Business Day

The Accounting Tack

That Makes PayPal’s Numbers Look So Good

Fair Game

By

GRETCHEN

MORGENSON

AUG. 4, 2017

|

Dan Schulman, chief executive of

PayPal, taking a selfie after his company’s initial public

offering in July 2015.

Andrew Gombert/European Pressphoto Agency |

Dan

Schulman, chief executive of PayPal, taking a selfie after his

company’s initial public offering in July 2015. Credit Andrew Gombert/European

Pressphoto Agency

Investors liked what they saw in PayPal’s second-quarter financial

results, reported by the digital

and mobile payments giant on July 26. Revenues grew to $3.14 billion

in the quarter that ended in June, an increase of 18 percent over the

same period last year. Total payment volume of $106 billion was up 23

percent, year over year.

Even better,

PayPal’s favored earnings-per-share measure — which it does not calculate in

accordance with generally accepted accounting principles, or GAAP — came in at

46 cents per share, 3 cents more than Wall Street analysts had expected. The

company has trained investors to focus on this number, rather than on the less

pretty GAAP-compliant numbers most companies are judged by. And

focus they did.

Exceeding

analysts’ estimates — “beating the number,” in Wall Street parlance — is crucial

for any corporate leader interested in keeping his or her stock price aloft.

Even the smallest earnings miss can send shares tumbling.

Examining how a

company meets or beats analysts’ estimates, therefore, can be illuminating.

| |

Fair Game

A

column from Gretchen Morgenson examining the world of finance

and its impact on investors, workers and families

See More »

|

| |

|

PayPal’s stock has been on a tear this year, up almost 50 percent

since January. At a recent $59, its shares are trading at over 40

times next year’s earnings estimates. It is clearly an investor

darling, providing all the more reason to dig into its numbers.

Naturally, many

factors contributed to PayPal’s second-quarter earnings. But one element stands

out: the amount the company dispensed to employees in the form of stock-based

compensation.

How could

stock-based compensation — which is a company expense, after all — have helped

PayPal’s performance in the quarter? Simple. The company does not consider stock

awards a cost when calculating its favored earnings measure. So when PayPal

doles out more stock compensation than it has done historically, all else being

equal, its chosen non-GAAP income growth looks better.

Accounting rules

have required companies to include stock-based compensation as a cost of doing

business for years. That’s as it should be: Stock awards have value, after all,

or employees wouldn’t accept them as pay. And that value should be run through a

company’s financial statements as an expense.

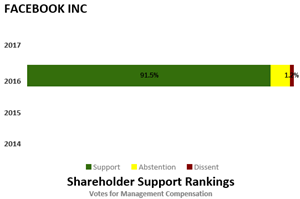

Consider the

practice at Facebook, a company PayPal identifies as a peer. In its most recent

quarterly income statement, Facebook broke out the roughly $1 billion in costs

associated with share-based compensation that it deducted from its $9.3 billion

in revenues.

Back in the 1990s,

technology companies argued strenuously against having to run stock compensation

costs through their profit-and-loss statements. Who can blame them for wanting

to make an expense disappear?

They lost that

battle with the accounting rule makers. But then they took a new tack:

Technology companies began providing alternative earnings calculations without

such costs alongside results that were accounted for under GAAP, essentially

offering two sets of numbers every quarter. The non-GAAP statements — called pro

forma numbers or adjusted results — often exclude expenses like stock awards and

acquisition costs. And the equity analysts who hold such sway on Wall Street

seem to be fine with them.

As long as

companies also showed their results under generally accepted accounting rules,

the Securities and Exchange Commission let them present their favored

alternative accounting.

PayPal is by no

means the only company that adds back the costs of stock-based compensation to

its unconventional earnings calculations. Many technology companies do,

contending, as PayPal does, that their own arithmetic “provides investors a

consistent basis for assessing the company’s performance and helps to facilitate

comparisons across different periods.”

