|

Sizing Up

Small Caps

Phil Falcone’s Long Game

The controversial HC2

Holdings CEO is looking to repeat the success he enjoyed at HRG Group.

Shares could be worth more than double.

By

David Englander

April 30,

2016

Phil Falcone made billions for his hedge fund, Harbinger Capital, when

he bet against the housing market in 2007. He is also known for his

past legal troubles with the Securities and Exchange Commission, and

as a large owner of troubled wireless network LightSquared, now called

Ligado Networks.

Lost in the shuffle, perhaps, is his successful deal-making record at

HRG Group, a holding company that he founded, and where he took major

stakes in Spectrum Brands Holdings and Fidelity & Guaranty Life. From

2011, when HRG made its first investment, through 2014, its stock

returned 129%, versus the Standard & Poor’s 500 index’s 64%.

|

Phil Falcone, the head of Harbinger

Capital Partners Photo: REUTERS/Brendan McDermid

|

|

A new Falcone play is a venture called

HC2 Holdings

(ticker: HCHC), a company in the same cut as HRG. While small, with a

market value of just $135 million, HC2’s potential could be great, if

Falcone can recreate some of his past success.

Over the last two years, HC2 has bought cash-generating businesses at

cheap prices, often from motivated sellers. Its holdings include

Schuff Steel, a steel-fabrication company; Global Marine Systems,

which installs and services undersea fiber-optic cable; a long-term

care insurance business; and smaller stakes in about half a dozen or

so other businesses.

After a strong start, HC2 shares have dropped 60% since last June,

along with other leveraged investment companies, which have fallen out

of favor. Selling related to redemptions at some fund holders may also

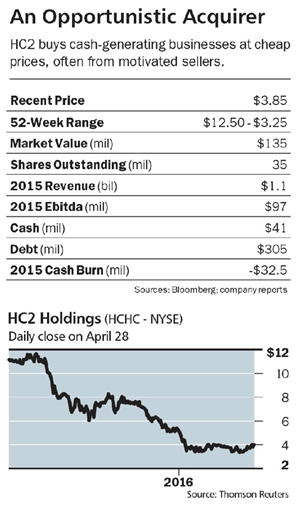

have played a part. At a recent $3.85, the stock looks attractive, but

it isn’t without risks.

HC2 is burning cash at the holding-company level,

meaning it isn’t collecting enough dividends from its subsidiaries to

cover interest and operating expenses. Still, Falcone is on the hunt

for a new deal, which could push the company toward break-even.

One holder, Chris Mittleman of Mittleman Brothers, thinks HC2 is worth

more than double its current quote. He puts the net asset value at

$8.30 a share. A new acquisition could bump that up. As cash flow

break-even gets closer, the stock, too, will probably attract a wider

group of investors.

In early 2014, HRG Group bought a large stake in a shell company

called Primus Telecom; the company was renamed HC2. Falcone became CEO

that April, and HC2 completed its first deal, a majority stake in

Schuff, in May.

Six months later, Falcone stepped down from HRG, to focus on HC2. Last

year, HRG exited its stake in the company. In 2013, as has been widely

reported, Falcone agreed to a five-year ban from the securities

industry, for borrowing from his hedge fund to pay his taxes, and for

giving preferential treatment to some clients.

LAST YEAR, HC2 GENERATED

$97 million in Ebitda, or earnings before interest, taxes,

depreciation and amortization, on revenue of $1.1 billion. Schuff and

Global Marine accounted for almost all the company’s Ebitda and

subsidiary dividends of $24.7 million. Free cash flow was negative

$32.5 million. No Wall Street analysts cover the stock, so there are

no published estimates available.

Schuff does the fabrication and

placement for structural steel in large commercial construction

projects, such as high-rise office buildings, sports stadiums, and

hospitals. Notably, it’s working on Apple’s futuristic new

headquarters in Cupertino, Calif. Last year, its Ebitda rose 15%, to

$52 million. As long as construction activity keeps up, the business

should do well.

Global Marine generates the majority of its revenue from installing

and repairing subsea fiber-optic cables for telecom companies, through

its fleet of seven ships. Half its revenue is tied to long-term

maintenance contracts, which ensure a stable cash-flow stream.

Last year, HC2 bought two long-term care insurance units from American

Financial, with a $1.4 billion portfolio of policies. Long-term care

has been out of favor, as costs have skyrocketed for insurers, and

many have exited the business.

On the March earnings call, Falcone called the industry “a little bit

misunderstood,” and added, “selectively, there’s opportunity here.”

HC2 plans to build the business by buying existing policies, not

underwriting new ones. A key part of the bet is that while people may

live longer, they will be healthier, and claims will fall.

HC2 has also invested roughly $60 million in six smaller,

venture-capital type businesses, which include natural-gas fueling

stations for trucks, a biotech with a skin-lightening technology, and

a Nascar-branded videogame developer. Even one success, there, could

be a big score.

Mittleman, a 4.4% holder, values HC2’s

91% stake in Schuff and its 97% stake in Global Marine at a multiple

of 7.5 times Ebitda. He values the VC-type investments at cost, so

they aren’t a big part of his NAV estimate. Mittleman bought his

shares last October in a $7.50-a-share private placement from HRG

Group, an offering that Falcone participated in, as well.

HC2 had $305 million in debt, and $41 million in cash, at the

corporate level, at the end of the year. It reported $158 million in

cash, across all its consolidated subsidiaries. Probably reflecting

some concern over the negative cash-flow issue, its senior bonds trade

for 89 cents on the dollar.

WHEN ASKED BY AN ANALYST

about timing for break-even, Falcone responded, “We are probably one

acquisition away from doing that. We aren’t quite there yet, but we

have adequate resources, so that we don’t have any problems.” In the

past, HC2 has sold equity, including preferred stock, to finance

deals.

At the end of 2015, HC2 disclosed it spent $54.6 million on unnamed

investments, perhaps an indication of a larger investment underway.

Falcone, who through his stock and

options owns 13% of HC2, seems to be playing a long game. “It’s all

about driving value,” he told investors and analysts. “In the end,

value will win.”

Investors who can stomach the risk could turn out to be winners, too.

E-mail:

editors@barrons.com

|