Business Day

Want Change?

Shareholders Have a Tool for That

Fair Game

By

GRETCHEN

MORGENSON

MARCH

24, 2017

|

The Exxon Mobil refinery in

Torrance, Calif. The topic of climate change and its effects

will again appear on shareholder proxies this year at companies

like Exxon Mobil.

Jamie Rector/Bloomberg News |

Are you

an investor who usually junks the voluminous corporate proxy

statements that arrive each spring, declining to take part in director

elections and other governance matters because you think your vote

won’t count?

If so,

you are not alone. With millions of shares outstanding at large

companies, it’s hard to believe that an individual investor’s vote can

make a difference.

But the stakes are

higher this year. If, for example, you’re concerned about the Trump

administration’s plans to roll back regulations throughout corporate America,

you may want to take a more active approach to proxy voting.

| |

Fair Game

A

column from Gretchen Morgenson examining the world of finance

and its impact on investors, workers and families

See More »

|

| |

|

Say that the new leaders at the

Securities and Exchange Commission

and the

Environmental Protection Agency

relax their agencies’ oversight, as anticipated. That would mean

shareholder votes in favor of holding executives accountable on

executive pay, climate change issues and other governance matters are

especially important.

“There’s

never been a better time to address these issues, whether as an

institutional investor or an individual,” said Nell Minow, vice

chairwoman at

ValueEdge Advisors, a firm that

guides institutional shareholders on how to reduce risk in their

portfolios. “If you are worried that your company is lobbying to

weaken environmental rules, for example, then it’s really a fabulous

opportunity for you to join in with the institutions and other

economic forces making it clear to companies that they can’t get away

with it.”

As was the case

last year, the topic of climate change will again appear on shareholder proxies

this year. One proposal that gained a lot of traction among investors in 2016

asked energy companies to publish an analysis of how their holdings would be

affected in the long term by measures limiting the global increase in

temperature to 2 degrees Celsius — a goal

agreed to by nations in the 2015 Paris

accord.

That kind of

analysis may force a company to alert shareholders that its assets would not be

worth as much under those conditions. (BHP Billiton, the Australia-based mining

giant,

undertook such a study in 2015 and concluded

that while its asset value would be affected, it would continue to create value

for shareholders.)

Management at the

companies whose proxies included these proposals generally urged investors to

vote against them. Still, they received substantial support at some companies —

38.1 percent of votes cast at Exxon Mobil favored the proposals, as did 40.8

percent at Chevron, and almost half the votes at Occidental Petroleum.

None of these

companies have published a proxy statement yet, but similar proposals are likely

again this year at those and other energy companies, governance experts said.

Fresh support from investors could put the proposals over the top.

Shareholders

should realize that they can no longer rely on the government to urge companies

to recognize the risks that climate change poses to their operations. That is

the view of Edward Kamonjoh, executive director of the

50/50 Climate Project, a nonprofit

organization that helps institutional investors work with corporate boards on

climate change issues. “Investors have to become more involved to exercise their

collective power as owners of these corporations so that they run their

businesses in the best long-term economic interests,” he said in a telephone

interview.

Of course,

shareholder proposals are typically not binding, so companies are not required

to abide by them. Still, managers are usually loath to ignore the wishes of a

majority of their shareholders.

Individual

investors can effect change this year on another topic: company policies

governing when it should act to recover an executive’s compensation because of

corporate wrongdoing.

The idea of

recouping executive pay took hold in the early 2000s after the Enron and

WorldCom accounting fiascos. The Sarbanes-Oxley

law of 2002 gave the S.E.C. the ability to

go after incentive pay earned improperly by an executive in connection with an

accounting irregularity.

Actual clawbacks

have been few, however. So the Dodd-Frank legislation of 2010 required the S.E.C.

to write new rules expanding the potential for recoveries.

