|

THE WALL STREET

JOURNAL. |

Business

|

CFO Journal

Buybacks Can

Juice Per-Share Profit, Pad Executive Pay

Share Repurchases,

Running at Fastest Clip Since Recession, Likely to Accelerate

Through Year-End

|

|

|

Otto Steininger

|

By

Maxwell Murphy

and

John Kester

Oct. 27, 2014 7:42

p.m. ET

Buying earnings growth cuts both ways.

In the most recent quarter, one in four companies in

the S&P 500 index is expected to have juiced its earnings per share by

4% or more by snapping up its own stock, according to S&P Dow Jones

Indices. That is up from one in five at the beginning of the year.

Corporations have long bought their own shares as a way

of returning excess cash to shareholders. Reducing the number of

shares outstanding gives the remaining investors a larger stake in the

company. Buybacks also are often a sign of a company’s confidence in

its future.

The other side of the blade: Some shareholders and

analysts are questioning why companies aren’t instead plowing more

money back into their business, and they say that buybacks may serve

the interests of top management more than those of average

shareholders.

“Executives are compensated [based] on EPS,” said

Warren Chiang, a managing director at investment firm Mellon Capital

Management Corp. EPS growth, he added, is “the primary reason they do

buybacks.”

After a dip in the second quarter, companies have been

buying back their shares at the quickest clip since the recession, and

the pace is expected to accelerate through year-end.

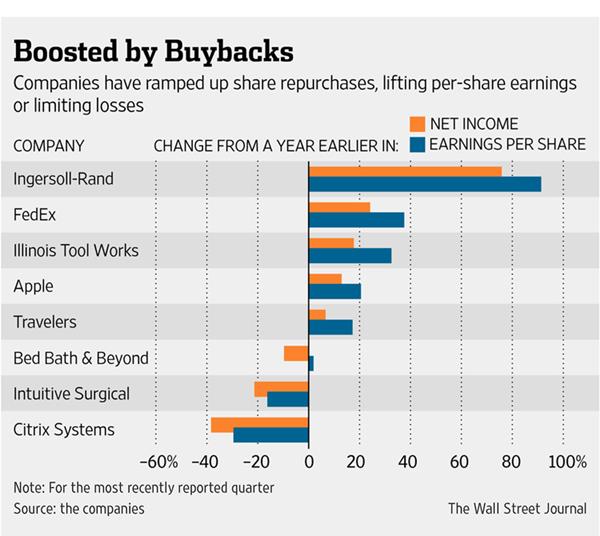

Among those that have invested most aggressively in

their own stock are

Ingersoll-Rand PLC,

Illinois Tool Works Inc., and

FedEx Corp. , which all have

reported year-to-year EPS growth in the latest quarter at least 13

percentage points higher than their gains in overall profit.

Ingersoll-Rand and Illinois Tool spokeswomen said

one-time events were partially responsible for the discrepancy between

net income and EPS growth. FedEx didn’t provide comment.

While the economy has crawled back to life, many

businesses remain reluctant to buy new equipment, build factories or

hire workers. They blame the uneven recovery that has left many

Americans behind and foreign markets that are stumbling.

Repurchases, meanwhile, can boost a company’s curb

appeal. Illinois Tool Works used buybacks to post an EPS surge of 33%,

nearly twice the latest quarter’s bottom-line profit growth.

Bed Bath & Beyond Inc. ’s stock

purchases turned a 10% drop from a year earlier in overall profit into

a penny improvement in EPS. The housewares retailer didn’t provide

comment.

Flouting Wall Street’s conventional wisdom of “buy low,

sell high,” companies tend to vacuum up their stock as prices rise,

and dial back purchases when prices swoon, said Gregory Milano, chief

executive of business consulting firm Fortuna Advisors LLC. Plus, he

said, companies that avoid buybacks usually outperform those that

embrace them over the long term.

“It’s kind of like a kid in school. A lot of kids are

motivated by getting the best grades they can; other kids are focused

on learning as much as they can,” he said. While the child with better

marks might have a leg up entering the workforce, “the kid who

understands it better has a better career.”

Of course, there are times when companies are awash in

cash.

Home Depot Inc. has bought back

almost $50 billion of its shares since 2002. And CFO Carol Tomé says

she is content to pursue this strategy as long as the home-improvement

retailer’s stock price is below what she believes is its intrinsic

value.

“If you’re cash rich, and you have no better place to

put it,” she said. “We’re such a cash cow. The last thing we’re going

to do is sit on cash. That is value-destroying to our shareholders.”

In addition, a well-executed buyback can charm money

managers.

Northrop Grumman Corp. has “done

an A-plus job in our mind,” because it has been buying shares at an

attractive valuation, and

Lockheed Martin Corp. has “done a

similarly good job,” said Matt Lamphier, a portfolio manager at First

Eagle Investment Management, a major shareholder in both defense

companies.

Finance chiefs bristle at the idea that buybacks are

just a mechanism to burnish EPS numbers or pad their bonuses.

“If you’re doing the top-line growth, buying back stock

is just a means of returning capital to shareholders,” said John

Geller Jr. , CFO of

Marriott Vacations Worldwide

Corp. , which announced this month it would buy back 10% of its

shares. Plus, he added, “most investors are fairly sophisticated,” and

can tell the difference between real and fabricated growth.

Still, investors should expect a year-end spending

spree. While about 8% of a year’s buybacks historically take place

October, the peak is in November, with 14% of repurchases, and another

10% come in December, according to David Kostin, senior U.S. equity

strategist at Goldman Sachs Group Inc.

Late last year,

Stanley Black & Decker Inc. said

it would buy back as much as $1 billion of its stock, or 7% of its

current market value, by the end of 2015. But, CFO Donald Allan Jr.

acknowledges that the tonic effects of such deals are temporary.

Buybacks alone “might help your stock price performance

and your company’s performance for a two- to three-year period,” he

said, “but it’s not going to help the performance of the company over

a decade.”

Write to

Maxwell Murphy at

maxwell.murphy@wsj.com and John

Kester at

John.Kester@wsj.com

|