The Celebrity Activist Investor Is Going Extinct

Turns out you don’t need a tough activist reputation to spur

change at companies anymore

By

Lauren Thomas

Dec. 26, 2024 9:00 pm ET

|

Illustration: Rachel

Mendelson/WSJ, iStock (2)

|

An era of big-name activists with fiery personalities waging noisy

proxy battles and wielding brash tactics to win board seats is over.

Carl Icahn, facing

attacks on how he manages his

own publicly traded firm, has slowed his fire. Nelson Peltz, fresh off

losing a battle with Disney,

is planning to

hand his firm to his less

pugnacious son and others. Bill Ackman and Jeff Ubben have

walked away from fights. Dan

Loeb hasn’t had a big proxy war in years.

In their stead is a newer crop of activists who are smaller in size,

less well known and often less eager to brawl.

The activist shift is coupled with changes on the corporate side.

After years of activists hammering the same points over and over, many

boards are more alert. They are moving faster in cases of

underperformance, firing CEOs, striking deals and more willing to

embrace activists who do come along.

The results: The number of proxy fights that go all the way to a vote

is down. Settlements with companies are up, and coming faster than

ever. And the returns of the activist funds are generally

underperforming.

With the proverbial low-hanging fruit picked, and fundraising

difficult, it is unlikely a new activist giant will emerge to strike

fear each time it appears in a shareholder roster.

|

Nelson

Peltz, of Trian Fund Management, sees himself as a

‘constructivist.’ Photo: Marco

Bello/Bloomberg News

|

“The industry in most cases is becoming much more institutionalized,”

said Charlie Penner, a longtime activist investor who launched a new

firm with a name purposefully meant to sound anonymous: Ananym. “It’s

not as personality-driven anymore.”

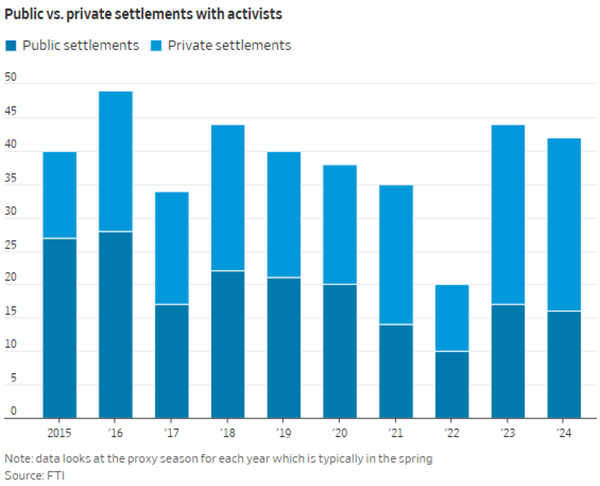

For the past two years, nearly two-thirds

of agreements between companies and activists have been struck

privately, according to an analysis by FTI

Consulting. Even when things

get heated, they are cooling quickly. It took only an average 34 days

for an investor to get a settlement after publicly demanding board

seats in 2024, down from 68 days in 2023, FTI found.

Take some of the settlements that happened

in recent months with investors: CVS

Health quickly

settled with Glenview Capital

Management, which isn’t typically an activist.

Ancora Holdings took on Norfolk

Southern in a

proxy fight earlier this

year—winning three board seats—and later struck a settlement deal to

expand the board and avert a second proxy battle at the railroad

operator. Engaged Capital struck

an agreement last year with

burger chain Shake

Shack. Sachem Head Capital

Management landed a spot on communication-technology firm Twilio’s

board in April. Anson Funds recently snagged a seat on the board of

cloud-software provider Five9.

Penner was at Engine No. 1 when that

little-known firm successfully

challenged the board of Exxon

Mobil and he previously worked

at Jana Partners. He launched Ananym Capital Management this year with

Alex Silver, formerly of another firm, P2.

An “ananym” is a pseudonym made by

spelling one’s name in reverse. Penner said they chose it in part to

underscore today’s dynamics. They recently found a first target:

pushing Henry

Schein, a healthcare products

distributor, to change its board.