In July 2015, the S.E.C. proposed a

rule requiring companies to adopt clawback

policies on executive compensation. But it did not go into effect before the

Trump administration took over. That rule is probably dead. Nevertheless,

shareholders may be able to improve clawback policies at two big companies this

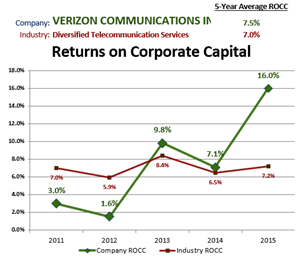

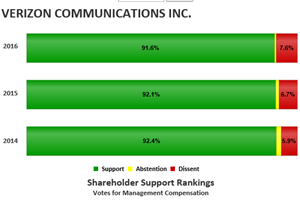

year: Verizon and Caterpillar.

“The

whole concept of executive compensation is pay for performance,” said

Cornish F. Hitchcock, a lawyer in Washington

who is advising the group of Verizon shareholders proposing the policy change at

the company. “If executives’ behavior costs the company money or damages its

reputation, shouldn’t there be consequences?”

The Verizon

shareholders agitating for change are a group of 205,000 former telecom

employees known as the

Association of BellTel Retirees. Since 1997,

10 proposals put forward by the retirees have been voted on by Verizon

shareholders; in eight of the measures, the company responded by changing its

policies, according to the retirees’

website.

This year, the

retirees’ organization wants the company to expand its clawback policy;

Verizon’s current

policy limits pay recoveries to executives

who engaged in “willful misconduct” that causes significant financial or

reputational harm to the company.

Far too narrow,

the retirees say. First of all, the term “willful misconduct” is ill defined,

Mr. Hitchcock said, and may limit pay recoveries to egregious cases only. In

addition, Verizon’s policy should also cover wrongdoing that arose because of

negligence or a supervisory failure.

Verizon is urging

its shareholders to vote against the retirees’ proposal at the annual meeting in

early May. James Gerace, a Verizon spokesman, explained why in a phone

interview.

“Negligence could

be really broad and open to interpretation,” he said. “We were trying not to

make it so broadly applicable that it was going to paralyze our people in making

decisions.”

In their proposal,

the retirees detailed why Verizon’s current policy is problematic, citing a 2015

regulatory settlement Verizon struck with the Federal Communications Commission.

The agency contended that Verizon placed unauthorized third-party charges on

customers’ cellular phone bills; the company paid $90 million to settle the

matter.

Under the policy,

it’s unclear whether the company scrutinized the actions of any executives

relating to this settlement, the retirees’ proposal said. So they urged Verizon

to change its policy so that it must disclose details of any clawbacks to

shareholders as well as decisions not to pursue recoveries.

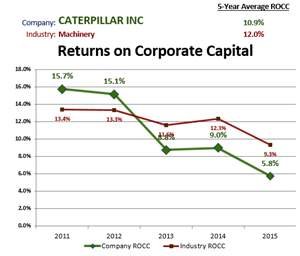

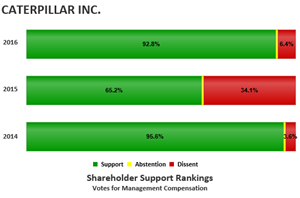

Shareholders of

Caterpillar, the heavy-equipment maker whose offshore tax practices are under

investigation by federal authorities, will

vote on clawbacks this year.

Tejal Patel,

corporate governance director at

Change to Win Investment Group, said her

group put forward a shareholder proposal on clawbacks for this year’s annual

meeting. “If something goes wrong,” she said, “you want executives to be held

accountable and know what the company is doing about it.”

A Caterpillar

spokeswoman confirmed that the proposal would be on the proxy this year.

Of course, many

individual investors — those who own shares in mutual funds — can’t speak their

minds through proxy votes. Their funds vote their shares for them and all too

often follow corporate boards’ recommendations to reject shareholder proposals.

If you own shares

in a mutual fund and feel strongly about these issues, write to the fund’s

executives and tell them how you want them to vote your shares. They may not do

as you say, but at least they’ll know where you stand.

A version of this article appears in print on March 26, 2017, on Page

BU1 of the New York edition with the headline: Want Change?

Shareholders Have a Tool.

© 2017 The

New York Times Company