‘Enough is enough’: Wall Street analysts want Aramark top execs pushed

out as growth lags

by Harold Brubaker,

Updated: March 25, 2019- 6:30 AM

|

Ben Hider / NYSE

|

Misguided management is stifling growth at Philadelphia’s

food-and-facilities giant Aramark, according to two Wall Street

analysts who want an activist investor to step up and push out the

current leadership.

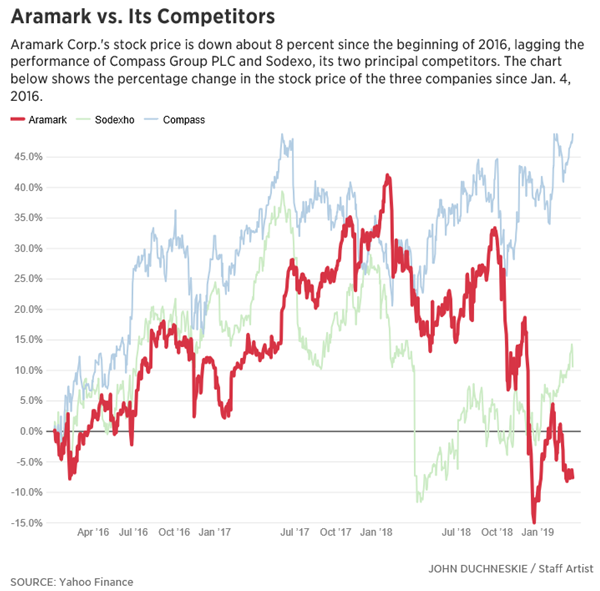

Aramark Corp. is a giant in the world of food and support services,

but the company’s 3 percent annual revenue growth significantly lags

that of its largest rival, Compass Group PLC, for one main reason. It

doesn’t win enough when it competes against Compass and others for

long-term contracts to run dining services for schools, universities,

hospitals, and other businesses, Dan Dolev and Sean Kennedy, analysts

at Nomura Instinet, argued in a March 18 report.

“What we’re saying is, you’re only winning 33 percent, compared to

Compass winning 50 percent plus," Kennedy said last week. "Part of the

reason for that is your offering isn’t as good as Compass’s offering.”

The rebuke by Dolev and Kennedy comes as Aramark shares have

underperformed the Standard & Poor’s 500-stock index and Compass over

the last five years, and follows a period of turmoil this year caused

by the decision to not pay annual bonuses to thousands of lower-level

managers. Aramark blamed a company-wide profit criteria — but the

managers were never told in advance about that.

‘Enough is enough’

The analysts don’t see much changing under the current management team

of Eric J. Foss as chief executive and Stephen P. Bramlage Jr. as

chief financial officer, because the financial incentives aren’t

aligned with long-term growth at the company.

Dolev and Kennedy told The Inquirer that they would like to see an

activist investor take a large position in Aramark and say “enough is

enough, and push management out,” because “they are definitely not

leveraging the full power of the business."

Aramark responded with CEO Foss’ familiar investor pitch: The company

has significantly increased revenue growth rates in the five years

since going public in 2013. That growth translated into

“industry-leading” earnings growth from 2013 to 2018 and landed

Aramark among “a handful of companies” with double-digit percentage

gains in adjusted earnings per share for five consecutive years.

After returning to the stock market in December 2013 at $20 per share

after six years of private-equity ownership, Aramark’s shares went

mostly up, reaching a peak of $46 in January 2018, but since then

they’ve fallen 37 percent, closing Friday at $28.91 on the New York

Stock Exchange.

Where’s the growth?

When Aramark in December cut its target for annual revenue growth to a

range of 2 percent to 4 percent from 3 percent to 5 percent, analysts

were puzzled, especially because Aramark estimates overall annual

growth in its end markets at 3 percent, and Compass tells analysts to

expect annual revenue growth in the range of 4 percent to 6 percent.

Sodexo, based outside Paris, is a third major competitor for food

services. Compass is the biggest, with $30 billion in revenue last

year. Sodexa was at $23 billion, while Aramark was at $16 billion.

