Business Day

How to Gauge a

C.E.O.’s Value? Hint: It’s Not the Share Price

Fair Game

By

GRETCHEN

MORGENSON

JUNE

17, 2016

Everybody knows that chief executives

receive bounteous pay as a matter of course. In 2015, for example, the

median

pay for a top corporate executive

at 200 large American companies was $19.3 million.

Less discernible, though, is who

actually earned their pay the most by increasing the value of the

companies they run by a commensurate amount. Such performers are not

to be confused with executives who work to propel their company’s

stock price. This pursuit can have fleeting benefits and disastrous

consequences, as Valeant International, the beleaguered drug company,

has shown.

One reason it’s so hard for shareholders

to determine a chief executive’s value is that companies’ descriptions

of their pay packages are complex. For example, the discussion of

General Electric’s compensation practices took up more than 20 pages

of its 65-page proxy this year.

Any investor who plows through these pay

documents will recognize a common corporate theme: The amounts awarded

to the chief executive are aligned with shareholders’ interests

because the pay is grounded in the company’s performance.

| |

Fair Game

A

column from Gretchen Morgenson examining the world of finance

and its impact on investors, workers and families

See More »

|

| |

|

But companies use a bewildering array of

benchmarks in their compensation decisions. These gauges often vary,

even within the same industry, making apples-to-apples comparisons

difficult and hampering an investor’s ability to determine when an

executive is overpaid.

“It is amazing how complicated companies

make the proxy and how studiously they avoid the simple informative

presentation of relative pay for relative performance,” said Stephen

F. O’Byrne, president of

Shareholder Value Advisors, a

firm specializing in compensation design and performance measurement.

The most common performance metrics used

by companies can be problematic. Total shareholder return, according

to a recent

study by Equilar, a compensation

analysis firm in Redwood City, Calif., is the single most popular

measure related to pay at big public companies.

Companies love total shareholder return

in part because it is easy to calculate. But a company’s stock can

rocket even when its operations are being run into the ground. So

basing pay on total shareholder return can encourage an executive to

manage more for a company’s share price than for its overall health.

“When you look at total shareholder

return relative to pay, you’re not looking at the underlying returns

of the business,” said Mark Van Clieaf, managing director at

MVC Associates International, a

consulting firm. “That can take investors down the wrong path.”

A better way to measure whether a C.E.O.

has created value at a company is to look at its return on capital

over a period of years. This reveals how effectively a company is

using its own money to generate profit in its operations.

When you compare these returns to an

executive’s compensation, you see where pay is justified and where it

isn’t.

I asked Mr. O’Byrne and Mr. Van Clieaf

to analyze returns on capital among the top 200 companies whose

compensation was reported by The New York Times three weeks ago. The

goal was to see how the executive pay at each company stacks up

against its corporate performance and highlight which companies are

giving away the store to their chief executives and which are getting

their money’s worth.

Mr. O’Byrne and Mr. Van Clieaf began by

examining each company’s return on capital over the last five years

and then comparing it with companies in the same industry. This

resulted in a relative return on capital for each corporation.

The experts then compared each company’s

C.E.O. pay last year with that of its peers. This produced a relative

pay figure that could be set against its relative return on capital

over five years. The calculations were adjusted for company size.

Among the top 200 companies,

the study concluded that 74

overpaid their chief executives in 2015 based on five years of

underperformance in return on capital. The total overpayment last year

to the C.E.O.s at these companies, the study found, was $835 million.

Industries with the greatest outsize pay

were energy, technology, media, health care and consumer products, the

study said.

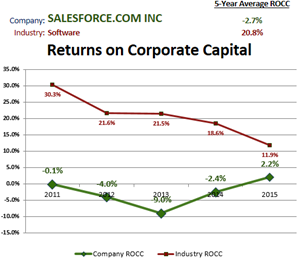

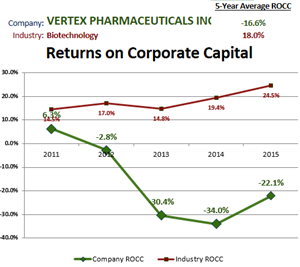

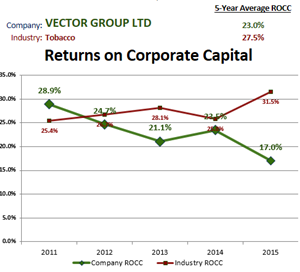

Companies high on the overpayment list

included Salesforce.com, a software company; Vertex Pharmaceuticals;

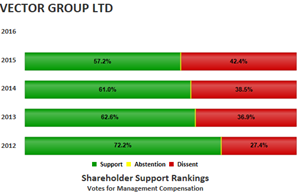

and the Vector Group, a tobacco concern.

