By

Rachel Evans

July 18, 2018 10:51 AM

►

U.S. watchdog wants information on indexes and their providers

► These companies are

growing in influence but aren’t monitored

A regulator’s

work is never done -- and when it comes to exchange-traded funds, it

seems it’s only just begun.

The U.S.

Securities and Exchange Commission, which is

working on an ETF-specific oversight

regime and

considering reviving a proposal to

limit the use of derivatives in the funds, is also asking questions

about the stock and bond benchmarks that underpin 98 percent of the

$3.6 trillion market for exchange-traded products. Currently the firms

that create the indexes supporting these funds do so without SEC

supervision.

“Everyone is

watching intently and we’re trying to be as best prepared as we can

be,” said Dave Gedeon, head of research and development at Nasdaq

Global Indexes. “One of the things that’s been the hallmark of the

industry has been innovation. I would worry that if we went to a new

regulatory regime, that essence of the market would be damaged.”

It’s all part of

a broader effort by regulators to get their arms around the

fast-growing business that’s seen its U.S. assets triple since 2011,

yet has spent decades in the shadows of the investment world.

Index Evolution

Designed to help

money managers and their investors judge a fund’s performance versus

the market, or a subsection of it, indexes began moonlighting as the

linchpin of low-cost investing in the 1970s. Back then, early pioneers

like Vanguard Group’s Jack Bogle found they could cut costs by firing

big-shot traders and achieve market returns by passively tracking one

of these gauges instead.

Since then,

investors have witnessed an explosion of indexes. There are now more

than 3.28 million market benchmarks worldwide, dwarfing the number of

global stocks,

according to the Index Industry

Association. Licensing these gauges to fund issuers and other asset

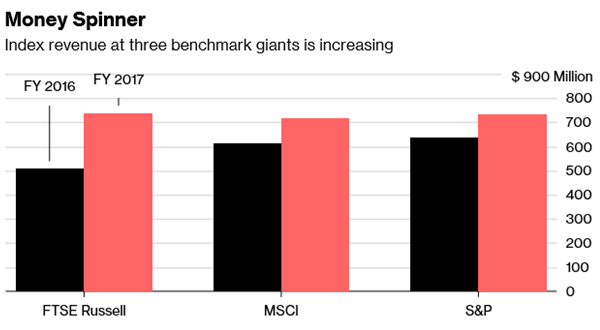

managers helped S&P Global Inc., MSCI Inc. and the London Stock

Exchange Group Plc’s FTSE Russell -- three of the largest indexers --

together

generate more than $2 billion of

revenue last year, according to the companies.

ETFs have added

to the craze, with issuers frequently working with indexers to turn

complex strategies more commonly used by active managers into

benchmarks. Yet, while the issuers and the resulting funds are

regulated, those creating the gauges behind them operate unchecked.

“It’s a purely

reputational business,” said Rick Redding, the IIA’s chief executive

officer. “If you start miscalculating or putting out indexes that are

not representative, no one will use them.”

Teaming Up

Switching to

another gauge, however, isn’t always easy or practical, as those who

would like to

replace the disgraced London

interbank offered rate have found.

A spokeswoman

for MSCI declined to comment, citing company policy on potential

regulation. A spokesman for FTSE Russell declined to comment, while

media representatives for S&P did not immediately respond to emails

requesting comment.

Indexers in the

U.S. rely on a regulatory dispensation known as “the publishers’

exemption” to avoid registering as

investment advisers, the way issuers must do. This clause excuses

those who distribute advice that isn’t tailored to a specific client

or portfolio from more onerous rules. But as issuers and indexers

increasingly team up to create bespoke benchmarks some new ones

threaten this designation, with indexers appearing to be advising

issuers.

“Recent

developments appear to have moved certain index providers away from

what we might think of as publishers,” Dalia Blass, head of the SEC’s

investment management division, said in March. The industry should not

assume that index providers qualify for the exemption and should

revisit fund disclosure to ensure it is describing these indexes and

their strategies clearly and transparently, Blass said.

Judith Burns, an

SEC spokeswoman, declined to comment.

Growing Impact

The U.S. is not

the only regulator taking a hard look at indexing. Within the European

Union, all gauges that are tracked by a fund or used by an investor to

measure performance, have been overseen by national watchdogs since

new rules took effect in January.

While those

regulations stemmed from the Libor fixing scandal, their breadth

reflects how influential indexers have become. Inclusion in a

particular benchmark can

send capital flooding into a country

or into a company’s stock, and more than

$9.9 trillion currently follows or

measures itself against the S&P 500 Index alone. Benchmarkers are also

dipping a toe into oversight themselves, with some

omitting companies with multiple

share classes from their most widely used measures because the

structure limits voting rights.

That’s raised

eyebrows, even among the issuers that rely so heavily on their

services, with Barbara Novick, BlackRock Inc.’s vice chairman,

writing that “policy makers, not

index providers, should set corporate governance standards.”

Should the SEC

decide to pursue its inquiries, the agency’s Office of Compliance

Inspections and Examinations could question fund advisers about it,

according to Barry Pershkow, a partner at the law firm Chapman &

Cutler who used to work at the SEC. These interviews could form the

basis of an enforcement action if the SEC determined that an indexer

was acting as an unregistered adviser for the fund company -- or even

the funds.

“The solution

for those folks who are finding themselves in a questionable place is

to probably think about rearranging the deck chairs a little,”

Pershkow said, possibly by looking more closely at customized indexes

with exclusive licensing rights. “The last thing indexers will want to

do is register as an adviser and become subject to that regulatory

regime.”

— With

assistance by Carolina Wilson, and Benjamin Bain

©2018 Bloomberg L.P. All Rights Reserved