|

Your Money

Financial Advice

for Women, From Women

NOV. 9,

2015

|

Amanda Steinberg,

left, and Michelle Smith are joining forces to create an online

investment firm called WorthFM, a financial services firm aimed

at women.

Credit Jordan Matter |

It’s

been a long time since a talking teenage Barbie doll uttered

the words, “Math class is tough!” That was 1992, and the

uproar that ensued caused Mattel

to banish the words from Barbie’s vocabulary.

Today,

as men’s and women’s traditional roles continue to blur, companies are

even more careful not to reinforce gender stereotypes.

Yet at

the same time, two new online investment firms — known as robo-advisers

— are introducing products that suggest women need extra hand-holding

with their money. They are offering financial and investment advice

tailored just for females.

Women

are increasingly their households’

breadwinners, and they are more

likely than men to enroll in and complete

college. Women are also a growing

market, exercising decision-making control of an estimated

$11.2 trillion in investable

assets, according to the Center for Talent Innovation.

But do

they really need specialized help — any more than the sort of

personalized attention that many consumers crave? Or are these firms,

backed by big investors, simply grasping for women’s growing wallets?

Amanda Steinberg — founder of

DailyWorth, which sends its 1.2 million female subscribers

daily emails about money — will soon introduce a robo-adviser for

women with

Michelle Smith, whose firm

Source

Financial Advisors caters to multimillionaire women who

have been divorced. Their new service,

Worth Financial Management, will

make its debut next year. But the gendered focus isn’t necessarily

being driven by women’s need for extra help, Ms. Steinberg said, and

is instead the response to a dialogue she has had with her subscribers

for nearly seven years.

“I

know they don’t like what is out there,” Ms. Steinberg, a programmer,

said of her subscribers, who, on average, are 38 years old and earn

$78,000. “My mission from the beginning was about empowering women to

build net worth. Not to get better at budgeting, not to save $10 when

buying flowers for their dinner party. It was to give them control

over their futures.”

Women

surely face their own set of challenges. They generally earn less than

men, are more likely to take breaks from the work force, and live

longer, all intractable issues that demand societal and policy

changes, like less male-focused workplaces and policies.

Helping women account for these handicaps is what is driving

Sallie Krawcheck, a former Wall

Street executive, into the same business: She recently announced

plans to introduce her own robo-adviser,

Ellevest,

next year.

“Men

have more room for error,” said Ms. Krawcheck, who became well known

on Wall Street after she graced the cover of Fortune in 2002 as one of

Wall Street’s “last honest analysts.” She has held high-ranking

positions at Bank of America and

Citigroup, and along with her co-founder, Charlie Kroll, raised $10

million for her new venture from several heavy hitters (mostly men) in

the financial industry.

She

declined to provide details about the service, but here is hoping Ms.

Krawcheck will veer far from her Wall Street roots and use her stature

to provide the kind of low-cost, comprehensive advice that is still

more difficult for nonwealthy people to come by.

The

women at WorthFM, as the firm will be known, both divorced single

mothers with an unstoppable entrepreneurial drive, have already mapped

out their approach and raised $2 million from investors — all divorced

women. They will focus on the mass affluent, generally someone with

less than $500,000 to invest. That amount is usually not enough to

capture the attention of many human advisers (who generally charge 1

percent of assets) because of sheer economics.

But an

integral part of WorthFM’s approach is to act a tad more like a human

adviser — that is, build a relationship first and then get into all

the money stuff.

So how

does one go about building a relationship with a robot? Apparently, by

making a woman feel that she has been heard.

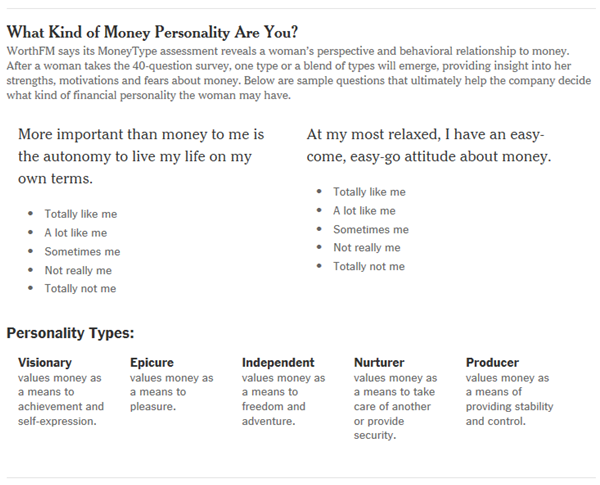

To do

that, they need to learn how she relates to money. They will ask her

to complete a “MoneyType”

assessment, a 40-question survey the company developed with a

psychologist. The results, they say, will reveal her perspective and

behavioral relationship with money — one dominant type or some

combination of the five types may emerge.

