|

THE

WALL STREET JOURNAL.

Markets

|

Deals

|

Deals & Deal

Makers

Debt Markets Hold Key to Dell’s Bold EMC Bid

Acquisition to require massive amount of debt

|

|

|

Dell and private equity firm Silver Lake are in advanced talks

to buy data storage company EMC, for what could be the biggest

technology-industry takeover ever. |

By

Dana

Cimilluca,

Don Clark and

Dana Mattioli

Updated Oct. 8, 2015 10:53

p.m. ET

Michael Dell

is pressing ahead with partner Silver Lake on a $50 billion-plus

acquisition of data-storage giant

EMC Corp., people familiar with

the matter said, a bold but risky deal that would require massive debt

financing at a time when credit markets have become less hospitable to

mergers.

Negotiations have advanced and could produce an agreement by next week, the

people said. A merger of that size would be the largest ever in the

technology industry, and Dell and Silver Lake are in talks to secure a debt

package that could top $40 billion to fund it, one of the people said.

The recent rebound in markets has added urgency to the talks. Dell and its

advisers have been grappling in recent days with how to finance the takeover

at a time when markets are volatile and debt investors have balked at a

number of recent takeover-related offerings, another person said. They are

eager to get the deal done before credit tightens further, the person said,

and the improved climate has given them an opening.

The deal would mark an attempt by Mr. Dell to craft a future for a company

caught between the shift toward mobile devices such as

Apple Inc.’s iPhone and fierce

competition among providers of storage capacity and computing power. A

merger in theory could transform the PC and server specialist Mr. Dell took

private two years ago into a one-stop shop capable of serving a full range

of corporate computing needs.

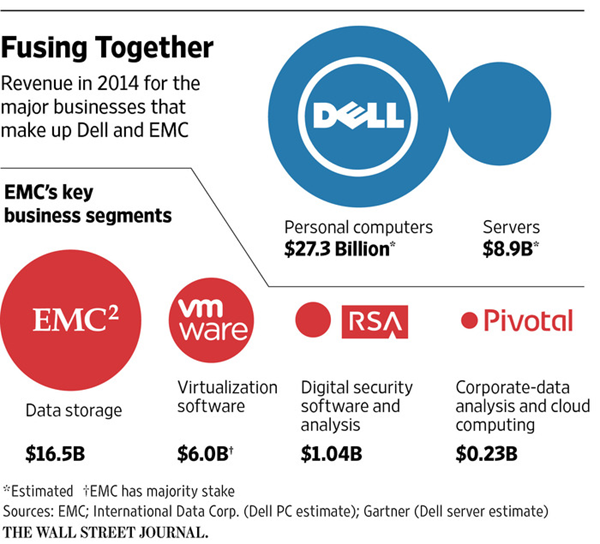

A combined Dell-EMC would encompass computing, networking and storage—both

hardware and software—giving it the breadth to compete more effectively with

larger companies such as

International Business Machines Corp.,

Hewlett-Packard Co.,

Cisco Systems Inc. and

Oracle Corp.

“Dell and EMC would be a tech behemoth,” said Daniel Ives, an analyst at FBR

Research. “It would change the landscape of enterprise computing.”

A deal wouldn’t answer all of the questions facing Dell or EMC. Some close

watchers of the tech scene feel that finding ways to unlock stock-market

value may outweigh any potential business benefits to the companies.

To cover the cost of a deal, closely held Dell and Silver Lake may also need

to come up with as much as $20 billion themselves, which they would likely

do in part by selling shares in EMC’s

VMware Inc.

unit, the people said.

VMware,

which helped develop software that makes corporate data centers more

efficient, is seen as the crown jewel of the transaction. EMC currently owns

roughly 80% of VMware, which has a market capitalization of about $32

billion. Dell would likely hold on to a controlling stake after any sales,

the people said.

A merger with EMC would help Dell exploit a trend toward selling bundles of

hardware components together, known as converged infrastructure, which eases

the need for companies to assemble and test technology combinations

themselves. EMC helped pioneer that tactic in a joint venture with Cisco,

which now supplies networking and computing gear sold along with EMC storage

gear.

An acquisition of EMC would also give the company’s new owners a chance to

turn around its lackluster performance in recent years outside the glare of

public shareholders, much like Dell was. EMC shares rose 4.7% on news of the

possible deal Thursday to $27.18. Still, the stock is up 37% in the past

five years, versus a 76% gain in the S&P 500.

