|

|

|

Andrew Smithers

Economics

and markets

Hello!

I’m Andrew

Smithers; I studied economics at Cambridge and used to run the fund

management business at S G Warburg which became Mercury Asset

Management and is now BlackRock.

I set up

Smithers & Co in 1989 as an economics consultancy. Much of the

comments on economics and markets that I read as a fund manager struck

me as nonsense and I have had great fun in pointing this out to

clients over the years.

I now have

the opportunity to disseminate my views more widely and hope that this

will amuse and inform readers.

|

Buybacks and the parallel universe of bankers

Andrew Smithers

| Nov 05 07:00

The damage done to the UK and US economies by

buybacks in preference to capital

investment was a central theme of my book The Road to Recovery, and

it has found its way, not too often I hope, into these blogs. I have

therefore been heartened by the growing interest shown by the financial

press in this threat to our economies.

The Economist recently devoted a

major section to the issue, as did the

Financial Times on October 12.

The change in the way managements are paid drives buybacks but this has yet

to be widely appreciated. The US Federal Reserve’s quantitative easing

programme was rightly underlined by my colleagues as adding the fuel of

cheap debt but, without the preference for buybacks, low bond yields would

have encouraged capital investment. This they markedly failed to do. An

important paper, shortly to be published in the Review of Financial Studies,

“Corporate

Investment and Stock Market Listing: A Puzzle?” by John Asker,

Joan Farre-Mensa and Alexander Ljungqvist demonstrates that a huge

difference has appeared in recent years in the levels of investment by

quoted and unquoted companies.

It is clearly absurd to claim, as is nonetheless so often done, that

companies are deterred from spending on new equipment by fears about future

demand. If this were correct, it would be a concern restricted to quoted

companies and to which unquoted ones are immune. Listing matters because

unquoted companies are more often controlled by investors with a long-term

interest in the company’s future. While this has always been true, the

change in management remuneration has greatly magnified the difference in

incentives and, thus, in the behaviour of the two groups. The difference,

therefore, does not lie in fears about economic prospects but is determined

by whether the companies are listed.

Another misunderstanding was shown in a

letter to the FT from

Insead finance professor

Theo Vermaelen, who criticised the October 12 article by Michael

Mackenzie and Nicole Bullock on the grounds that it is a “widely documented

fact that, on average, companies that buyback stock outperform their peers”.

The key issue here has been misunderstood. The concern is not that buybacks

damage share prices. What we observe is that high buybacks and low

investment have a common cause, which is the change in management

remuneration. While this may or may not be in the interests of shareholders,

the problem is that it severely damages the economy.

Not everything that is good for shareholders is good for the economy. Weak

competition is an outstanding example, to which the impact of modern

management remuneration systems has important similarities. In many

industries, companies have considerable short-term monopoly power. If they

choose to push up prices, which increases the risk of being undercut by

competitors, or keep investment levels low, which would allow competitors to

have lower production costs through newer equipment, they increase the risk

that their companies will lose market share. But, particularly in the case

of investment, these risks are long-term rather than short. Furthermore, if

the incentive to push up prices and underinvest is widespread, the

short-term risks are reduced. The risk of losing market share is low if

almost everyone in an industry is seeking to boost prices and keep down

investment.

A reduction in competition will boost profits and, looked at exclusively

from the narrow view of shareholders, there is no call for governments to

seek to prevent an increase in monopoly power. Indeed, if what is good for

shareholders was automatically good for the economy, then economic policy

would be devoted to reducing competition. But rent-gouging monopolies do

great damage to the economy, which is why we need to be alert to the risks

of falling competition and have an active policy to prevent the rise of

oligopolies. For the same reason, we need policies to counter the damage

that is being done by the change in management remuneration.

There are many ways that this can be done but, before the necessary policies

can be introduced, it is essential that the problem is recognised and widely

debated. The increase in concern, illustrated by the articles in the FT and

The Economist, is therefore to be welcomed. But the level of

misunderstanding and distraction is high and comes in various guises. The

idea, discussed earlier, that the issue is whether or not shareholders

benefit is one misconception. The perceived unfairness of the huge increase

in management pay is another distraction. I sympathise with such concerns

but there is ample evidence that shareholders have received no benefit from

the rise in pay. There is therefore a strong case against the rise in

management remuneration, even from the narrow view of shareholders’

interests. But fairness is a very subjective matter and I fear that, if the

discussion of management pay is limited to whether it is fair or in the

interests of shareholders, it will result in unfocused debate rather than

effective action. I am anxious therefore that the economic damage should be

the subject that receives most attention.