All three companies had a return on

capital below that of their peers over the last five years, the

analysis showed. Nevertheless, the pay received by these company’s

chief executives was lush.

For example, at

Salesforce.com, return on capital fell 23 percent over the last

five years. As a result, Marc Benioff, its chief executive, received

almost $31 million more last year than was warranted by the company’s

performance against its peers.

Jeffrey M. Leiden of

Vertex Pharmaceuticals received

$27 million in excess pay based on the company’s negative 35 percent

return on capital over the period. And Howard M. Lorber, the head of

the Vector Group, was overpaid by $35

million last year when judged on the company’s 4.5 percent decline in

return on capital during the previous five years.

Representatives for all of the companies

challenged the idea that return on capital was the best way to measure

their operations.

Chi Hea Cho, a spokeswoman for

Salesforce.com, said that because its business model was based on

recurring revenue, return on invested capital was not the right way to

measure performance. “We have created a thoughtful executive

compensation structure based on total shareholder return, which aligns

executives’ interests directly with those of our stockholders, and

over the last five years, Salesforce has delivered returns of 111

percent, more than double the S.&P. 500 index.”

Paul Caminiti, a spokesman for the

Vector Group, said in a statement: “From 2010 to 2015, Vector’s common

stock produced total annualized returns of 21.6 percent, as compared

to 12.6 percent for the Standard & Poor’s 500 over the same five-year

period.”

A Vertex spokeswoman, Heather Nichols,

said in a statement that successful earlier-stage biotech companies

were measured largely on research productivity and shareholder

returns. “Over the last five years,” she said, “Vertex has delivered

three breakthrough medicines to people with serious diseases and a 259

percent total shareholder return.”

The analysis also identified more than

70 companies whose chief executives were delivering outsize returns on

capital for fair or even undersize pay.

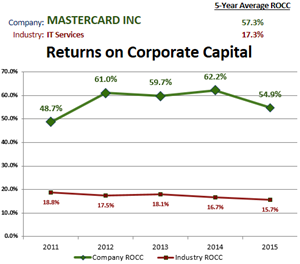

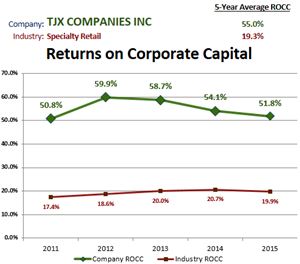

This group included

MasterCard, overseen by Ajaypal Banga, which had a 40 percent

premium compared with its peers, and the TJX

Companies, the retailer run by Carol Meyrowitz, with a 36 percent

excess return on capital.

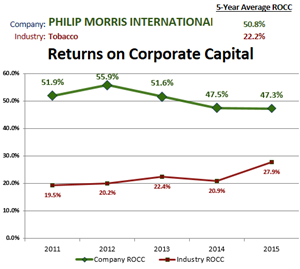

Philip Morris International, a tobacco company headed by André

Calantzopoulos, generated excess return on capital of almost 30

percent compared with its peers.

Gary Lutin, a former investment banker,

said it was crucial for investors to assess whether their companies

were generating more wealth for management than for shareholders. As

overseer of the Shareholder Forum, an independent creator of programs

to provide information investors need to make astute decisions, he has

convened a workshop to focus investor attention on

basic measures of

corporate performance

that generate long-term shareholder

wealth.

“Both investors and corporate directors

need to measure performance based on the profits a company generates

from its competitively successful production of goods and services,”

Mr. Lutin said. “That’s the only real foundation there is for

investment value, and for national prosperity.”

A version of this article appears in print on June 19, 2016, on page

BU1 of the New York edition with the headline: Gauging the Value of a

C.E.O.

© 2016 The

New York Times Company