these products. Vanguard, for instance, a

traditional low-cost mutual fund complex, may be represented in other

plans, such as Jefferson National. Likewise, you can find low-cost

funds from Dimensional Fund Advisors in several annuity programs.

Advisors seeking bargains for their clients can take advantage of this

competition.

“If an appropriate client situation surfaces, the lowest-cost variable

annuity that I am aware of is the Jefferson Nation Monument Advisor

annuity,” notes Gil Armour, a CFP with SagePoint Financial in San

Diego. “Instead of a hefty 1.25% mortality and expense ratio like most

annuities, they charge a flat $20 per month,” he explains. “In the

right situation, that could save the client a lot of money in ongoing

fees.”

ANNUITIES AND THE FINANCIAL PLAN

When choosing among annuities or deciding whether to use an annuity at

all, an advisor must consider a variety of factors.

Taxes are one consideraion. Since withdrawals are taxed at full

marginal rates as ordinary income, the only advantage of annuities

from a tax perspective is their ability to defer them. A tax-efficient

portfolio of mutual funds or exchange-traded funds that generates

capital gains at a lower tax rate may be more suitable for many

clients.

The use of riders is another factor. These require a further

cost-benefit analysis, since advisors have to weigh the additional

expense against alternative strategies to protect their clients’

future income.

“Riders may be more expensive than a mutual fund or managed

portfolio,” says Joe Heider, president of Cirrus Wealth Management in

Cleveland. “They cost from 1.25% to 1.5% extra. Are they worth it?”

Besides comparing annuities’ costs and features, another basic

consideration is the financial strength of the issuing company.

annuity selection

But annuity selection depends greatly on clients’ inclinations and

risk tolerance. Some may insist on a guaranteed income benefit and be

willing to pay the extra cost. Others may be more interested in saving

money and boosting returns with a lower-cost platform. In that case,

you may be able to switch them through a 1035 Exchange of similar

insurance products into a no-load, no-surrender fee annuity with low

subaccount fees.

Selecting an appropriate annuity also depends on the kind of advisor

you are. Those tied into broker-dealers or wholesalers may access

entirely different products than advisors who operate as fee-only

planners under a fiduciary model.

Eve Kaplan, a fee-only certified financial planner in Berkeley

Heights, N.J., says she typically avoids recommending non-qualified

variable annuities in part because of higher taxes on withdrawals.

“I’m not sure why you would want to invest in a variable annuity with

after-tax dollars and incur ordinary income tax rates on capital

gains,” she says, “when you can benefit from the current [lower]

capital gains rates available in taxable accounts.”

But for advisors who recommend annuities, the Labor Department’s

proposed fiduciary rules for retirement advice have the potential to

be a game changer.

If

commission-based advisors are forced to hew to a new fiduciary

standard, they will inevitably pay much more attention to the

lowest-cost products and rethink some of the retirement income

strategies they offer.

John F. Wasik is the author of Keynes’s Way to Wealth and 13 other

books. He is also a contributor to The New York Times and

Morningstar.com. Follow him on Twitter at

@johnwasik.

|

|

© 2015 SourceMedia. All rights

reserved. |

|