“It shouldn’t be about ego or whatever,” Penner said. “It should be

about having good ideas and a good process.”

|

CVS

Health conducted a strategic review and quickly settled with

Larry Robbins’s Glenview Capital Management. Photo: Amir

Hamja for WSJ

|

From ‘corporate raiders’ to ‘constructivists’

Shareholder activism traces its roots back to the 1980s, when

investors started to buy up stakes in companies and agitate for

changes ranging from management shake-ups to strategic breakups. Into

the 1990s, the investors were commonly referred to as “corporate

raiders.”

In the last few decades, they have worked

to shed their negative stigma. Peltz, founding partner of Trian Fund

Management, has waged some of the biggest proxy fights ever, including

at Procter

& Gamble in

2017 and Disney

in 2023. He is also among those

labeling themselves as “constructivists,” for being helpful rather

than antagonistic.

They

pitch complex plans for turnarounds and corporate shifts, not only

financial moves aimed to juice the stock immediately. By proving they

do their homework, firms like Elliott Investment Management, Starboard

Value and Jana have won more allies.

But companies and their defenders still scoff at the constructivist

idea and believe activists themselves can be disruptive.

That is one reason activists propose allies for boards. Fifteen or 20

years ago, the big-name fund managers would mostly nominate themselves

for board seats, said Amy Lissauer, global head of activism- and

raid-defense at Bank of America.

“Activists now are identifying great independent candidates…the

highest quality I have seen,” Lissauer said.

Companies play defense first

Company attitudes have also helped reduce big activist brawls.

Management teams are now more cognizant about the possible threat and

are working to stay ahead of it by swapping directors and executives

and pursuing deals.

In 2024, a number of companies including Boeing, Under

Armour and Intel have ousted

their CEOs without the known

presence of an activist.

“There were many sleepy C-suites and passive boardrooms, and it took

an activist waging a public campaign to shift the mindset,” in years

past, said Mary Ann Deignan, head of Capital Markets Advisory at

Lazard, where she helps defend companies against activist attacks.

CVS this fall ousted its chief executive

and concluded a

strategic review, then struck a

deal to add Glenview founder Larry Robbins to its board of directors.

Robbins had only twice in 24 prior years used an activist playbook.

It is also true that many companies have

grown more fearful of losing because of a recent change

in the proxy voting procedures,

leading them to accept the activists quickly.

The pressure for returns

Many of the new-age activists worked for the first generation. Now

they need to raise money on their own reputations, which has proven

difficult.

Activist hedge funds as a group saw net outflows in four out of the

last six years, though are seeing a slight bump in 2024, according to

HFR, a hedge-fund data tracker.

Activist-focused hedge funds also generally

tend to underperform the broader market.

Through early December of this year, activists were up 6.4% versus the

S&P 500’s rise of over 30%, according to HFR.

“It’s becoming increasingly harder for activists to raise money,” said

Michael Levin, founder of consulting firm the Activist Investor. As a

result, some firms realize “it doesn’t pay to be quite as distinctive

or outspoken.”

There remain exceptions and big fighters, including Elliott and

Icahn.

|

Carl

Icahn remains an activist investor. Photo: Victor

J. Blue/Bloomberg News

|

But Icahn had his own Icahn

Enterprises hit by short-seller

accusations that he was

overvaluing some positions. Icahn has denied the claims, but has

dialed back his activity.

Peltz has seen his firm’s assets under

management shrink and is preparing to step back himself, handing

over more responsibility to a

younger generation of leaders, including his son, Matt Peltz, as well

as Josh Frank and Brian Baldwin. Some wonder whether Trian will

continue launching high-profile activism campaigns when the elder

Peltz is no longer at the helm.

(Baldwin landed a seat on U.K.-based Rentokil

Initial’s board in October,

shortly after Trian disclosed

a position in the pest-control

maker.)

More may go the way of Ackman, once one of the biggest activist

managers. After a series of losses, he decided to be less vocal and

more friendly about investments.

“It makes our job easier and more fun, and

our quality of life better,” Ackman penned in his annual

letter to Pershing Square

investors in 2021. “So, if it is helpful to call this quieter approach

Pershing Square 3.0, let it hereby be so anointed.”

Write to Lauren Thomas at lauren.thomas@wsj.com

Appeared in the December 27, 2024, print edition as 'Era of Turbulent

Proxy Battles With Big-Name Activists Ends'.