Mr. Dell, who founded his company in his college dorm room in 1984,

pioneered direct sales of computers based first on phone calls and later the

Web. The company later branched into servers, the mainstay computers used to

manage corporate operations, and more recently acquired storage and

networking businesses.

Both Dell and EMC rely heavily on sales of hardware for corporate data

centers, a business expected to gradually decline as more operations are

outsourced to cloud-computing services operated by the likes of Amazon.com

Inc., Google Inc. and Microsoft Corp., said Toni Sacconaghi, an analyst at

Sanford C. Bernstein.

Spokesmen for Dell and EMC declined to comment on the deal talks, first

reported by The Wall Street Journal on Wednesday.

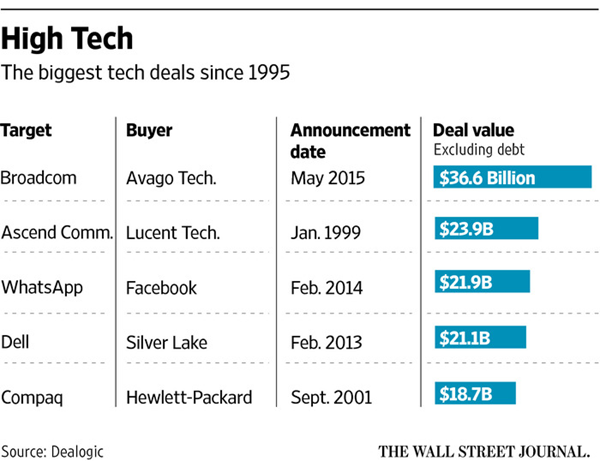

This has been a banner year for takeovers, one that has been characterized

by megadeals like Dell-EMC. There have been nearly $3.4 trillion of mergers

and acquisitions struck world-wide so far this year, according to Dealogic,

putting 2015 on pace to possibly be the best year ever for deal making.

Should credit investors willingly fund an EMC takeover, it would bode well

for other deals and could be a sign that the surge in M&A will continue.

Dell and Silver Lake, which helped take the PC and server maker private in a

$25 billion leveraged buyout in 2013, have assembled a group of lenders

including J.P. Morgan Chase & Co., Bank of America Corp. and Credit Suisse

Group to help them secure the debt portion of the deal, the people said. The

banks would provide a bridge loan that could later be replaced by

investment-grade bonds and syndicated loans, one of the people said.

Following record or near-record debt issuance in recent years that supported

the M&A surge, credit investors have lately become more fickle. In late

September, J.P. Morgan cut a planned high-yield bond sale backing Altice

NV’s purchase of Cablevision Systems Corp. by $1.5 billion, making up the

difference by selling more debt in the loan market. Leveraged loans are

viewed as safer than bonds because they are secured by corporate assets.

More recently, Goldman Sachs Group Inc. and J.P. Morgan struggled to sell

$1.2 billion of loans backing the leveraged buyout of online clothing

retailer FullBeauty Brands, investors said this week.

| |

Photo: bazuki muhammad/Reuters |

One thing working in Dell’s favor as it seeks to cobble together the outsize

debt package is EMC’s relatively limited debt load and its investment-grade

credit rating. The Hopkinton, Mass., company, had just $7.4 billion of debt

and $7.7 billion of cash at the end of June. Dell, meanwhile, had $11.7

billion in debt as of mid-September, according to FactSet, and is junk-rated

from both Standard & Poor’s and Moody’s Investors Service.

Mr. Dell and Egon Durban of Silver Lake are likely to sell as much as $10

billion of shares in VMware, which could leave them with just over 50% of

the software provider; roll over their combined stake in Dell and between

them and possibly others come up with another roughly $5 billion of cash,

one of the people said.

The talks come at a delicate moment for Dell. A trial concludes Thursday in

a Delaware court over whether Mr. Dell and Silver Lake paid a fair price

when they took the company private. Former stockholders with claim to about

37 million shares have argued the company was worth roughly double the

$13.75-a-share buyout price—a figure Dell rejects, citing headwinds facing

its PC business and the risks surrounding its shift toward more-profitable

areas.

At the high end, the difference amounts to more than $500 million, although

a dispute over whether certain shareholders are eligible could reduce that.

If Dell is forced to make a large payment, it could make its efforts to pay

for EMC that much more difficult.

—Shira Ovide and Liz Hoffman contributed to this article.

Write to

Dana Cimilluca at

dana.cimilluca@wsj.com, Don Clark at

don.clark@wsj.com and Dana Mattioli at

dana.mattioli@wsj.com

|