With

that information in hand, the service will personalize the woman’s

path through the site, taking into account her financial circumstances

and knowledge about finance.

The

women who value money as a means to pleasure might first be presented

with a video featuring the co-founders, in an attempt to engage them.

Those who see money as a means to stability and control might see a

savings chart or more explicit directions on what to do next. The

robot will also take note of how many times the client logs in.

The

idea is to keep the user interested and to build her confidence. “Our

job is to get to know her and reflect back to her what is important to

her,” Ms. Steinberg said. “We are feeling out her level of intensity

so we can be responsive to her instead of pushing her.”

Ms. Smith said it amounted to digitizing the type of experience you

can have in a human adviser’s office. “Good advisers do this first,”

Ms. Smith said. “They don’t come out with their proposal and say,

‘Pick a plan! Pick a plan!’ ”

|

Sallie Krawcheck,

a longtime Wall Street executive, will soon introduce her own

robo-adviser, Ellevest.

Credit Tony Cenicola/The New York

Times

|

|

The

overriding goal, however, is the same for all users. Once an account

is in place, the site will guide users to set up two separate pots: a

short-term savings account, with the goal of contributing three months

of net income (you can link to an outside account); and a longer-term

account for

retirement savings (like an

individual

retirement account or a taxable

brokerage account). They will recommend one of five diversified

portfolios of low-cost

exchange-traded funds, though

more account types and funds are expected to come later (including

joint accounts that can be held with male partners or husbands).

Users

will have the ability to automate their savings, but within six

months, the service plans to introduce an algorithm to figure it out

for them. Based on recurring patterns in the user’s income and

expenses, it will automatically shuttle a safe amount into savings or

investments, similar to what the

Digit app does now, with the

user’s permission.

“The

focusing on where all of your money goes is a frustrating and

impossible process for a lot of people,” Ms. Steinberg said. “So we

are inverting it by thinking about your buckets. It’s not ‘Do I go out

to dinner or do I not?’ It’s savings.”

Ms.

Steinberg said her firm planned to measure its success with one

yardstick: It aimed to increase each women’s net worth by 30 percent

over five years.

Building one’s net worth is just as much about chipping away at debt

as it is as building savings. And one of the biggest weaknesses of

robo-advisers is that they fail to address a person’s entire financial

picture as a human adviser might, instead focusing on the handful of

investment accounts they offer. Ms. Steinberg said she wanted to

address the whole picture, including debt management, but that would

come later.

WorthFM will charge one all-inclusive fee — including underlying

investments — that is generally competitive with those of other

robo-advisers, which

charge anywhere from 0.15 to 0.50

of total investable assets. (They declined to provide specifics

because they hadn’t yet filed pricing data with regulators.)

According to a 2009 report by the Boston Consulting Group, there is a

huge opportunity to capture women’s wallets — “one that can be

immensely profitable for financial institutions,” the report said,

noting that women continually feel exasperated by the poor way

financial companies treat them.

Robo-advisers

deliver the same product to everyone. But even some of the leading

firms in this category, including

Betterment and

WealthFront, each with $3 billion

under management, admit that their customers are largely male.

WorthFM and Ellevest aren’t the first to try to win women’s wallets.

LearnVest, which sells

comprehensive

financial advice, started in 2009

as a budgeting website directed at women, but it eventually broadened

out to include men, too. In March, it was acquired by Northwestern

Mutual. With only about 10,000 customers paying for its standard

financial plans at that time, its fate is now unclear.

“The

economics of the industry are tough,” said Manisha Thakor, director of

wealth strategies for women at Buckingham, an investment advisory

firm.

Interestingly, women may actually be better savers and investors than

men. “Women do it a little bit better,” said Jean Young, a senior

research analyst at Vanguard, who recently completed a

study that found that females

tend to save more, on a percentage basis, in their 401(k) plans than

their male counterparts.

“They

are more likely to be in the plan, they save more when they are in the

plan, they trade less and they take advantage of professional

management,” she added.

Their

problem? Even though they squirrel away more, the average man’s

account balance is about 50 percent larger, largely because women earn

less on average.

And

that can’t be solved by any robo-adviser.

Correction: November 6, 2015

An earlier version of the picture caption with this column reversed

the identities of the two women shown. Amanda Steinberg is on the left

and Michelle Smith on the right.

A version

of this article appears in print on November 7, 2015, on page B1 of

the New York edition with the headline: Financial Advice for

Women, From Women .

© 2015 The

New York Times Company |