“Why do you not see Aramark being able to gain share based on some of

the improved brand position and the improved scale that you now have?”

asked Harry Martin, an analyst at Sanford Bernstein & Co., during the

Dec. 11 investor day. If the company were taking market share from

others by winning new business, Aramark’s revenue would increase

faster than the market as a whole.

Schlomo H. Rosenbaum, a Stifel, Nicolaus & Co. analyst, told Foss and

Bramlage at the same meeting that he was “just trying to get my hands

around” why the expected growth rate was not accelerating after

acquisitions and years of technology investments.

Foss said Aramark’s primary goals of growth in earnings per share and

higher profit margins can be achieved without higher revenue growth.

“The way the machine works does not require us to drive 5 percent or

even 4 percent revenue growth,” Foss said.

“I don’t think he understands what investors like," Dolev said.

"Investors want organic growth. He’s going for some margin by cutting

spending on food and support.” Dolev and Kennedy estimated that

between fiscal 2016 and fiscal 2018, Aramark cut its spending on food

by anywhere from 0.2 percent to 2 percent when it should have spent

any savings on better food offerings.

“Food has become more of a novelty. Plain old food to be fed is not

enough anymore,” Dolev said.

Elsewhere, Bramlage has said the company does not grow faster because

it needs to carefully balance spending money to win new clients with

generating cash to reduce its heavy debt load.

“I don’t think that’s the reason. To me that’s just like an excuse,”

Dolev said.

Both Compass and Aramark gain about 2 percent in revenue annually from

existing operations and lose 4 percent or 5 percent of revenue when

clients chose new providers, Dolev and Kennedy said in their report.

The big gap is in revenue from new contracts.

At Compass, that growth has been around 9 percent for the last two

years, public reports show. Aramark does not include that information

in public presentations, but Dolev and Kennedy said Aramark revenue

gain from new contacts has been around 5 percent to 6 percent in the

last three years.

New business comes from organizations that are outsourcing for the

first time or is taken from competing food-service providers.

Aramark took a hit on both counts when in 2017 Inspira Health of South

Jersey chose Compass over Aramark to provide food and cleaning

services at its three hospitals. Inspira itself had managed the

services in Elmer and Vineland; Aramark had been the provider in

Woodbury.

“We selected Compass not only on price, but we also thought some of

their values that they brought to the table, and of the priorities

that they have as a corporation, matched and mirrored ours around

patient safety, around quality, around the patient experience,” said

Todd Way, Inspira’s executive vice president of operations.

Misaligned incentives

Management incentives are part of the problem at Aramark, Dolev and

Kennedy said. Only half of Aramark’s long-term incentives are based on

core financial measures. The remainder consist of share-based

compensation that unlocks over time rather than based on meeting

targets, the analysts said.

At Compass, by comparison, 80 percent of the top executives’ long-term

incentives are based on core financial measures and 20 percent on

total shareholder returns. At Compass, the executives get no annual

and no long-term incentive payout if only the minimum threshold is

met, according to the company’s annual report.

Last year Foss, Bramlage and other top Aramark executives collected 77

percent of their annual bonus target after Aramark’s adjusted

operating income landed precisely on the minimum threshold — $974.5

million — needed for top executives to receive an annual bonus. That

amounted to $2.6 million for Foss and $546,900 for Bramlage.

For thousands of low-level managers who met the financial targets they

knew about but still got no bonus, that stung.

As a group, investors two years in a row have panned Aramark’s

executive pay practices in their annual non-binding “say on pay” vote.

The approval rate climbed to 55.8 percent at this year’s annual

meeting from 50.7 percent last year, according to Aramark’s SEC

filings.

Mary J. Mullany, a Ballard Spahr LLP partner whose specialties include

executive compensation, said that’s still a failing grade.

“If you get less than 80, you’re in trouble,” she said.

|

Copyright

2019, Philadelphia Media Network (Newspapers), LLC

|

|