While we seem a long way from the widespread understanding of these dangers,

a paper published in the Harvard Business Review’s September 2014 edition, “Profits

Without Prosperity by William Lazonick,

does an excellent job of pointing them out. The paper rightly scorns the

excuses that corporate executives give for buybacks. Prof Lazonick correctly

identifies the true motivation for buybacks, which is that stock-based

instruments make up the majority of senior executives’ pay.

In addition to their economic importance, buybacks are very important for

equity prices. As companies are the main, and often the only significant,

buyers of shares, the stock market is likely to suffer if companies are

deterred from buybacks by the negative publicity that they are receiving.

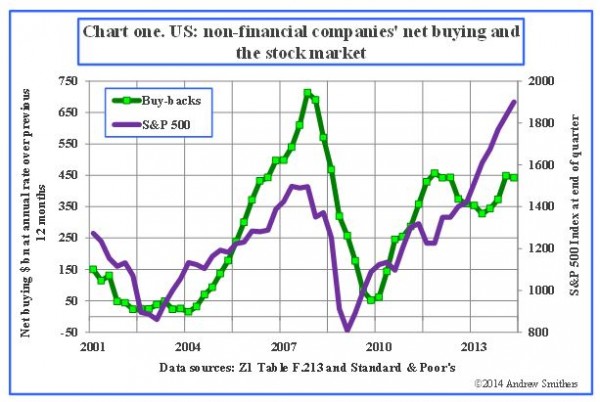

Experience, however, points to the direction of change in share prices as

being a more likely deterrent to buybacks than adverse publicity (see chart

one above). This shows that buybacks rise and fall with the level of the

stock market and it is surely difficult to praise buybacks as being good for

shareholders when they are made at such disadvantageous times. Buying

overpriced shares is a way of destroying value and spending more money when

the market is most overpriced is particularly egregious.

When the market falls, share buybacks destroy less value for shareholders

but they also become less valuable for managements, whose bonuses are linked

to share prices. They become more valuable, however, for those whose bonuses

are linked to returns on equity or earnings per share because the cheaper

the shares are, the more these metrics can be improved by the same dollar

expenditure. If profits start to fall, buybacks cease to be of much help to

management as they cannot offset the negative impact on ROE or EPS.

Provided profits hold up, I think it is more likely that buybacks will

continue to support the stock market. Many of the incentives for managements

will remain in place and, if profits do not fall, the key issue will be the

financial ability of companies to buy shares, which depends on their cash

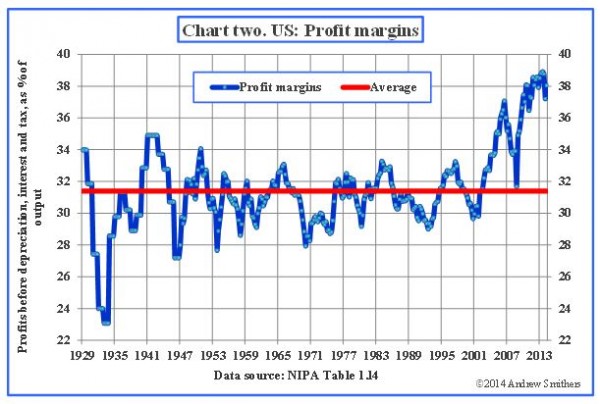

flow and balance sheets. The extremely high level of profit margins (see

chart two below) means that cash flow is abundant for financing buyback. In

addition, companies claim and presumably believe that they have low

leverage, so, if cash flow alone is not enough, increasing debt should pose

no problem.

Mr Mackenzie and Ms Bullock quoted

an alternative view in their article from an investment banker who remarked

that “ buybacks will continue until companies regain pricing power”. Now, in

the universe in which I live, pricing power is revealed in profit margins.

As chart two shows these are at their highest recorded level in the US.

There would appear therefore to be no lost pricing power to be regained.

However, readers of this blog will know that investment bankers and I appear

to inhabit parallel universes.

© The Financial Times Ltd 2014 |

|