Business Day

Investors Get Stung

Twice by Executives’ Lavish Pay Packages

Fair Game

By

GRETCHEN

MORGENSON

JULY

8, 2016

It’s a

frustrating fact of life for many

mutual fund investors: Even if

they’re distressed by outsize

executive compensation at public

companies whose shares they indirectly own, chances are good that the

votes cast by their investment managers actually encourage delusional

pay.

In recent years, as executive pay has climbed, fund managers have

continued voicing their approval for stratospheric compensation

packages. The failure by these fiduciaries to use their power to rein

in pay has led some critics to contend that the managers aren’t

viewing the packages in the context of what they cost company

shareholders.

| |

Fair Game

A

column from Gretchen Morgenson examining the world of finance

and its impact on investors, workers and families

See More »

|

| |

|

It is

undeniable that pay arrangements are a shareholder expense, and

sometimes a significant one. Last year, despite a slight decline from

2014,

the median pay package for chief

executives at 200 large United States companies was almost $20

million.

When

compared with those companies’ earnings or revenue, $20 million may

not sound like much. But looking at pay another way, said David J.

Winters, chief executive at

Wintergreen Advisers, a money

management firm in Mountain Lakes, N.J., brings a clearer picture of

the costs that these lush packages mean for shareholders.

The analysis

suggested by Mr. Winters focuses on the stock awards given to top corporate

executives every year, and the two kinds of costs they impose on shareholders.

Stock grants are a substantial piece of the pay puzzle: Last year, they

accounted for $8.7 million of the $20 million median C.E.O. package, according

to

Equilar, a compensation analysis firm in

Redwood City, Calif.

Cost No. 1 is the

dilution for existing shareholders that results from these grants. As a company

issues shares, it reduces the value of existing stockholders’ stakes.

A second cost to

consider, Mr. Winters said, is the money companies pay to repurchase their

shares in trying to offset that dilutive effect on other stockholders’ stakes.

“We realized that

dilution was systemic in the Standard & Poor’s 500,” Mr. Winters said in an

interview, “and that buybacks were being used not necessarily to benefit the

shareholder but to offset the dilution from executive compensation. We call it a

look-through cost that companies charge to their shareholders. It is an expense

that is effectively hidden.”

Mr. Winters and

his colleague Liz Cohernour, Wintergreen’s chief operating officer, totaled the

compensation stock grants dispensed by S.&P. 500 companies and added to those

figures the share repurchases made by the companies to reduce the dilution

associated with the grants.

What they found:

The average annual dilution among S.&P. 500 companies relating to executive pay

was 2.5 percent of a company’s shares outstanding. Meanwhile, the costs of

buying back shares to reduce that dilution equaled an average 1.6 percent of the

outstanding shares. Added together, the shareholder costs of executive pay in

the S.&P. 500 represented 4.1 percent of each company’s shares outstanding.

Of course, these

numbers are far greater at certain companies. The 15 companies with the highest

combination of dilution and buybacks had an average of 10.2 percent of their

shares outstanding.

“It’s not only

today’s expense,” Mr. Winters said. “It’s that the costs of dilution over time

have been going up, so you have a snowballing effect.”

Wintergreen

Advisers has been critical of executive pay for some time. Two years ago, the

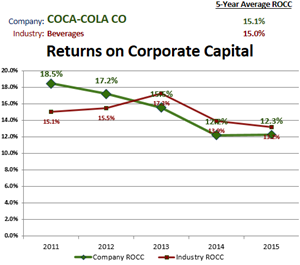

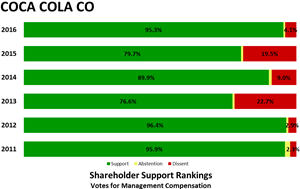

firm led the charge against executive pay at Coca-Cola,

arguing that the stock awards given to Muhtar Kent, the company’s chairman and

C.E.O., were excessively dilutive to existing shareholders’ stakes. Last year,

the company reduced Mr. Kent’s grants by almost half.

And yet, though

Mr. Kent’s total pay fell by 42 percent in 2015, with a package of $14.6

million, he is not headed for the poorhouse.

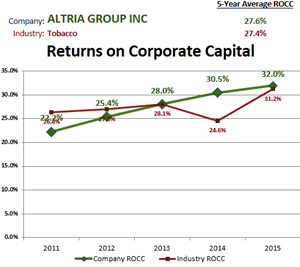

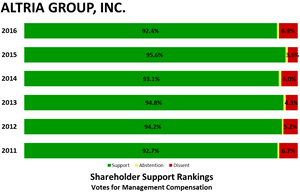

Not all companies

give executives loads of stock grants. Mr. Winters provided four examples with

far less dilution related to compensation plans than is typical in the S.&P.

500. Only one is in that index: the Altria Group, the

tobacco company, with 0.7 percent average annual dilution.

The three other

companies are European: British American Tobacco, with zero dilution; Nestlé,

with 0.1 percent, and the Swatch Group, with 0.6 percent.

Mr. Winters

contended that the circular arrangement of stock grants and buybacks was

especially costly at companies in the S.&P. 500. One reason, he said, is that

many of the large money management firms offering index funds and

exchange-traded funds do not generally vote against pay packages at the

companies whose shares they own on behalf of their clients.

Consider this

year’s votes by BlackRock and State Street, two major providers of index funds

and exchange-traded funds. According to

Proxy Insight, as of June, BlackRock and

State Street voted to support the pay at 95 percent of S.&P. 500 companies. This

parallels data from previous years.

Why these

companies don’t take a more aggressive stance on pay issues is something of a

mystery. Some critics speculate that it may be because their own executive pay

is high, or that they don’t want to alienate corporate clients, whose money they

manage, by voting against their pay.

When asked about

their votes in support of lavish pay, money managers often contend that when

they see problems with a company’s compensation, they talk privately with its

board to try to effect change.

For example, Anne

Elizabeth McNally, a spokeswoman for State Street, which has $415 billion under

management in a wide array of E.T.F.s, said it used

a screening process to identify companies

whose pay practices were problematic.

It engages with

these companies, and if they don’t take action, State Street will vote against

their compensation, Ms. McNally said. Last year, she said, State Street voted

against pay practices at almost half the 1,424 companies it had selected for

review.

But this kind of

engagement process is slow, frustrating investors who are eager for a quicker

pace of change in pay plans.

Highlighting the

erosion of their wealth that lush executive compensation can mean for investors

might just light a fire under more money managers. And to this end, Ms.

Cohernour, the Wintergreen C.O.O., suggested that the Securities and Exchange

Commission help by requiring companies to include in their annual proxy

statements both the dilution that their executive stock grants represent and the

cost of the buybacks conducted to offset it.

“Companies could

easily make this information clear in their proxy materials instead of making

investors dig through documents for it,” Ms. Cohernour said. “These are

significant factors for an investor to know.”

A version of this article appears in print on July 10, 2016, on page

BU1 of the New York edition with the headline: Stung Twice by Lavish

Pay at the Top.

© 2016 The

New York Times Company