|

Strategy

What’s Your Return on Buybacks?

Managements may be biased in favor

of their own companies' valuation.

>>

Gregory V. Milano

June 3, 2011 | CFO.com | US

During informal discussions after a recent presentation to a company’s

investors and analysts, I stood with the CFO and watched in dismay as

he was barraged with questions about buybacks. He and his CEO had

presented a strong growth strategy and were commended for it, yet the

questions were disproportionately about share repurchases and not the

company’s organic and acquisitive investments. Sometimes investors

seem to overly fixate on what they perceive to be the benefits of

buybacks.

In other cases, senior executives seem to overemphasize share

repurchases, often because they boost earnings per share (EPS).

Interest rates are so low that cash in the bank contributes zilch to

net income. By distributing excess cash via repurchases, EPS increases

because net income is divided by fewer shares. I’ve heard one CFO say

that more than half of his company’s EPS growth in recent years came

from buybacks — but is that as valuable as EPS improvements from

revenue growth and margin improvements?

Do buybacks help improve a company’s total return to shareholders?

What sort of return do investors get from buybacks?

Those are critical questions, since after a lull during the financial

crisis corporate buybacks are on the rise again in a big way. During

the previous buyback wave from 2004 through 2008, the members of the

current Standard & Poor’s 500 repurchased more than $1.80 trillion

worth of their own shares, which represents $90 billion per quarter.

In 2009, buybacks declined 63% from that five-year average. In the

first quarter of 2011, however, buybacks are back up to $85 billion.

The recent torrent of buyback announcements indicates we’re in the

midst of another wave of heavy share repurchases.

So how do buybacks affect share price performance? Our research on the

buyback habits of 461 of the current S&P 500 during the five-year

buyback wave from 2004 through 2008 and the aftereffects on share

prices demonstrates, for one thing, that investing in them may not

yield as much value as investing in a company’s business.

One observation based on the research is that the 29 companies that

did not repurchase any stock during this period delivered median total

shareholder return (TSR) of positive 40%, while the overall S&P 500

index was down 19%. That was likely caused by differences in the

investment opportunity set.

Those companies with great investment opportunities don’t buy back

shares, yet they have strong TSR. It may not mean that the presence or

lack of buybacks caused the difference, but the result certainly

reinforces the notion that investing in the business is a better way

to drive the share price than buybacks. CFOs must be careful not to

allow buybacks to keep the company from making good investments in the

business.

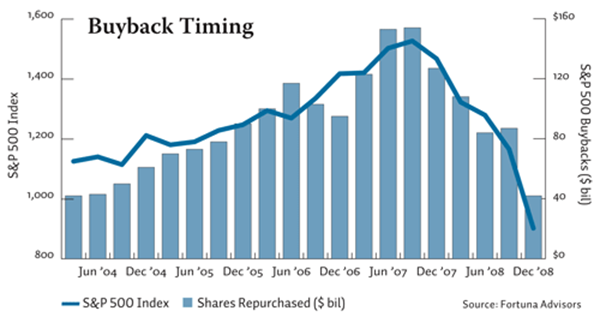

A second observation is that buyback timing doesn’t seem to follow the

“buy low and sell high” paradigm. Indeed, as shown in the graph below,

buyback timing seems to follow a “buy high” rather than a “buy low”

course. That is critical, since many companies explain their buyback

programs by claiming their shares appear undervalued. Perhaps

managements are prejudiced in their assessment of their own company’s

valuation.

We also tested the return on investment (ROI) of buyback programs by

using both a straight gain-or-loss methodology and an internal rate of

return (IRR) approach.

Overall, these companies repurchased $1.80 trillion worth of their

shares from 2004 through 2008, and the shares would have a market

value of $1.96 trillion as of April 2011, resulting in a gain of $160

billion. The top gains were registered by IBM, Exxon, and Oracle, with

the top 10 accounting for 90% of the gains.

The bottom 10 buyback companies repurchased $230 billion worth of

shares at prices that averaged 94% higher than their prices are today.

Not surprisingly, this group included many financial institutions,

with the top losses registered by Bank of America, Citigroup, and GE.

Do such results represent a desirable use of capital? We applied an

IRR approach to examine the average annualized ROI on these

“investments.” We examined the cash outflows each quarter from 2004

through 2008 and estimated the number of shares repurchased at the

average share price of the quarter. We then calculated an ROI relative

to what those shares would be worth at the April 2011 share price. The

top ROI was Netflix, with $300 million in repurchases now worth nearly

$2.7 billion, for an ROI of 94%.

The median buyback company delivered an ROI of 3%, and three out of

every four companies delivered a buyback ROI of less than 10%, a

common hurdle rate for capital investment. For companies with rising

share prices, buybacks amplified the increase. But for those with

declining share prices, buybacks exacerbated the decline. In many

cases, the only happy shareholders were the ones who sold shares back

to the company when the share price was higher.

Given common buyback strategies, such poor results are almost

inevitable. Many companies employ a pecking-order capital-deployment

strategy in which cash in excess of reinvestment needs is distributed

via share repurchases. While this strategy seems sensible, it leads to

buying back more shares when the market value has increased

significantly in response to stronger cash flows. This

capital-deployment strategy seems flawed.

What are better buyback strategies? There are two reasonable choices.

The first is to stop distributing capital based on availability and

shift to a steady buyback program that distributes a consistent sum of

cash every quarter. In effect, it means buying back more shares when

prices are low than when they are high. That may be hard to stomach in

a financial crisis, and may attract activist investors who abhor

rising cash balances during good times.

The second is to continue with the pecking-order strategy but shift

the variable portion of the distributions to a changeable special

dividend. That way leverage and cash balances can be maintained while

avoiding the typical propensity to buy back more shares when they are

expensive. Either way, the shareholder will be better off.

Gregory V. Milano is co-founder and CEO of Fortuna Advisors LLC, a

strategic advisory firm, and a regular columnist for CFO.com. |