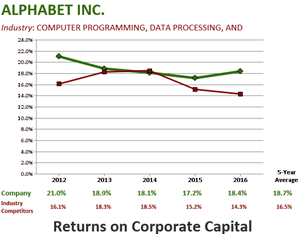

Still, some

technology leaders are dumping the practice. In addition to Facebook, Alphabet

said this year that it would no longer present results that excluded the costs

of stock-based compensation.

Dave Wehner,

Facebook’s chief financial officer, told investors on a May conference call that

the company would report results that include share-based compensation because

it’s a true cost of running the business.

Ruth Porat, chief

financial officer of Alphabet, which is Google’s parent company,

said the same thing on a conference call in

January.

Under generally

accepted accounting principles, PayPal reported operating income of $430 million

in the second quarter of 2017. That was up almost 16 percent from the $371

million it produced in the same period last year.

But under PayPal’s

alternative accounting, its non-GAAP operating income was $659 million in the

June quarter, an increase of almost 25 percent from 2016.

So what’s to

account for the added $230 million in operating income under PayPal’s preferred

calculation? Most of it — $192 million — was stock-based compensation PayPal

dispensed to employees in the June quarter and added back to its results as

calculated under GAAP.

That was a big

jump — 57 percent — from the $122 million PayPal handed out during the second

quarter of 2016. And back in 2015, PayPal reported just $89 million in stock

awards.

I asked PayPal why

it has been ratcheting up its stock-based compensation. Amanda Miller, a PayPal

spokeswoman, declined to discuss why the company was raising its stock-based

pay, and the role the increase played in the company’s recent results. She

provided this statement: “We pay for performance and align our compensation with

how shareholders are rewarded. We believe our treatment of stock-based

compensation is broadly consistent with our peer group.”

But this isn’t

accurate, according to the companies PayPal lists as peers in its proxy filing.

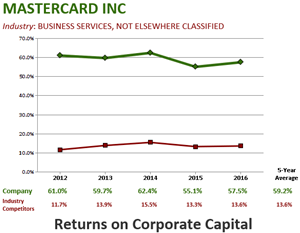

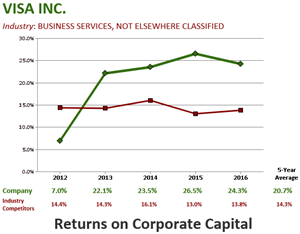

At least four of those companies — Alphabet, Facebook, Mastercard and Visa — do

not exclude stock-based compensation from their earnings calculations as PayPal

does.

Craig Maurer is a

partner at

Autonomous, an independent investment

research firm in New York. He follows payments companies and rates PayPal’s

stock an underperformer.

In a telephone

interview, Mr. Maurer was critical of how the company accounts for stock-based

pay. He said that as a percentage of PayPal’s non-GAAP operating income,

stock-based compensation has risen to 29 percent this year from 17 percent in

2015.

“They are

literally taking a cost out of their income statement, moving it to a different

line and backing it out of results,” Mr. Maurer said in an interview. “And you

can see that it’s adding significantly to their ability to meet earnings

expectations. If you backed out the difference between what we were expecting on

stock-based comp in the quarter versus what they reported, it was 2 cents of

earnings.”

In other words,

the increase in stock-based compensation made a big contribution to PayPal’s

results versus what analysts had been expecting.

PayPal’s

stock-based compensation practices have another noteworthy effect: They drive

executive pay higher at the company. Here’s

how.

The company says

it has three main metrics for calculating its managers’ performance pay each

year. One of those measures, its proxy shows, is non-GAAP net income. So, as

PayPal awards more and more stock to its executives and employees, non-GAAP net

income shows better growth. And the greater that growth, the more incentive pay

the company awards to its top executives.

For PayPal

insiders, at least, that’s one virtuous circle.

A version of this article appears in print on August 6, 2017, on Page

BU1 of the New York edition with the headline: Making PayPal’s Numbers

Shine.

© 2017 The

New York Times Company